Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

May 7, 2026

If you're sitting in stables, clipping low-risk yield, and waiting for crypto to pick a direction, you're already playing the same game that institutional cash desks play. The difference is scale, structure, and information quality.

BlackRock liquidity funds matter because they show where serious capital hides when risk appetite drops. For a DeFi trader, that makes them more than a TradFi curiosity. They’re a benchmark for what conservative capital accepts, a template for risk management, and a signal source when money rotates out of risk assets.

A common crypto setup looks like this: BTC is chopping, perp funding is noisy, and sitting in stables at 4% to 5% suddenly feels competitive again. That is the same capital-allocation problem institutional treasury desks solve with BlackRock liquidity funds. They are built for cash that needs to stay available, hold its value, and earn short-term rate income without reaching for risk.

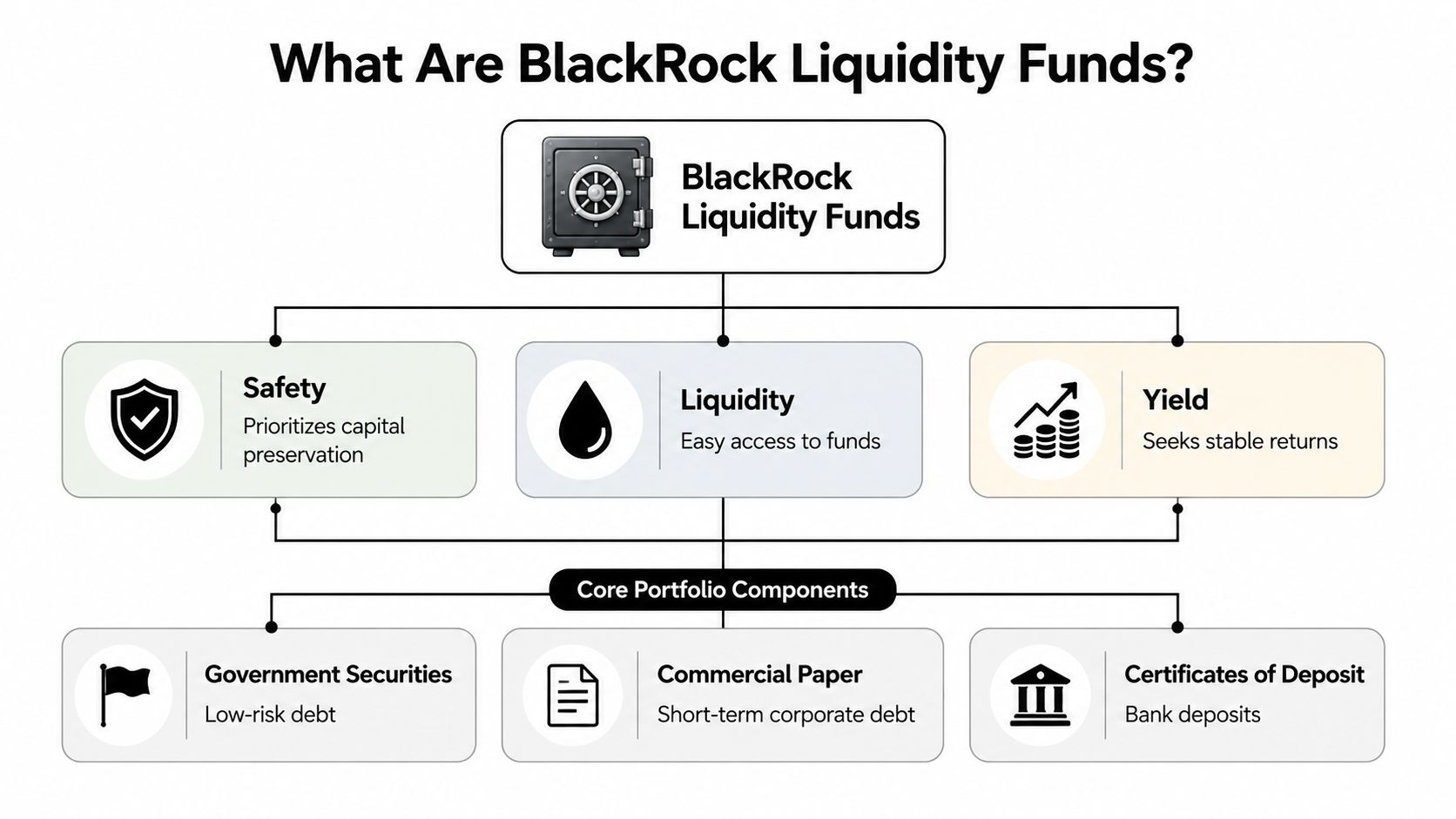

BlackRock liquidity funds are cash-management products that invest in very short-dated, high-quality instruments. The mandate is narrow by design: preserve principal, meet redemptions, and pass through money-market yield. For DeFi traders, the practical read is simple. These funds sit near the TradFi risk-free baseline that on-chain stablecoin products compete against.

Institutions park cash here because idle balances still need a job. A corporate treasury team may need same-day liquidity for payroll, margin, or operating expenses. An asset manager may need cash ready for subscriptions, redemptions, or collateral calls. In both cases, the goal is not maximizing return. The goal is keeping cash usable while collecting short-term yield.

