Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

March 10, 2026

Think of a crypto DeFi wallet as your personal key to the world of decentralized finance. It’s what gives you complete control over your own digital assets, sort of like a digital passport for the entire Web3 ecosystem. With it, you can plug into financial applications without ever needing a bank or a broker.

A DeFi wallet is so much more than just a place to stash your coins; it's the interactive tool that connects you directly to the blockchain. This is a huge shift from traditional finance apps, where a company is ultimately holding your money for you.

With a DeFi wallet, you are the only one with the keys. This is the core idea that lets you trade, lend, borrow, and earn interest entirely on your own terms.

This move toward self-sovereignty is what's fueling the massive growth in this space. It helps to understand how all the pieces of the Web3 world fit together, including how prominent DeFi wallets like MetaMask are enabling this new financial system.

To get started, you just need to grasp a few fundamental ideas. Nailing these down is the first real step toward navigating the DeFi world with confidence.

Here’s a quick breakdown of the terms you'll see over and over.

Four concepts sit at the foundation of every DeFi wallet, and getting comfortable with them early makes everything else in the space click into place.

The first is non-custodial ownership. This simply means that you, and only you, control the private keys to your funds. The wallet provider has no ability to access, freeze, or move your assets on your behalf. Unlike a bank account or an exchange account where a company holds your money and you hold a claim against it, a non-custodial wallet gives you direct, sovereign ownership of what is on-chain.

That ownership is secured by your private keys — a secret string of characters generated when your wallet is created, which proves ownership of your crypto and cryptographically authorizes every transaction you sign. Think of it as the ultimate password: whoever holds the private key controls the funds, no questions asked, no identity verification required. This is why keeping your private key confidential is non-negotiable.

Because a private key is long, complex, and easy to lose, DeFi wallets represent it in a more human-friendly form called a seed phrase: a list of 12 to 24 ordinary words generated in a specific order that serves as a master backup for your entire wallet. If your device is lost, stolen, or destroyed, entering your seed phrase into any compatible wallet application restores full access to your funds instantly. It is the only recovery mechanism available, which means its physical security matters enormously.

Finally, dApp interaction is what transforms a DeFi wallet from a simple storage tool into a gateway to an entire financial ecosystem. dApps — decentralized applications — are protocols that run on the blockchain and enable activities like swapping tokens, lending assets, borrowing against collateral, and providing liquidity to earn yield. Your wallet connects directly to these applications, authorizing each action with your private key, without any intermediary standing between you and the protocol.

These concepts might sound technical, but they all boil down to one thing: putting you in the driver's seat.

The growth here isn't just hype. As of early 2025, the Decentralized Finance (DeFi) ecosystem had locked up a total value of over $100 billion across countless blockchains. This explosion is powered by roughly 17.5 million unique DeFi users around the world who depend on these wallets to interact with protocols every single day.

Now that we’ve covered the basics, this guide will walk you through everything from advanced security practices to spotting profitable strategies, making sure you can operate safely and effectively in this exciting space.

