Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

May 23, 2026

A green PnL screenshot feels good until you ask the only question that matters. Could you do it again on purpose?

Most active on-chain traders have lived this. You finish the week up. One wallet rotation into a meme token exploded, a few swing trades in majors worked, and several smaller positions bled. Net result: positive. Diagnosis: unclear.

That's a dangerous place to operate from.

Raw profit and loss tells you what happened after the fact. It doesn't tell you whether you sized well, picked well, managed exits well, or merely caught one violent move that covered a pile of weak decisions. A wallet can look smart in a hot tape and fragile in a flat one. Without a way to separate those effects, you can't tell the difference between a process worth scaling and noise you were lucky to survive.

This matters even more in DeFi because the path of returns is messy. You're not just trading spot tokens. You're bridging, LPing, farming, rotating narratives, paying gas, eating slippage, and sometimes carrying positions across chains where the benchmark itself is unclear. Two wallets with similar PnL can come from completely different behaviors.

One trader made money because they repeatedly entered early in strong sectors and cut losers fast. Another made money because a single low-liquidity token went vertical before its lock-up period ended. Those are not the same skill set. They shouldn't be evaluated the same way.

That's where performance attribution becomes useful. It turns your wallet from a scoreboard into a diagnostic system. If you're already thinking seriously about benchmarking wallet performance against a relevant market baseline, attribution is the next step. It tells you whether your edge came from asset choice, position sizing, timing, exposure to a narrative, or constraints that shaped the portfolio without you realizing it.

A trader who ends the month in profit usually asks the wrong first question. They ask, “How much did I make?” The better question is, “What exactly produced that result?”

Take a simple wallet pattern. You ran five ideas. One memecoin ripped. One ETH trade was fine. Three smaller positions lost money slowly. The wallet finished green, so the month looks good. But if the winner was a low-conviction flyer and the losers came from your normal process, the PnL report is flattering you.

PnL summarizes outcomes after market moves, liquidity conditions, and execution have already done their work. It doesn't identify skill. It doesn't tell you whether returns came from:

Practical rule: If you can't explain why a profitable period worked, you don't yet know what to repeat.

That's why experienced traders treat green periods with suspicion. A positive month can hide weak sizing. A negative month can hide strong decision quality if the benchmark or factor backdrop was hostile. Attribution forces honesty.

Luck tends to show up as concentrated contribution from a small number of outsized outcomes. Skill tends to show up as repeatable patterns. Better entries in the same setup. Better hold discipline in the same category. Consistent outperformance versus an appropriate benchmark.

On-chain, this distinction matters because wallet histories are public and seductive. You can find a wallet with excellent realized gains and still fail badly by copying it if you don't know what drove those gains. Was it early access to a narrative, superior sizing, one-off token access, or repeatable trade construction?

Performance attribution gives you a way to answer that with more rigor.