A government-focused example is BlackRock Select Treasury Based Liquidity Fund (TFFXX). Its mandate limits holdings to cash, U.S. Treasury bills, notes, other government obligations, and qualifying overnight repo, with strict maturity limits. That structure matters more than the headline yield because it defines what kind of stress the fund is built to survive.

For a DeFi trader, that framing is useful because it sets the right comparison set. TFFXX is not competing with a high-beta farm or an incentive-heavy lending market. It competes with the decision to stay liquid and wait.

BlackRock liquidity funds are not all the same product with different labels. The portfolio mix drives the trade-off.

That distinction matters on-chain. If a tokenized Treasury vault is pulling demand while DeFi stablecoin yields are falling, conservative capital has a clear alternative. If flows favor products tied to government paper, risk appetite is usually tightening, not expanding.

My rule is straightforward: use BlackRock liquidity funds as a benchmark for defensive capital. Then compare any stablecoin vault, lending loop, or basis trade against that benchmark in plain terms. How much extra yield are you getting, what risk creates it, and how quickly can you exit if the market turns?

A DeFi trader parking dry powder for a week cares about one thing first. What yield can you earn without introducing a hidden liquidation path, governance surprise, or exit bottleneck?

BlackRock liquidity funds solve that with a simple mandate. They collect income from very short-dated instruments and keep the portfolio liquid enough to meet redemptions without dumping assets into a bad tape.