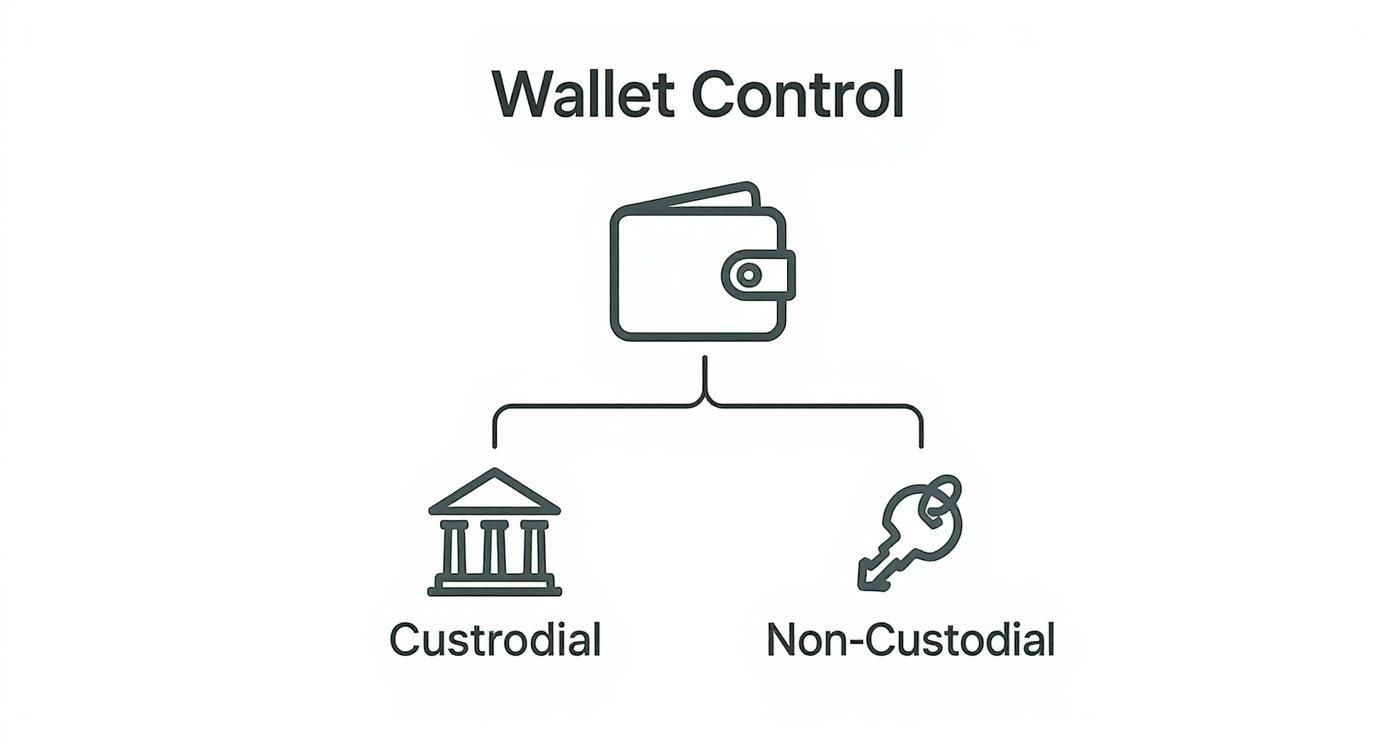

When you first jump into crypto, one of the first forks in the road you'll hit is choosing a wallet. The choice boils down to two camps: custodial or non-custodial. Think of a custodial wallet—like the one you get on a big exchange—as a bank’s safety deposit box. The bank holds your stuff for you and manages the keys. It’s convenient, sure, but you're ultimately trusting someone else with your assets.

A non-custodial crypto defi wallet, on the other hand, is your own personal safe. You, and only you, have the combination. This idea of self-sovereignty is the absolute bedrock of decentralized finance, perfectly summed up by the golden rule of crypto: "not your keys, not your crypto." This single difference changes everything about how you own and interact with your digital assets.

With a non-custodial wallet, your funds are secured by math on the blockchain, and they can only be moved with your private keys. This gives you final, undeniable control. No company can freeze your account. No government can seize your funds without those keys. No platform outage can block you from your money.

This is it. This is the core reason non-custodial wallets are non-negotiable for anyone serious about DeFi. You stop being just a "user" of a financial service and become the sovereign owner of your assets, free to plug into any part of the ecosystem without asking for permission.

This empowerment is a huge reason the market has grown so dramatically. The global crypto wallet market, which is dominated by these DeFi-ready wallets, was valued at around $4.18 billion in 2025 and is on track to hit nearly $56.74 billion by 2035. With roughly 65% of digital asset users already using crypto wallets to tap into DeFi, their role as the gateway to financial freedom is undeniable. You can dig into more of the numbers in these crypto wallet market projections and trends.

Getting a handle on the trade-offs between convenience and control is crucial. While custodial services are a simpler entry point for beginners, only non-custodial wallets give you the keys to the entire DeFi kingdom.

The fundamental divide between custodial and non-custodial wallets runs through every aspect of how you own and interact with your crypto, and understanding it in full is worth more than any individual security tip.

Private keys are where the difference begins. With a custodial wallet — the kind you get when you sign up for a centralized exchange — the exchange holds your private keys on your behalf. You have an account with a balance, not direct ownership of on-chain assets. With a non-custodial DeFi wallet, the private keys live with you and no one else, which means ownership is real and direct rather than a claim against a third party.

That key distinction flows directly into asset control. On a custodial platform, moving your funds requires the platform's cooperation. They can freeze withdrawals, suspend accounts, or restrict access entirely — and history has shown they sometimes do, whether due to regulatory pressure, insolvency, or internal policy. A non-custodial wallet answers to no one. You have direct and absolute control over your assets, and no external party can block a transaction you initiate.

Security is the trade-off where custodial wallets look most appealing at first glance. When an exchange holds your keys, their security team, infrastructure, and insurance bear the burden of protecting your funds. The downside is that you inherit all of their vulnerabilities too — if they get hacked, your funds are at risk through no fault of your own. With a non-custodial wallet, security responsibility sits entirely with you, which is a higher bar but one that cannot be breached by a third party's failure.

DeFi access is where the practical gap becomes impossible to ignore. Custodial wallets offer limited or nonexistent access to decentralized applications. At best, some exchanges provide curated DeFi features within their own interface, but you are interacting indirectly and only with what they choose to support. A non-custodial wallet connects directly to any dApp or protocol on the blockchain, with no gatekeeper deciding what you can or cannot use.

Recovery works differently in each model in a way that surprises many newcomers. A custodial account can be recovered through customer support — reset your password, verify your identity, and regain access. A non-custodial wallet has no customer support to call. Recovery depends entirely on your secret seed phrase. Lose it and your funds are gone permanently. Keep it safe and you can restore full access to your wallet on any device, anywhere in the world, without asking anyone's permission.

