Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

May 15, 2026

A trade looks clean on the chart, the wallet you follow has started building size, and the token has held support for hours. Then the market lurches. Your stop gets hit, price overshoots, liquidity thins out, and the move that looked manageable turns into a scramble. Most traders call that “bad luck.”

Usually it's bad volatility measurement.

In DeFi, volatility isn't just how far price moves. It's how violently price moves, when that movement happens, how hard it is to execute during that move, and whether derivatives or on-chain flows were already warning you before the candle printed. If you trade on-chain and still rely on a single chart indicator borrowed from equities, you're using a partial map in a market that never closes.

The familiar failure pattern looks like this. A trader sees a token grinding higher in a narrow range and assumes risk is low because the chart looks calm. They size up, maybe increase their exposure, maybe mirror a wallet entry. Then a burst of selling hits during a thin-liquidity window, the range breaks, and slippage does more damage than the candle itself.

That mistake starts with treating volatility as a visual impression instead of a measured condition.

A lot of DeFi traders still judge market risk by asking one question: “How big have the candles been?” That's too shallow for an always-on market. A token can look quiet while liquidity is deteriorating, while funding is getting unstable, or while large wallets are rotating inventory toward venues where liquidation pressure can build fast. In meme tokens and thinner pairs, that disconnect gets even worse, which is why low liquidity increases meme token volatility in ways a simple chart scan won't capture.

Volatility hurts most when traders confuse a quiet chart with a safe market.

The traders who survive this space longest don't try to predict every move. They build a better read on market conditions first. That changes position size, stop placement, pair selection, and whether a signal is worth taking at all.

A token can close flat on the day and still be dangerous to trade.

That happens all the time in crypto. Price ends near where it started, but the route there includes thin order books, sudden liquidity withdrawals, a burst of liquidations on perp venues, and wide execution slippage for anyone trading size. If you measure volatility only from closing prices, a lot of that stress disappears from view.

Volatility measurement starts with a distinction many traders skip. Price direction tells you whether the asset moved up or down. Price level tells you where it trades now. Volatility tells you how unstable the path was, and in DeFi that path often matters as much as the destination.

Two tokens can print the same daily return and offer completely different trading conditions. One moves in a steady market with consistent depth. The other chops through air pockets, wicks through stop clusters, and gaps between liquidity bands on DEXs. On paper, the return looks similar. In practice, the second market is far harder to hold and far more expensive to trade.

The first category is historical volatility, also called realized volatility. It looks backward and asks how much returns have varied over a chosen sample. In standard market practice, that usually means calculating the standard deviation of returns over a set window, often from daily closes, then annualizing it.

That works well enough as a baseline. It gives traders a common yardstick for comparing assets, regimes, or time periods.

It also breaks in a 24/7 market if used alone.

Crypto does not have a clean open and close like equities. Volatility can build during low-liquidity hours, then get expressed later when larger flow returns. A close-to-close measure can understate what happened, especially for on-chain assets where liquidity is fragmented across pools and venues.

The second category is implied volatility. It is inferred from options prices and reflects what the options market is pricing in for future movement. In traditional markets, implied volatility is often a useful forward-looking signal because options books are deep and continuously traded.

In DeFi, that signal is less consistent. Some assets have no meaningful options market. Others have options liquidity that is too thin to trust as a broad market estimate. So traders often borrow the concept of implied volatility without having the market structure that makes it reliable in TradFi.

For on-chain trading, the gap between realized volatility and tradable risk is wider than many traders expect.

A token may show moderate historical volatility while the actual setup is deteriorating. LP depth can shrink. Bridge flows can become one-sided. A few large wallets can pull inventory from pools. Perp funding can get crowded in one direction. None of those conditions need to appear clearly in a basic volatility series, yet each one can turn a normal move into a disorderly one.

That is why volatility should be treated as one layer of market risk, not the whole map. A cleaner framework combines price dispersion with liquidity quality, execution conditions, and positioning pressure. This explanation of volatility vs risk in liquidity pool token analysis is useful if you want the distinction laid out more explicitly.

For trading decisions, volatility measurement should answer three questions:

That third question matters more in DeFi than many chart-based systems admit. In equities, a volatility spike is often discussed as a price problem. On-chain, it is also a liquidity problem. The same position can become harder to exit just as risk rises.