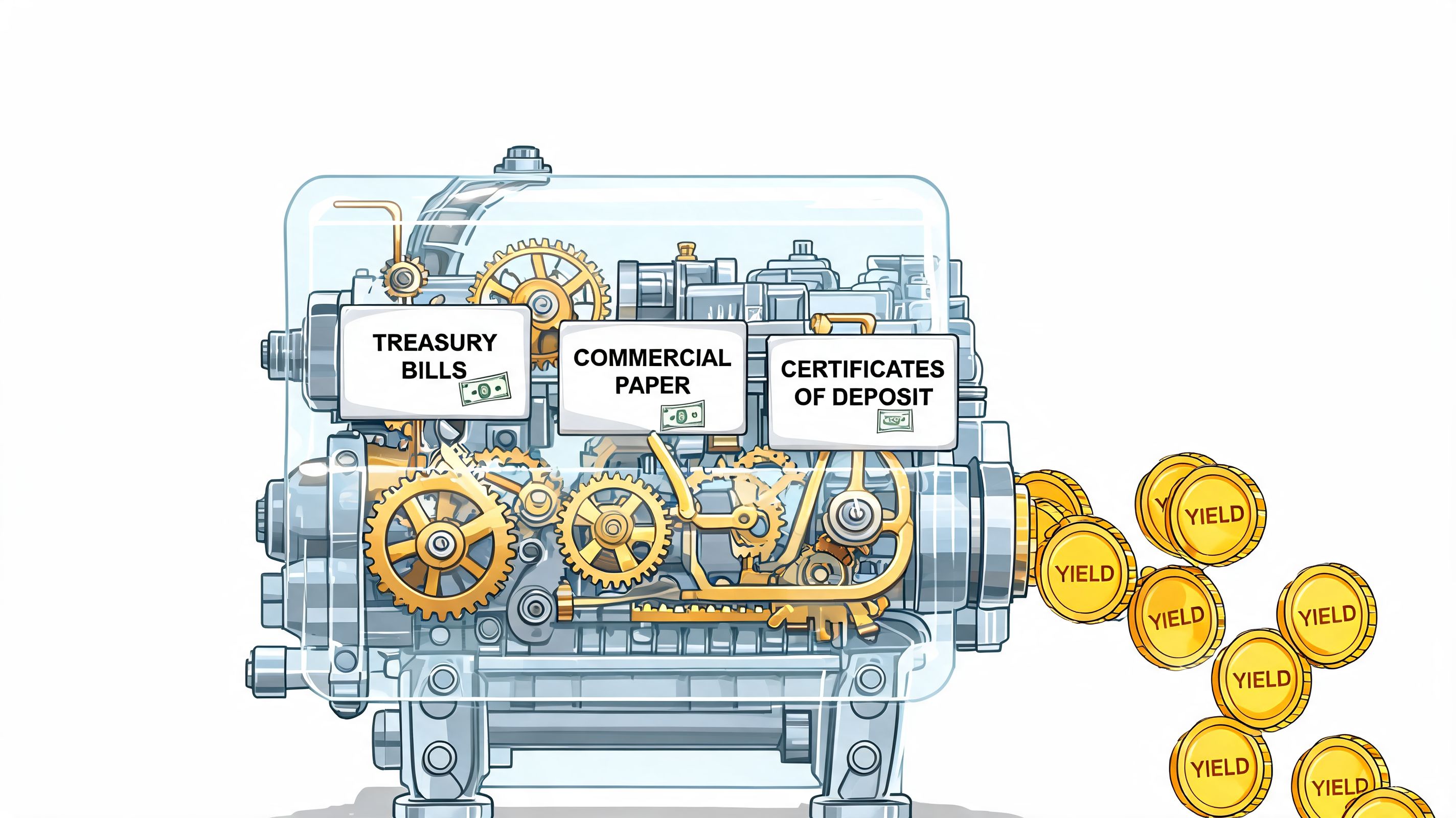

The income stream usually comes from three buckets:

The trade-off is clear. You get rate income and daily liquidity, but upside is capped because the portfolio stays short and conservative.

A practical reference point is the BlackRock Institutional Cash Series US Dollar Liquidity Fund. BlackRock’s fund materials for March 2025 show a portfolio built around high weekly liquidity and a short weighted average maturity, which is exactly what supports capital stability and same-day or next-day cash management in normal conditions. For current yield and portfolio details, the higher-quality source is BlackRock’s own cash product and fund information page, not a secondary commentary link.

That matters on-chain because this yield is policy-rate transmission, not protocol growth. If DeFi stablecoin yields fall toward money market fund levels, the case for taking smart contract and counterparty risk gets weaker. If you need a clean benchmark, compare any farm or lending venue against current stablecoin interest rates across major on-chain venues.

Two TradFi metrics deserve attention because they map well to DeFi risk.

| Metric | What it tells you | Why it matters |

|---|---|---|

| WAM | How quickly the portfolio resets on average | Lower WAM usually means lower sensitivity to rate moves |

| WAL | How long principal stays tied up on average | Lower WAL usually means a stronger liquidity profile |

WAM works like repricing speed. WAL is closer to capital lock duration.

A short maturity profile does two jobs at once. It keeps the fund close to a stable NAV framework, and it reduces the chance that managers need to sell longer paper at the wrong time to meet withdrawals.

If you want the real risk read, start with the maturity schedule, not the marketing label.

These funds produce stable yield because they stay disciplined:

The failure mode is just as clear. Stretch duration, add lower-quality credit, or rely on less liquid instruments, and the extra yield starts coming from risks that only show up under pressure.

That is the actionable signal. Treat BlackRock liquidity fund yields as the clean baseline for defensive capital. Any on-chain strategy paying more has to explain the spread. Sometimes that spread is worth taking. Sometimes it is just unpriced liquidity risk waiting for a busy redemption day or a sharp move in stablecoin demand.