Censorship resistance is the final and perhaps most philosophically important dimension. Custodial accounts are susceptible to freezes, restrictions, and forced closures — governments can compel exchanges to block specific users, and exchanges can impose their own restrictions for any reason. A non-custodial wallet is highly resistant to all of this. As long as the blockchain runs and you hold your keys, no institution can prevent you from transacting.

When you lay it all out, the choice comes down to one question: Who do you trust to hold your money? For anyone venturing into DeFi, the only real answer is yourself.

The whole point of decentralized finance is to cut out the middlemen. You can't really be part of a permissionless world if you have to ask a third party for permission to use your own money.

Here's exactly why non-custodial wallets are the only way to fly in DeFi:

This freedom, of course, comes with the responsibility of keeping your seed phrase safe. But that’s a small price to pay for complete financial autonomy. When you embrace a non-custodial crypto defi wallet, you're not just storing crypto—you're unlocking an entirely new financial world.

Let's get one thing straight: not all DeFi wallets are built the same. The world of wallet tech is surprisingly deep, and picking the right one is a huge deal for both your security and your sanity. The first, and most important, split you need to understand is between wallets that are always online versus those that are kept completely offline.

This initial choice between "hot" and "cold" storage shapes everything about how you'll interact with your crypto. Are you a high-frequency trader who needs instant access, or are you looking to lock down your assets for the long haul? Your answer to that question will point you in the right direction.

This simple diagram really hammers home the core difference in wallet control—are you letting someone else hold your keys (custodial), or are you taking full ownership (non-custodial)?

As you can see, with a non-custodial wallet, you are the only one with the keys. That’s the entire foundation of self-sovereignty in DeFi.

Hot wallets are exactly what they sound like: software wallets that are always connected to the internet. They usually live on your computer as a browser extension or desktop app, or on your phone as a mobile app. Think of a hot wallet as your everyday spending cash—easy to get to and always ready for action.

Because they’re constantly online, hot wallets are the go-to for anyone actively participating in DeFi. Swapping tokens on a decentralized exchange (DEX), farming yields, or interacting with dApps all become frictionless. Their biggest selling point is pure convenience and speed.

Some of the most popular hot wallets you'll run into are:

But here’s the trade-off: that always-on convenience creates a much larger attack surface. This makes them a poor choice for storing the majority of your crypto portfolio.

On the other end of the spectrum, we have cold wallets. These are physical hardware devices that keep your private keys totally offline. A cold wallet only connects to the internet for the brief moment you need to sign a transaction, and even then, your private key never actually leaves the secure chip inside the device. It’s like keeping your life savings in a bank vault instead of your back pocket.

The core benefit of a cold wallet is that it isolates your keys from online threats like malware, viruses, and phishing attacks. This makes them the gold standard for securely storing large amounts of cryptocurrency over long periods.

Hardware wallets from brands like Ledger and Trezor are the industry leaders here. To send funds, you connect the device to your computer, verify the transaction details on the device’s tiny screen, and then physically press a button to give it the green light. That physical confirmation step is an incredibly powerful security layer.

Once you've got the hot vs. cold distinction down, you can start exploring some of the more advanced wallet types. These offer unique features that cater to serious traders, organizations, or anyone looking for next-level security.

Smart Contract Wallets

These wallets aren't just key containers; they are actual smart contracts living on the blockchain that you control. This opens up some powerful possibilities you won't find in a standard wallet.

Multi-Signature (Multisig) Wallets

A multisig wallet is a wallet that requires more than one private key to authorize a transaction. For example, a "2-of-3" multisig setup would have three authorized signers but requires approval from at least two of them to move any funds. This structure is a game-changer for:

By understanding these different wallet types, you can make a strategic choice that actually fits your goals—whether you’re an active trader, a long-term hodler, or a treasurer for a decentralized organization.

In DeFi, the old saying "be your own bank" is true, but it leaves out the most important part: you also have to be your own security guard. This is the trade-off for having complete control over your money. To protect your assets from the very real threats out there, you need to move beyond generic advice.

A structured security routine is your best defense. It replaces fear with confidence, giving you a clear framework to interact with DeFi protocols while keeping your funds safe. It's all about building specific, repeatable habits that shut down the most common ways people get hacked.

Your seed phrase—sometimes called a recovery phrase—is the single most critical piece of information you'll ever handle in crypto. It's the master key to everything. If someone else gets their hands on it, they can drain your wallet from anywhere on the planet.

The rule here is simple and absolute: never type your seed phrase into a computer, take a picture of it, or save it in a digital file. Think of it like a bar of pure gold; it belongs offline, stored physically, and completely cut off from any internet-connected device.

Consider these tried-and-true methods for keeping it safe:

Exposing this phrase is the number one reason people lose everything. Your discipline here is non-negotiable.

Good security isn't something you set up once and forget about; it's an ongoing practice. By making a few key habits part of your routine, you can dramatically lower your risk. The goal is to create layers of defense so that a single mistake doesn't wipe you out.