Practical rule: A market is only calm when price movement, liquidity, and positioning are stable at the same time.

A token can show the same daily realized volatility as another asset and still be far harder to trade. One has thick books, steady pool depth, and orderly funding. The other trades fine until liquidity thins, then slips 3 percent on a medium-sized order. That is why DeFi traders need a toolkit, not a single volatility number.

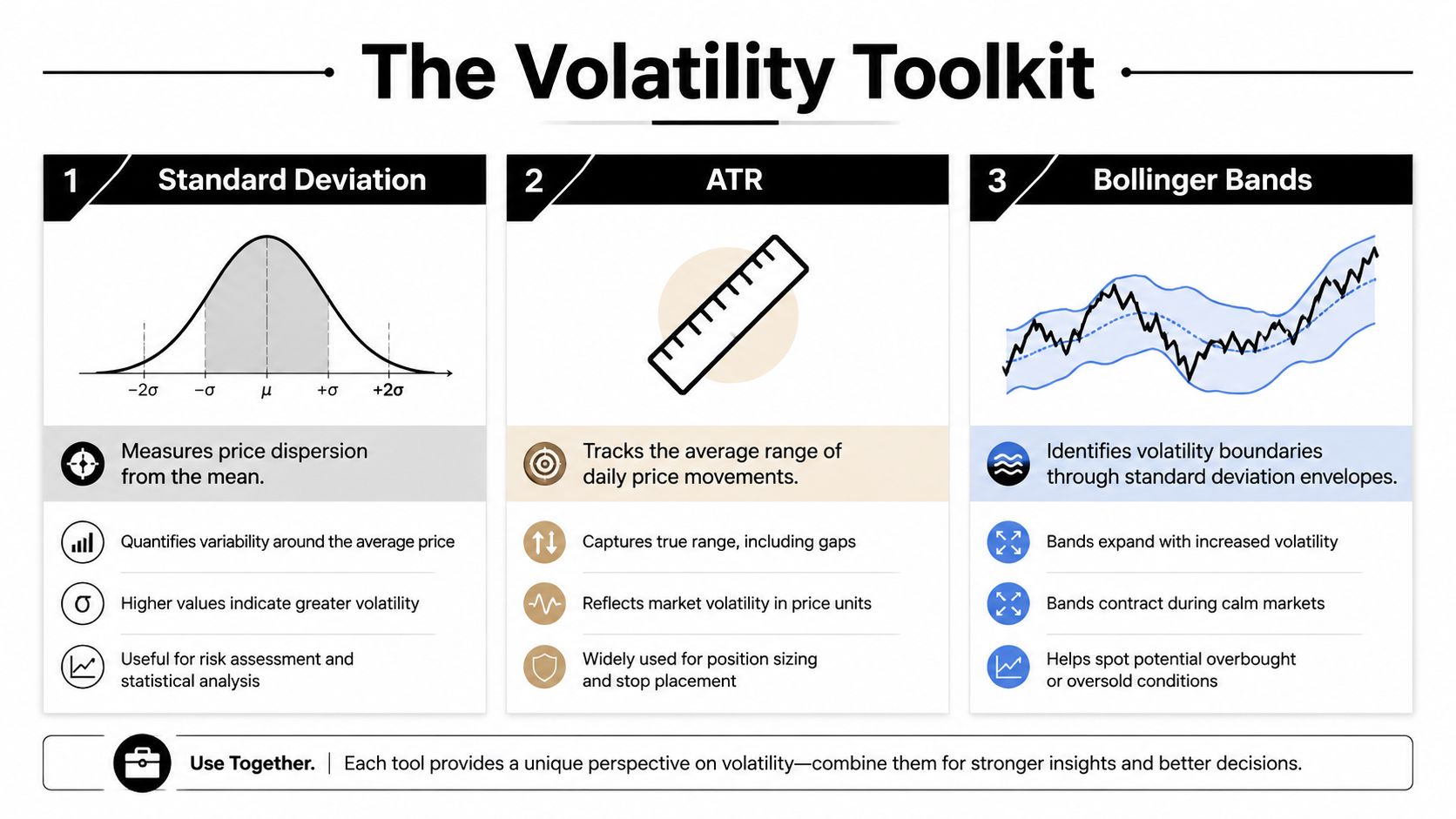

Standard deviation is the base layer for volatility work. It measures how widely returns spread around their average. In practice, it helps answer a simple question: are recent moves staying near the usual range, or are they starting to scatter?