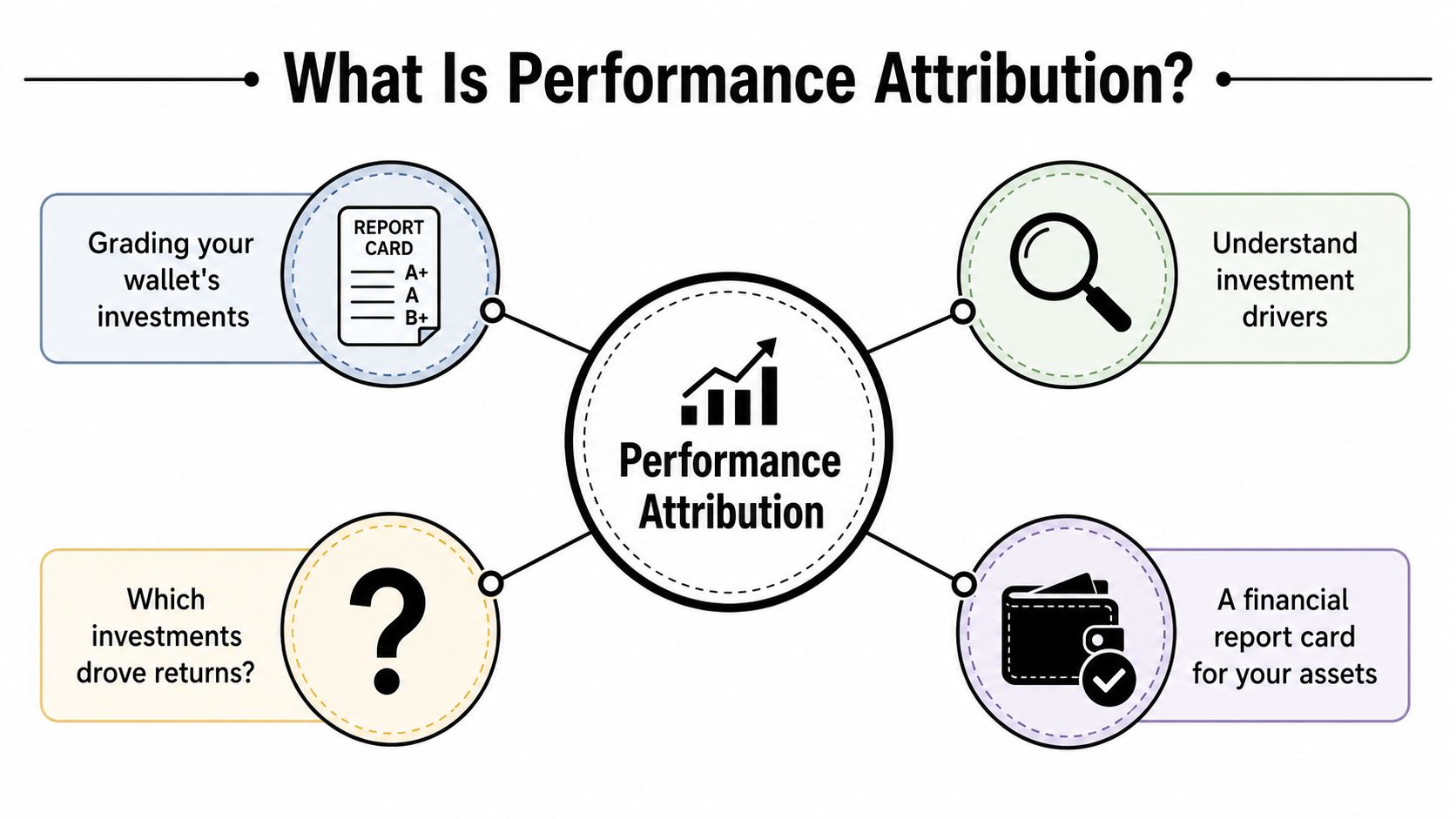

Performance attribution is a structured way to break portfolio results into decision-level drivers. For a trader, the simplest definition is this: it's a report card for your wallet.

It grades two core skills. First, did you choose the right assets? Second, did you size them correctly relative to a benchmark or alternative opportunity set?

A useful visual helps anchor the concept.

In institutional investing, performance attribution became a standardized concept largely through the Brinson, Hood, and Beebower framework published in 1986. CFA Institute's literature review describes that paper as “perhaps the most well-known paper on attribution” and notes that it gave its name to the Brinson model, which remains the most common equity attribution approach today. It decomposes active return versus a benchmark into allocation, selection, and interaction effects, rather than explaining total portfolio return on its own, as summarized in the CFA Institute review of performance attribution.

That benchmark-relative framing is the key point many crypto traders miss.

Attribution isn't just asking whether your wallet made money. It asks whether your wallet beat a relevant baseline, and if it did, why. If your alt basket outperformed a majors basket, was it because you overweighted the right sector, or because your token picks inside that sector were better? Those are different sources of edge.

You can think of the classic breakdown like this:

This is why performance attribution is more useful than a plain wallet leaderboard. A leaderboard tells you who won. Attribution tells you how they won.

Strong attribution often reveals that a trader's visible “alpha” is partly just exposure to a winning pocket of the market.