Here’s an actionable checklist to get you started:

Attackers are always getting smarter. Phishing scams, for instance, have become incredibly sophisticated, often creating perfect clones of legitimate DeFi websites to steal your credentials. These are a constant threat, and you can learn more about spotting them in our detailed guide on common DeFi wallet scams.

Another huge risk is the malicious contract approval. This happens when you sign what looks like a normal transaction, but you're actually giving a smart contract unlimited permission to spend one of your tokens. Hackers can then use that approval to drain all of that specific token from your wallet whenever they want.

By combining iron-clad seed phrase management with a hardware wallet and a disciplined routine, you build a powerful defense. This proactive approach is what allows you to operate in DeFi with both confidence and control.

Jumping into DeFi is way easier than it looks. It all starts with setting up your first non-custodial wallet, which is your personal gateway to this new financial world.

We'll walk through the process using a browser extension wallet like MetaMask or Rabby. These are the most common starting points for anyone using a desktop computer, and getting the setup right from the beginning is the foundation for everything you'll do in DeFi.

First things first, you need to pick a wallet and install it.

metamask.io or rabby.io. Do not just Google it and click the first ad you see. Scammers love to create fake ads that lead to phishing sites designed to steal your crypto.The installation takes just a couple of minutes, but what comes next is the single most important step in your entire crypto journey. Pay close attention.

After your password is set, the wallet will generate your Secret Recovery Phrase (often called a seed phrase). This is a list of 12 or 24 words that serves as the ultimate backup for your funds. If your computer crashes or you get a new one, this phrase is how you'll restore your wallet.

Your seed phrase is the master key to all your crypto. Its security is 100% your responsibility. If you lose it, your funds are gone forever. If someone else finds it, they can drain your wallet from anywhere in the world. There's no "forgot password" button or customer support line to call.

You need to store this phrase offline, immediately. Here’s how:

Okay, your wallet is set up and your phrase is safely tucked away. Now you're ready to actually use it by connecting to a dApp (decentralized application).

Follow these steps, and you’ll sidestep the common mistakes that catch so many newcomers. Your first experience in DeFi will be secure and successful, setting you up for the road ahead.

Every time you use your crypto defi wallet—whether you're swapping a token, interacting with a dApp, or just sending funds to a friend—you leave a permanent mark on the blockchain.

Think of the blockchain as a giant, transparent public ledger. Your wallet address acts like your account number, and every single transaction is a new line item recorded for anyone to see, forever.

This permanent, public record is your on-chain footprint. While your real-world identity isn't directly linked to your wallet, the entire history of its activity is an open book. This isn't a bug; it's a core feature of blockchain that unlocks incredible opportunities for analysis and research.

If you're new to this idea, it helps to understand what a digital footprint is in a broader sense. Just like your web browsing leaves a trail, your DeFi activity creates a verifiable and unchangeable history of every financial move you make.

This raw, public data is the goldmine that powers sophisticated on-chain analysis. Every successful trader, every crypto fund, and every market-moving "whale" leaves a trail of breadcrumbs on the blockchain. By digging into these on-chain footprints, you can start to reverse-engineer their strategies, spot new trends before they hit the mainstream, and find a real edge.

This is exactly where wallet tracking tools come in. Platforms like Wallet Finder.ai are built to cut through the noise of millions of daily transactions and highlight the signals that actually matter. They act like financial detectives, piecing together clues from the public ledger to show you who's winning and, more importantly, how they're doing it.

Here’s a look at how Wallet Finder.ai turns that messy on-chain data into a clean, actionable dashboard for discovering profitable wallets.

The platform automatically aggregates transactions to calculate key metrics like profit and loss, win rate, and the top-performing assets for any given wallet.

Turning raw blockchain data into strategic insights isn't magic. It's a methodical process of data aggregation and intelligent filtering.

The core idea is simple: if a wallet has a proven track record of making smart moves, its future actions are worth watching. By following the "smart money," you can gain insights that are typically only available to large institutional players.

This approach is becoming more and more common. In 2025, the number of active wallets used for DeFi hit around 198 million globally, making up nearly 24% of all crypto wallets. With cross-chain DeFi wallet transactions surging by 27%, the amount of on-chain data available for analysis is growing exponentially.

Of course, a fully transparent ledger raises valid questions about financial privacy. For users who want to minimize their on-chain footprint, our guide on blockchain privacy and obfuscation techniques is a great place to start. Understanding both the power and the pitfalls of on-chain transparency is key to navigating the DeFi world safely and effectively.

Setting up a crypto DeFi wallet and securing your seed phrase is only the beginning. The real reason most people want a DeFi wallet is what comes next: connecting it to a living, breathing ecosystem of protocols that can make your assets generate income around the clock. This is the part that traditional finance cannot offer — permissionless, programmable yield with no bank, broker, or minimum balance requirement standing between you and your money.