That makes it useful for screening assets, comparing regimes, and building a baseline before adding more context. A quant desk will usually start here because many other volatility measures are just variations on this idea.

Its limitation in crypto is obvious once you trade around the clock. Close-to-close returns can look calm while the market went unstable for several hours overnight, then mean-reverted before the daily candle finished. For DeFi markets, that missing path matters because execution risk often shows up before end-of-period data does.

Historical volatility turns recent return dispersion into a percentage that is easy to compare across tokens and timeframes. It is a clean dashboard number. It is also easy to misuse.

For ranking assets, it does the job well. If one token has been moving much more than another, the trade usually needs smaller size, wider stops, or both.

The problem is that annualized historical volatility smooths the timing of the stress. In equities, that can be acceptable because trading hours are fixed and liquidity patterns are more stable. In crypto, the same reading can hide whether the turbulence happened during active hours with deep liquidity or during thin hours when a modest order can push price far off fair value.

Average True Range, or ATR, is one of the few volatility metrics that maps directly to trade management. It measures the typical range a market travels over a period, which makes it practical for setting stops, estimating required breathing room, and checking whether a breakout has real expansion behind it.

For DeFi traders, ATR is useful because it connects analysis to order placement:

ATR still has blind spots. Crypto does not have the same session gaps as equities, but it does have liquidity gaps. A token can print a normal-looking ATR while the actual problem is that depth disappears at specific hours or on specific venues. ATR tells you how far price has been moving. It does not tell you how expensive it will be to get out.

Bollinger Bands are less useful as a pure risk measure and more useful as a visual map of compression and expansion. They wrap price in a moving envelope based on standard deviation, so traders can quickly see when the market is tightening or starting to fan out.

That is helpful for pattern recognition. It is weaker for decision-making on its own.

In on-chain markets, band compression can persist because flows are waiting on a catalyst, not because risk has fallen. A breakout through the band can also be misleading if it is driven by liquidations or a temporary hole in pool depth rather than broad demand. Used alone, bands often overstate the quality of the signal.

Range-based estimators such as Parkinson are more useful in 24/7 crypto because they use intraperiod information instead of relying only on closes. That makes them better at catching markets that stay noisy inside the day even when the final return looks moderate.

This is closer to how traders experience volatility. PnL is affected by the path, fills, and slippage, not just by where the candle closes.

These estimators still need clean data. On-chain assets often trade across fragmented venues, with varying liquidity quality and occasional price distortions from thin pools. If the underlying data is messy, the estimate can look precise while reflecting noise. The fix is to pair price-based estimators with venue and liquidity checks, such as a routine to check on-chain liquidity and wallet activity before a trade.

| Metric | What It Measures | Best For | Crypto-Specific Caveat |

|---|---|---|---|

| Standard Deviation | Dispersion of returns around the average | Baseline comparison and quantitative screening | Close-only data can miss intraday instability and venue fragmentation |

| Historical Volatility | Standard deviation of returns expressed as an annualized percentage | Ranking assets by recent realized movement | A clean annualized figure can hide when volatility and slippage actually occurred |

| ATR | Average realized range over time | Stop placement, breakout filtering, position sizing | Useful for trade management, but it does not capture depth loss or execution stress |

| Bollinger Bands | Volatility envelopes around a moving average | Visualizing compression and expansion | Helpful for context, weak as a standalone signal in thin on-chain markets |

| Parkinson Estimator | Range-based realized volatility using high-low data | Capturing intraday movement more fully | Better for 24/7 markets, but sensitive to poor venue data and distorted prints |

The useful approach is to assign each metric a job.

Use standard deviation or historical volatility to compare regimes. Use ATR to define trade risk. Use Bollinger Bands to spot compression and expansion. Use range-based estimators when you need a better read on always-open markets where the close hides too much.

What fails is asking one metric to do all of that at once. In DeFi, a volatility framework has to answer two questions at the same time: how much price is moving, and what market structure will do to your execution if that movement accelerates.