For on-chain research, attribution sharpens wallet analysis in three ways:

That turns wallet tracking from admiration into analysis.

Not every attribution method fits every trading style. The right choice depends on how active the wallet is, how clean your transaction history is, and whether your main problem is return decomposition or exposure diagnosis.

This is the simplest starting point. You take portfolio holdings at the beginning and end of a period, compare them with a benchmark, and estimate where excess return came from.

It's useful when you have periodic snapshots but not a clean transaction ledger. For public wallets, that can be enough to get directional answers. You can often tell whether a wallet was overweight memecoins, underweight majors, or concentrated in one narrative.

The weakness is obvious to any active trader. It smooths over path and timing. If the wallet traded in and out aggressively, a holdings snapshot can miss the actual decision process.

This is the method active traders usually want, even if they don't call it that. You reconstruct trades, cost basis, fees, and realized versus unrealized outcomes. Then you tie returns to actual entry, exit, and size changes over time.

It's harder. You need clean data, normalized token events, and sensible treatment of transfers, swaps, staking receipts, airdrops, and bridge activity. But when you get it right, this is the closest thing to the trading truth.

For a busy on-chain wallet, transaction-based attribution is often the only way to tell whether good results came from timing or from being in the right names eventually.

This method asks a different question. Instead of decomposing performance by holdings and categories alone, it decomposes returns by risk exposures or broad drivers.

That matters because return-only attribution can explain relative performance without explaining the risks that generated it. Industry analysis from SimCorp notes that returns-based methods such as Brinson don't reveal underlying return drivers or unintended exposures, while factor risk models decompose active risk and return into factor and specific components. In practice, that helps distinguish intended bets from hidden concentration or style exposure, as described in SimCorp's piece on breaking down performance attribution.

In crypto, factors aren't always formal in the equity sense, but the idea still works. You can model exposure to momentum, majors, beta to SOL ecosystem names, AI-token narrative concentration, exchange token sensitivity, or liquidity regime. A wallet may look like a strong selector when it was really just loaded with one factor that happened to lead.

| Method | Data Required | Accuracy | Best For |

|---|---|---|---|

| Holdings-based | Beginning and ending holdings, benchmark weights, category mapping | Moderate for slower portfolios, weaker for active trading | Swing portfolios, quick review, rough manager comparison |

| Transaction-based | Full transaction history, prices, fees, transfers, cost basis logic | High when data is clean | Active wallets, copy trading analysis, trade process review |

| Factor-based | Return series plus factor definitions or exposure model | High for exposure diagnosis, less direct for trade-by-trade review | Risk analysis, narrative exposure, hidden beta detection |

A practical rule works well:

If a wallet trades like a sniper, holdings may be enough. If it trades like a market maker with opinions, you need transaction-level reconstruction.

A strong workflow often combines them. Start with holdings-based to frame the period, move to transaction-based for real trade diagnosis, then add factor-based analysis if the wallet's risk profile still isn't clear.

The math behind performance attribution looks intimidating until you attach it to a small crypto example. Then it becomes manageable.

Assume a wallet holds ETH, SOL, and one memecoin. The benchmark is a simple majors basket. You group ETH and SOL as core layer-1 exposure, and the memecoin as speculative exposure.