The landscape of on-chain yield strategies ranges from straightforward to genuinely complex. The key is understanding the mechanics well enough to choose the right strategy for your risk tolerance and experience level, rather than chasing the highest advertised number without understanding what drives it or what can go wrong.

This section walks through the core yield-generating strategies available from any crypto DeFi wallet, the risks specific to each, and a practical framework for building a yield approach that matches where you actually are as a DeFi user.

Lending protocols are the most straightforward starting point for wallet holders who want to put idle assets to work. Platforms like Aave and Compound allow you to deposit crypto assets into a smart-contract-managed pool, where borrowers can access those assets by putting up over-collateralized positions. In return for supplying the pool, you earn interest that accrues continuously, denominated in the same asset you deposited.

The appeal here is the simplicity of the risk profile. You deposit an asset — ETH, USDC, USDT, or a range of other supported tokens — and you receive a variable interest rate driven by market demand for borrowing that asset. When borrowing demand is high, rates rise. When demand falls, rates compress. You can withdraw your deposit at any time, since lending protocols maintain a buffer of liquid reserves. Your primary risks are smart contract vulnerability and, for volatile assets, the possibility that borrower liquidations fail to clear fast enough in a sharp market downturn, creating bad debt in the protocol. Established protocols with years of audit history and billions of dollars in total value locked carry meaningfully lower smart contract risk than newer, unaudited alternatives.

A subtlety worth understanding early: the difference between APR and APY. APR (Annual Percentage Rate) shows the base interest rate without compounding. APY (Annual Percentage Yield) shows the effective return when interest is compounded over the year. On lending platforms, interest accrues continuously, which means the APY is always slightly higher than the stated APR. When comparing yields across protocols, always verify whether the quoted figure is APR or APY to make a fair comparison.

Many lending protocols also distribute governance tokens as additional incentives for supplying liquidity. These token rewards are denominated in the protocol's native token and add to your effective yield, but they introduce a separate variable: the price of the governance token itself. A strategy that shows a 25% APY when governance token prices are elevated might show only 6% if those tokens depreciate. Always decompose the advertised yield into its base interest rate component and its token incentive component, and stress-test the strategy assuming the token incentive drops to zero.

Liquidity provision takes the yield-earning model a step further by deploying your assets directly into trading pools on decentralized exchanges (DEXs). When you provide liquidity to a pool on Uniswap, Curve, or a similar platform, you are enabling other traders to swap between the two assets in the pool. In exchange, you receive a proportional share of the trading fees generated every time someone uses the pool to make a swap.

The mechanics are important to understand before committing funds. Most liquidity pools require you to deposit two assets in a specific value ratio — for example, 50% ETH and 50% USDC. You receive LP tokens (liquidity provider tokens) representing your share of the pool. These LP tokens can themselves be staked in additional protocols to earn further rewards, a practice known as yield stacking, which is how experienced DeFi users build layered yield on a single capital base.

The central risk that every liquidity provider must understand is impermanent loss. This occurs when the prices of the two assets you deposited diverge from their ratio at the time of deposit. If you deposit ETH and USDC at a moment when ETH is worth $2,000 and ETH subsequently rises to $4,000, the pool's automatic rebalancing mechanism will have sold some of your ETH and bought more USDC to maintain the pool's ratio. When you withdraw, you will have less ETH than if you had simply held the asset outside the pool. The loss is called "impermanent" because it only crystallizes when you withdraw — if the price ratio returns to where it was when you deposited, the loss disappears. In practice, with highly volatile asset pairs, impermanent loss frequently exceeds the trading fees earned, turning a seemingly attractive yield strategy into an underperformance relative to simply holding.

The practical mitigation is to select your pool pairs based on correlation. Stablecoin-to-stablecoin pairs (USDC/USDT, DAI/USDC) experience near-zero impermanent loss because both assets maintain a stable peg to the same value. Stablecoin pools on Curve Finance, for example, are specifically optimized for this use case and offer trading fee yields with minimal impermanent loss exposure. They are the lowest-risk entry point for liquidity provision. Volatile-to-stable pairs (ETH/USDC) carry moderate impermanent loss risk but generally offset it with higher trading fees. Volatile-to-volatile pairs (ETH/BTC, ETH/SOL) carry the highest impermanent loss exposure and are appropriate only for users who have calculated their IL risk threshold explicitly rather than relying on headline APY numbers.

Once you are comfortable with the basics of lending and liquidity provision, yield aggregators represent the next step up in sophistication and efficiency. Platforms like Yearn Finance and Beefy Finance act as automated portfolio managers for your DeFi yield. You deposit an asset or LP token into an aggregator vault, and the vault's smart contracts automatically scan multiple protocols for the highest available yield, route your funds to the best opportunity, and compound your earned rewards back into your position — all without requiring manual intervention.

The compounding function alone provides a meaningful edge. Manually compounding yield farming rewards requires paying a gas fee for each transaction. Aggregators pool hundreds of users' positions and compound them in a single batch transaction, dramatically reducing the per-user gas cost and allowing rewards to be reinvested far more frequently than would be economical for an individual user acting alone. The mathematical impact of frequent compounding on long-run returns is substantial.