Price charts are late to some of the most important volatility events in crypto.

That's the edge gap between traditional volatility measurement and DeFi-native trading. A chart shows what already happened in price. On-chain and derivatives data often show what's building underneath.

Bullrush highlights a problem retail traders routinely miss. Derivatives data like funding rates and liquidation levels often signal stress hours before spot charts show volatility spikes, and the gap gets worse when liquidity deteriorates during off-peak hours (spot and derivatives volatility disconnect).

That statement lines up with what many active traders see in practice. Spot can look orderly while magnified exposures are becoming unbalanced. Once the unwind starts, price catches up fast.

A useful DeFi volatility framework pays attention to market structure, not just candles.

These aren't magic predictors. They're context signals. They improve your read on whether a calm chart is calm.

Crypto doesn't just move. It cascades.

When traders with amplified positions crowd one side, a relatively small push can trigger liquidations. Those liquidations force market orders, those market orders move price further, and the next layer of positions gets hit. That's volatility clustering in practice. High volatility tends to arrive in bursts because the structure itself amplifies the move.

For copy traders, this matters a lot. Mirroring a profitable wallet without checking market conditions can be dangerous if that wallet entered during deep liquidity and you're copying into a thinner phase.

Instead of asking only whether realized volatility is rising, ask four better questions:

A practical way to monitor the first piece is with tools that surface wallet behavior directly. Wallet activity tracking on-chain helps traders inspect whether smart money flows are expanding before spot charts fully react.

The strongest volatility signals in crypto often come from disagreement. Spot looks stable, but wallets, funding, and liquidity all say stress is building.

A DeFi trader can look safe on a daily chart and still get run over overnight. The usual calculation is not wrong. It is incomplete for a market that trades every hour, fragments across venues, and can gap on thin liquidity.

Use one pricing method for the full sample. If you mix CEX closes, DEX swaps, and aggregator marks without checking how each is constructed, the volatility number starts reflecting data inconsistencies instead of market risk.

Choose the interval based on the decision you are trying to make. Daily closes work for broad portfolio monitoring. Hourly or shorter intervals are more useful for active DeFi trading, especially for tokens that trade differently during Asia, Europe, and US hours.

On-chain markets add another wrinkle. A print from a shallow pool can exaggerate realized movement, while an aggregator price can smooth over the slippage you would face. For trading, I prefer data that matches executable conditions, not just a clean-looking chart.

Volatility is measured from returns. A $1 move means very different things for a $10 token and a $1,000 token.

The basic process is simple:

That spread is the standard deviation of returns. If you want an annualized figure from daily data, use the square root of the number of trading periods in your convention.

For crypto, that convention deserves attention. Equity traders often annualize from a weekday calendar. Crypto trades continuously, so the annualization choice should match the way you sample the market. The exact multiplier matters less than being consistent across assets and backtests.

A basic spreadsheet handles this well:

Use a rolling measure, not a single full-sample number.

A static volatility figure hides regime shifts. A 30-period rolling series shows whether risk is expanding, compressing, or staying unstable. That is usually the part worth trading around.

Desk habit: Plot volatility beside price and volume. The level matters. The change in level often matters more.

Traditional volatility workflows were built around markets with opening bells and closing auctions. Crypto does not have that structure. A daily close can flatten out the exact event that would have stopped you out, liquidated a crowded perp trade, or blown through a thin LP range.

Here is the practical consequence. Two tokens can show similar daily historical volatility, while one spends most of its risk inside short bursts during illiquid hours. For a DeFi trader, those are not the same asset. The second one carries more execution risk, more gap risk, and more danger if you rely on stops that assume continuous liquidity.

That is why a DeFi-native framework uses multiple lenses:

Here's a useful explainer for the mechanics:

Use one calculation for screening and another for execution.

Start with a rolling historical volatility series to compare assets and spot regime changes. Then add a range-based measure such as ATR if you need stop placement or intraday risk control. If you trade on-chain, add one more layer: check whether liquidity at your trade size stayed stable during the sample. Price volatility without liquidity context understates real risk.

For copy trading or wallet mirroring, match the volatility window to the wallet's behavior. A wallet that trades during deep US liquidity faces a different risk profile than one that enters during thin overnight rotations. Same token. Different realized volatility in practice.