Most DeFi traders don’t choose between “investing” and “not investing.” They choose between where idle capital sits. In practice, the menu is usually some mix of money market funds, centralized stablecoins, and on-chain lending or yield strategies.

That comparison gets sharper under stress.

A useful contrast comes from BlackRock’s own product mix. In March 2026, BlackRock’s $26B HPS Corporate Lending Fund (HLEND) gated redemptions, approving only about half of withdrawal requests. BlackRock’s regulated liquidity funds, by contrast, are designed for daily redemptions without that kind of gate, according to the BlackRock cash products material. Same manager, very different liquidity architecture.

| Vehicle | Typical Yield | Primary Risk | Regulation | Liquidity |

|---|---|---|---|---|

| BlackRock liquidity funds | Generally modest and tied to short-term rates | Interest-rate sensitivity, portfolio structure, operational fund constraints | Strong fund regulation | Designed for daily access, depending on fund terms |

| Centralized stablecoins | Often none by default unless deployed elsewhere | Issuer risk, reserve transparency, depeg risk, banking rails | Depends on issuer and jurisdiction | Usually highly liquid on-chain, but redemption access depends on issuer rails |

| DeFi lending protocols | Often higher but variable | Smart contract risk, collateral volatility, oracle risk, governance risk | Protocol-specific, not equivalent to money market fund regulation | Usually liquid until utilization, market stress, or pool design create friction |

BlackRock liquidity funds are strongest when your priority is capital preservation and predictable access. Stablecoins are strongest when your priority is settlement mobility. DeFi protocols are strongest when your priority is programmable yield and composability.

None of these replaces the others cleanly.

If you want a clean benchmark for whether on-chain cash deployment is worth it, compare it against conservative cash alternatives first. Wallet-level traders who monitor stablecoin interest rates across different crypto parking options usually make better decisions because they stop evaluating DeFi yield in a vacuum.

The mistake is comparing headline yield only. Compare redemption mechanics, collateral quality, and what happens when everyone wants out at once.

A risk desk cuts exposure on Monday, parks cash in short-duration vehicles on Tuesday, and DeFi traders only notice by Friday after perp open interest and alt beta roll over. That lag is the opportunity. BlackRock liquidity fund flows are useful because they show where large allocators want optionality, not because they predict any single token move.

Heavy inflows into liquidity funds usually signal defense first. Institutions are choosing immediate access, low duration, and cleaner collateral over reaching for extra return. For crypto, that tends to line up with slower rotation into high-beta assets, tighter risk budgets, and a stronger bid for stable parking.

The read-through is not mechanical. A cash allocation in TradFi does not produce an automatic sell signal for ETH, SOL, or DeFi governance tokens. But it does change the base rate. When large allocators prefer cash-like instruments, speculative capital usually becomes more selective across markets.

That matters because crypto often reacts late.

Outflows from conservative liquidity products often mean institutions are getting more comfortable extending duration or taking market risk somewhere else. Sometimes that supports a broader risk-on tape. Sometimes it only reflects rotation into slightly less defensive fixed-income positions. The distinction matters.

Use a simple filter:

A conservative cash vehicle can still see meaningful rotation as market preferences change, even when its mandate stays defensive, as noted earlier. That is the signal to watch. Not the fund in isolation, but the change in allocator behavior around it.

The practical edge comes from matching off-chain posture with wallet behavior on-chain. If institutions are moving toward cash and short duration, DeFi traders should ask where the crypto version of that preference shows up first.

Start with three checks:

Tools like Wallet Finder.ai become useful in practice. If TradFi flows suggest caution, I want to see whether smart-money wallets are increasing stablecoin balances, reducing directional token exposure, or parking funds in lower-volatility venues. For a practical process, pair fund-level context with on-chain fund flow analysis across protocols.

The edge is speed of interpretation. TradFi cash flow data gives you the posture. On-chain wallet tracking shows whether crypto natives are starting to express the same view.

If blackrock liquidity funds are the off-chain parking lot for cautious capital, your job is to find the on-chain echoes of the same behavior. You’re looking for rotation, not headlines.

That means watching where large wallets move stable assets, when they reduce exposure, and how quickly they re-enter risk once conditions improve.