The trade-off is an additional smart contract layer. When you deposit into an aggregator vault, you are trusting not only the underlying protocol's smart contracts but also the aggregator's own contracts. This layering of smart contract risk is why established aggregators with long audit histories and transparent on-chain track records are strongly preferable to newer alternatives promising higher vault yields.

Rather than approaching on-chain yield as a single category, the most effective framework treats it as a risk spectrum with distinct tiers, each appropriate for a different allocation of your total DeFi capital.

Tier 1 — Capital Preservation with Modest Yield (Lowest Risk): Stablecoin lending on established protocols (Aave, Compound), and stablecoin liquidity provision on specialized stable-swap DEXs (Curve Finance). Expected yields typically range from 3% to 8% APY, with minimal impermanent loss exposure and low smart contract risk relative to newer alternatives. This tier is appropriate for the largest portion of your DeFi capital and for funds you cannot afford to lose.

Tier 2 — Balanced Yield with Manageable Risk: Lending of blue-chip volatile assets (ETH, WBTC) on established protocols, and liquidity provision in stable-to-volatile pairs on high-volume DEXs. Expected yields vary more widely (5% to 20% APY) depending on market conditions and fee generation, with meaningful but calculable impermanent loss risk. This tier is appropriate for capital you are comfortable with in medium-volatility environments.

Tier 3 — High Yield with Elevated Risk: Liquidity provision in volatile-to-volatile pairs, yield aggregator vaults on newer protocols, and leveraged yield farming strategies that borrow assets to amplify farming positions. Yields in this tier can be dramatic when conditions are favorable, but impermanent loss, smart contract risk, and liquidation risk are all significantly elevated. This tier is appropriate only for capital you are explicitly allocating to high-risk DeFi positions, sized accordingly.

Building your on-chain yield approach as a deliberate allocation across these tiers — rather than rotating your entire capital into whichever protocol is showing the highest number on any given day — is what separates disciplined DeFi participants from those who find their portfolio devastated by a single smart contract exploit or impermanent loss event.

One of the most underestimated dimensions of using a crypto DeFi wallet is the tax and record-keeping obligation that comes with every on-chain transaction. Most guides walk you through wallet setup, security practices, and yield strategies. Almost none of them explain what happens come tax time, when a year of DeFi activity — dozens or hundreds of transactions across multiple protocols and chains — needs to be accounted for accurately.

This is not a trivial concern. In most major jurisdictions, every cryptocurrency transaction is a potential taxable event, and DeFi introduces transaction types that have no clear parallel in traditional finance and no established, universal tax treatment. Getting this wrong exposes you not just to an incorrect return but to the compounded problem of trying to reconstruct months of on-chain history from scratch under time pressure.

Understanding your obligations and building a record-keeping system from day one is far less painful than discovering the problem after the fact. This section explains the key tax situations that arise from DeFi wallet activity and the practical tools available to manage them.

The foundational principle in most jurisdictions — including the United States, the United Kingdom, Australia, and most of the European Union — is that disposing of a cryptocurrency triggers a taxable event. "Disposing" means selling, swapping, spending, or otherwise transferring ownership in exchange for value. This principle creates tax implications across most of the common DeFi wallet actions that users take without thinking twice.

Token swaps on a DEX are the most common trigger. When you swap ETH for USDC on Uniswap, you have disposed of ETH at the market price at the moment of the swap. If you acquired that ETH at a lower price, the difference is a realized capital gain. The fact that you received USDC rather than fiat currency does not change this — the swap itself crystallizes the gain or loss. If you are making dozens of swaps per month while yield farming or trading, each one is a separate taxable event requiring its own cost basis calculation.

Yield farming rewards and lending interest are typically treated as ordinary income at the fair market value of the tokens at the moment they are received. This means that if you earn governance tokens as liquidity mining rewards and those tokens are worth $500 at the time they land in your wallet, you have $500 of ordinary income — regardless of whether you sell them, hold them, or whether their value subsequently drops to zero. The timing of recognition matters: receiving rewards is the taxable moment, not the moment you decide to sell or swap them.

Liquidity provision introduces a particularly complex scenario. When you deposit assets into a liquidity pool and receive LP tokens, tax authorities in most jurisdictions treat this as either a disposal of the deposited assets (triggering a capital gains event) or a non-taxable exchange depending on how the transaction is classified. When you later withdraw from the pool and receive back the underlying assets, that withdrawal may itself constitute a disposal. The LP tokens you hold in between have a cost basis that needs to be tracked separately. This two-step structure means that a single liquidity provision entry and exit can generate up to four separate taxable events depending on jurisdiction.