The goal is not a perfect formula. The goal is a number that reflects the market you trade.

A token breaks out at 2:13 a.m. UTC. Price clears resistance, CT starts posting rockets, and the chart looks clean. Ten minutes later, the move retraces hard because the pool could not absorb size and the first push came from a handful of wallets, not broad participation. In DeFi, that kind of false read happens when traders measure volatility from price alone and ignore how the market trades on-chain.

Volatility matters when it changes execution. It should change whether you enter, how much size you carry, where the trade fails, and whether the opportunity is even worth touching.

Breakouts work better when expansion shows up in both price range and market participation. In practice, ATR is useful for judging whether a move has enough travel to justify the entry and for placing stops outside normal noise. A stop that sits too close to the breakout level gets clipped by routine churn. A stop that reflects recent range gives the trade room to work.

On-chain, one more filter matters. Check whether liquidity at your expected trade size is stable across the venues or pools you would use. A breakout in a deep market and a breakout in a shallow pool can print the same candle and carry very different risk.

A simple mini-case helps. A trader sees a token leave a long consolidation and wants the retest. Instead of anchoring the stop to a random chart line, they place it beyond recent range and verify that the pool did not thin out during the move. If range expands and depth holds, the breakout has a better foundation. If price breaks out but depth disappears, the move is easier to fade and harder to execute.

Sizing is where volatility measurement pays rent.

A high-beta token should usually get less notional size than a large-cap pair if the goal is to keep account risk consistent. That sounds basic, but many DeFi traders still size from conviction, wallet PnL, or how good the chart looks on first glance. In a 24/7 market, where liquidity can change by hour and weekends can trade very differently from weekday US sessions, static sizing gets expensive fast.

The practical approach is simple. Start with the amount of account risk you are willing to lose if the trade fails. Then back into position size using recent realized movement, expected stop distance, and current liquidity at your size. If slippage is likely to widen the loss beyond the chart stop, cut size again.

Different trades call for different volatility profiles.

For capital you want to preserve, lower realized volatility and steadier liquidity usually fit better than explosive upside stories. For directional trading, higher volatility can be attractive, but only if you can still get in and out without donating edge to slippage. For wallet mirroring, the match between asset behavior and wallet behavior matters as much as the chart.

That last point gets missed often. A sharp wallet can trade unstable names because it enters early, exits into strength, and tolerates noise. A follower who copies late often inherits the widest ranges and the worst fills. Measured volatility should shape which wallets you mirror and which tokens inside those wallets you ignore.

Volatility measurement is often more useful as an alert system than as a standalone trade signal.

Track a watchlist for volatility expansion after compression, sudden changes in intraday range, or a jump in failed breakout attempts. Then add DeFi-native triggers. Watch for liquidity leaving a pool, large holders rotating into or out of a token, or a burst of new wallet participation that changes the market's character.

For on-chain workflows, one option is Wallet Finder.ai, which tracks wallet activity, trades, and tokens across major ecosystems. That helps when a lagging volatility series is less informative than seeing the wallets you follow start to reposition before the next expansion phase.

Disciplined traders use volatility to improve trade mechanics.

A practical checklist looks like this:

Good traders can be wrong on direction and still survive. Traders who misread volatility and liquidity usually lose more than the chart suggested.

Volatility metrics are useful. They are not a crystal ball.

The first trap is assuming past volatility predicts future volatility cleanly. Sometimes volatility clusters and stays high. Sometimes it collapses right after a dramatic burst. A backward-looking measure can tell you what the market has been doing. It can't promise what the next hour will look like.

Another trap is false precision. Traders love clean numbers because they feel objective. But a volatility model built on weak inputs still gives a weak answer, just with more decimals.

Use volatility measurement to improve probabilities, not to manufacture certainty.

The right mindset is defensive and adaptive. Measure volatility so you can size better, place stops better, and know when not to trade. That's far more valuable than pretending any metric can tell you exactly where price goes next.

If you want to turn volatility measurement into something practical, Wallet Finder.ai gives you a way to track wallets, trades, and token activity across major chains so you can compare price behavior with what smart money is doing on-chain. That's the difference between reacting to volatility after the candle prints and spotting the conditions that often build before it.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.