A simple mistake is treating all stablecoin balances as neutral. They’re not. A stable balance sitting idle in a wallet, moving to an exchange, entering a lending market, or rotating into a tokenized Treasury wrapper each says something different.

What I watch first is behavioral intent:

Broad wallet tracking helps. Looking only at token prices makes you late. Looking at wallets gives you context before price confirms.

One of the best lessons from blackrock liquidity funds is that short duration is a feature, not a compromise.

BlackRock funds operating under SEC Rule 2a-7 keep WAM under 60 days, and on-chain analysts can borrow that mindset by filtering for DeFi vaults with similar short durations and stable 3% to 4% APYs, as noted in the SEC filing reference.

That gives you a practical filter:

| On-chain question | What to prefer |

|---|---|

| Is the yield source understandable? | Simple, short-horizon strategies |

| Can capital exit cleanly? | Vaults with clear liquidity terms |

| Does the yield depend on volatile incentives? | Prefer less emissions dependence |

| Is duration creeping higher than the cash sleeve should allow? | Keep cash-like capital short |

Desk habit: Build a separate stable-yield watchlist. Don’t mix your cash sleeve with your directional farming sleeve.

The strongest signal rarely comes from one wallet. It comes from clusters doing the same thing. If several experienced wallets start trimming risk, consolidating into stables, and pausing rotation into long-tail assets, that’s usually worth more than any single influencer thread.

A solid process looks like this:

If you want to sharpen this workflow, study a structured on-chain analysis process for wallet behavior and capital movement.

A quick visual walkthrough helps here:

The most reliable way to use these signals is as position-sizing input, not as a standalone trigger. If off-chain capital looks defensive and your tracked wallets are moving into stables or low-risk yield, that’s a reason to reduce aggression.

What doesn’t work is copying every stablecoin transfer as if it predicts a move. You need context:

The edge comes from combining three layers: macro cash posture, on-chain stable positioning, and wallet cluster behavior.

The line between TradFi and DeFi stops being theoretical as tokenized Treasury products bring conservative, real-world yield onto blockchains in a format that can plug into crypto infrastructure.

BlackRock’s BUIDL is the headline example. It matters because it turns a familiar institutional cash concept into an on-chain usable asset. For DeFi traders, that changes the menu. Conservative yield no longer has to stay entirely off-chain.

Tokenized Treasury exposure can reshape how traders think about reserve assets and collateral.

Instead of parking all non-directional capital in non-yielding stablecoins, market participants can use yield-bearing instruments that still fit into a digital asset workflow. That has obvious appeal for treasury managers, funds, and desks that want cash efficiency without stepping far out on the risk curve.

The broader tokenization discussion points in the same direction. A Federal Reserve Bank of New York research post noted that tokenized funds are already being used for secondary market liquidity, DeFi reserve assets, and collateral for derivatives, with BUIDL highlighted as the largest tokenized private fund at $2.5B AUM in that review, according to the New York Fed discussion of tokenized investment funds.

The opportunity is obvious:

The limit is also obvious. Tokenized Treasury products are not the same as permissionless native DeFi assets. They come with issuer structures, access rules, legal wrappers, and operational dependencies that pure on-chain assets don't.

That means traders should treat them as bridge assets, not as ideological replacements for DeFi.

Tokenized Treasuries matter most when they improve capital efficiency. They matter less if you expect them to behave like censorship-resistant bearer assets.

For a trader, BUIDL-style products fit best as part of the cash and collateral layer.

Use that lens:

That’s the practical takeaway. The growth of blackrock liquidity funds on-chain doesn’t eliminate DeFi. It gives DeFi a more serious benchmark.

Blackrock liquidity funds matter because they tell you what disciplined capital accepts in exchange for stability. That gives you a reference point every time a DeFi vault, lending market, or stable strategy offers higher yield.

The practical edge isn't in memorizing fund names. It's in learning how institutional cash behaves, then spotting when crypto wallets start behaving the same way.

If you do that consistently, you’ll size risk better, hold less dead capital, and avoid confusing fragile yield with safe yield.

If you want to track how smart money rotates between stables, exchanges, majors, and fresh narratives, Wallet Finder.ai gives you a cleaner way to do it. You can monitor profitable wallets, review full trading histories, build watchlists, and catch capital rotation faster instead of reacting after price already moved.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.