Gas fees are a frequently overlooked element of DeFi tax accounting. In most jurisdictions, gas fees paid to execute a transaction can be added to the cost basis of the asset acquired in that transaction (reducing your eventual capital gain) or treated as a capital loss deduction (when paid on a disposal transaction). Keeping granular records of every gas fee paid — which requires on-chain data, not just the net asset movements — is necessary for accurate cost basis calculation.

In traditional finance, your broker tracks your cost basis automatically and provides a year-end summary. In DeFi, every transaction is on-chain and public, but the computation of cost basis is entirely your responsibility. There is no bank statement, no consolidated year-end document from a DeFi protocol.

The challenge compounds when you consider that many DeFi users operate across multiple wallets, multiple chains, and dozens of protocols simultaneously. A single DeFi position might involve: an initial ETH purchase on a centralized exchange (establishing the cost basis of the ETH), a transfer of that ETH to a DeFi wallet (not itself a taxable event, but creating a tracking gap if the receiving wallet is not linked to the same record), a swap of ETH into a stablecoin (a potential disposal event), a deposit of that stablecoin into a lending protocol (possibly a disposal), daily accrual of interest (ordinary income events), and eventual withdrawal (possible disposal). Tracking this accurately in a spreadsheet for a year of active DeFi use is genuinely difficult.

The practical solution is on-chain tax software. Platforms like Koinly, CoinTracker, and TokenTax are built specifically to connect to blockchain addresses via read-only public key access, pull every transaction from all connected wallets across multiple chains, classify each transaction type, calculate cost basis using your jurisdiction's method (FIFO, LIFO, or specific identification), and generate the relevant tax forms. These tools do not eliminate the complexity of DeFi taxation, but they reduce it from "manually reconstructing a year of on-chain history" to "reviewing an automated classification and correcting any misidentified transaction types."

The single most important tax principle for DeFi wallet users is that record-keeping is dramatically easier to do in real time than retroactively. The cost basis of every asset you hold in your wallet was established at the moment you first acquired it. If you wait until the end of the year to connect your wallet to a tax platform, you will be relying on that platform's ability to reconstruct all of your historical transactions correctly — which is feasible for major chains but becomes significantly less reliable for newer chains, obscure tokens, and protocol interactions that tax software has not yet learned to classify.

Connect your wallet address to a tax tracking platform at the start of your DeFi journey and give it read-only access to your on-chain history. Check the transaction classifications periodically — monthly is sufficient for most users, weekly for active traders — and flag any misclassified entries. Common misclassifications include LP deposit and withdrawal transactions (often flagged as taxable swaps when they may be classified differently in your jurisdiction), cross-chain bridge transfers (which transfer asset ownership between chain-specific addresses and can be complex to classify), and staking reward events (which many platforms initially label incorrectly).

Maintain a separate record of the cost basis of your LP tokens. Most tax software handles this adequately for established pools on major chains, but unusual pool types and newer protocols frequently cause errors in LP token cost basis calculation. A simple spreadsheet tracking the date of LP token acquisition, the assets deposited, and their market values at deposit time takes minutes to maintain per transaction and can save hours of reconciliation later.

Document the purpose of each wallet address you control. If you have a hot wallet, a cold wallet, and a dedicated "burner" wallet for testing new protocols, maintain a simple record mapping each address to its function. This documentation helps both you and any tax professional you work with understand the flow of assets between your own wallets — which are internal transfers, not taxable events — versus assets moving to external parties, which are disposals.

The on-chain transparency that makes DeFi wallets powerful tools for tracking smart money and building wealth is the same transparency that makes DeFi activity visible to tax authorities. Approaching your record-keeping with the same discipline you bring to your security practices puts you in the best possible position regardless of how tax law in your jurisdiction continues to evolve.

Ready to track the wallets that are generating real on-chain returns and discover which DeFi strategies smart money is actually deploying? Wallet Finder.ai gives you real-time access to top-performing wallets across multiple chains, so you can follow the strategies that are actually working.

Jumping into DeFi always sparks a few questions. Even after you’ve got the basics down, you might still run into some practical what-ifs. Let's clear up some of the most common ones people ask when they're getting started with their first crypto DeFi wallet.

My goal here is to give you direct, no-nonsense answers so you can navigate the space with a bit more confidence.

Yes, you can—and honestly, you probably should. Using multiple wallets is a pro security move called compartmentalization. It’s all about separating your funds to limit your risk.

Here’s how a lot of seasoned users do it:

That way, if your active hot wallet ever gets compromised, your main stash remains completely safe and sound.

Don’t panic. With a non-custodial wallet, forgetting your password is a hassle, not a disaster. That password you set is just a local security measure; it only encrypts the wallet data on that one specific device. It's not the ultimate key to your funds.

If you lose it, you can simply uninstall and reinstall the wallet. During the new setup, you'll see an option like "Restore from seed phrase." Just punch in your 12 or 24-word recovery phrase, and voilà—your wallet, assets, and history are all back. This is exactly why your seed phrase is infinitely more important than any password.

The fact that you can restore your entire wallet on any device with just your seed phrase is the magic of self-custody. It's what gives you true ownership, independent of any single piece of hardware.

Think of a gas fee as the toll you pay to use a blockchain highway. It's a small charge that goes to the network's validators (the people running the computers) for processing and securing your transaction.

These fees are what keep the network running and secure. The price changes based on how busy the network is. When everyone is trying to make transactions at once, fees go up. When things are quiet, they drop back down.

No. This is one of the hardest and most important rules in crypto: once a transaction is confirmed on the blockchain, it is final and irreversible.

That permanence is a core feature of blockchain—it's what makes the ledger trustworthy. But it also means there's no central bank or customer service line to call if you make a mistake. So, always, always double-check the recipient's address and the amount before you hit that confirm button.

Impermanent loss is the reduction in value that occurs when you provide liquidity to a pool and the prices of your deposited assets change relative to each other. The pool's automated rebalancing mechanism continuously adjusts the ratio of the two assets to reflect price changes, which means that when one asset appreciates significantly, you end up with less of it when you withdraw than if you had simply held both assets outside the pool. The "loss" is the difference between what you would have had by holding and what you actually receive on withdrawal.

The most reliable way to minimize impermanent loss exposure is to choose liquidity pool pairs based on price correlation. Pools consisting of two assets that maintain a stable peg to the same value — such as USDC/USDT or DAI/USDC — experience near-zero impermanent loss because neither asset moves significantly in price relative to the other. This makes stablecoin pools the lowest-risk entry point for liquidity provision.

For pools containing one or more volatile assets, impermanent loss is unavoidable when prices move significantly. In these pools, your protection is the trading fee income generated by the pool. If the pool generates enough fee revenue to offset the impermanent loss on your position, your net return remains positive. High-volume pools on major DEXs with sustained trading activity tend to generate enough fee income to offset moderate impermanent loss, which is why experienced liquidity providers focus on selecting pools with proven volume rather than chasing the highest advertised APY in low-volume pools where fee income will not compensate for the loss.

In most major jurisdictions — including the United States, United Kingdom, Australia, and most EU member states — yes, swapping one cryptocurrency for another using your DeFi wallet is a taxable event. The tax treatment is generally the same as selling the asset you disposed of: you recognize a capital gain or loss equal to the difference between the asset's fair market value at the time of the swap and its cost basis (what you originally paid for it). The fact that you received another cryptocurrency rather than fiat currency does not change this.

This means that if you are actively yield farming, rotating between liquidity pools, or trading tokens through a DEX, each swap generates a separate taxable event requiring its own cost basis calculation. A year of active DeFi activity can easily produce hundreds of taxable transactions.

In addition to swap events, yield farming rewards and lending interest are generally treated as ordinary income in most jurisdictions, recognized at the fair market value of the tokens at the moment they are received — not at the moment you sell them. If you earn governance token rewards that are worth $1,000 when received and they subsequently drop in value to $200, you still owe tax on $1,000 of ordinary income for the year in which you received them.

The practical implication is that anyone using a DeFi wallet for more than occasional transactions should connect their wallet address to an on-chain tax tracking platform and maintain records throughout the year rather than attempting to reconstruct history at tax time. Note that this is general information and not legal or tax advice — consult a qualified tax professional familiar with cryptocurrency for guidance specific to your jurisdiction.

The most reliable approach is to use dedicated on-chain crypto tax and portfolio tracking software rather than attempting manual tracking in a spreadsheet. Platforms such as Koinly, CoinTracker, and TokenTax connect to your wallet addresses via read-only public key access, automatically import every transaction across multiple chains, classify each transaction type, and calculate your cost basis and realized gains or losses throughout the year.

The key steps for effective multi-wallet, multi-chain tracking are:

Add every wallet address you control — hot wallets, cold wallets, and any additional addresses you use for compartmentalization — to your tracking platform. Make sure to link addresses from every chain you use (Ethereum, Solana, Arbitrum, Base, and so on), because the software cannot connect the dots between chains automatically unless you add all of your addresses explicitly.

Review the automatic transaction classifications regularly rather than waiting until tax time. DeFi-specific transaction types — LP deposits and withdrawals, cross-chain bridge transfers, and protocol rewards — are frequently misclassified by automated software, especially for newer protocols or chains with limited historical data. Catching and correcting these classifications throughout the year is far less painful than reconciling a full year's worth of errors in one session.

Maintain a simple separate record of the assets deposited into any liquidity pool, their market values at the time of deposit, and the LP tokens received in return. Most tracking software handles this adequately for established pools, but documenting it independently provides a verification layer that is invaluable if your tax software produces output that does not match your expectations.

Platforms like Wallet Finder.ai can help you monitor the on-chain activity of your own wallets alongside the smart money wallets you follow for trading signals, giving you a unified view of what is happening across your on-chain positions.

Ready to turn on-chain footprints into actionable trading signals? Wallet Finder.ai helps you discover the most profitable wallets, track their every move, and get real-time alerts so you can act ahead of the market. Start your free trial today and see what the smart money is doing.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.