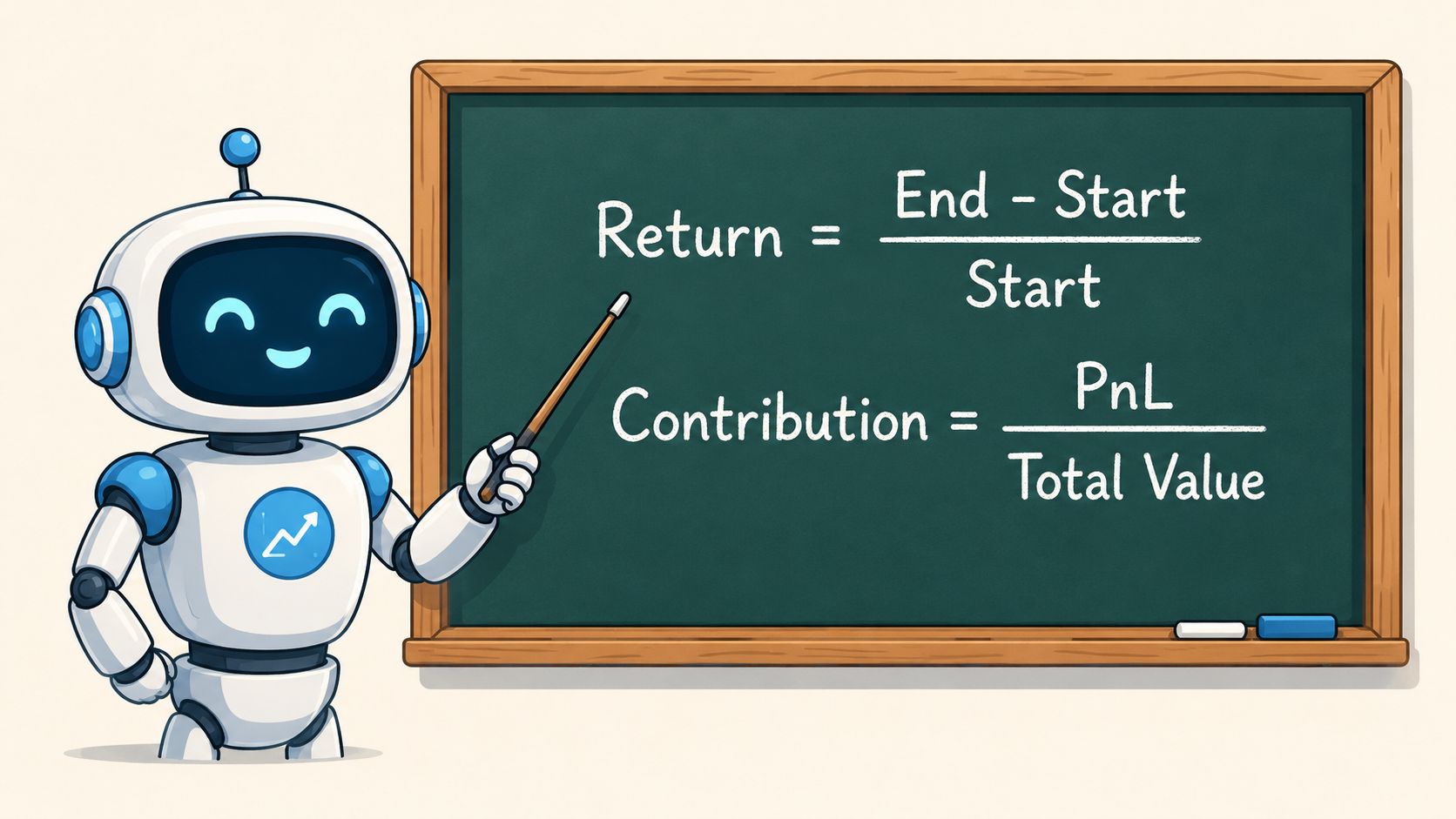

Start with the simplest building block. Contribution to return asks how much each position added or subtracted from overall portfolio return.

A practical expression is:

Contribution = portfolio weight × asset return

If SOL had a meaningful weight and rose sharply, its contribution will dominate. If the memecoin doubled but was tiny, its contribution may still be modest. This keeps you from overreacting to dramatic token-level moves that didn't matter much at the portfolio level.

Allocation effect measures whether your category weights helped relative to the benchmark.

A simple form is:

Allocation effect = (portfolio weight in category - benchmark weight in category) × benchmark category return

If you overweighted speculative tokens during a period when that category beat the benchmark, allocation helped. If you underweighted a winning category, allocation hurt.

This is a sizing question, not a token-picking question.

Selection effect isolates how well you picked assets within a category.

A simple form is:

Selection effect = benchmark category weight × (portfolio category return - benchmark category return)

Suppose your speculative bucket outperformed because you owned the stronger token inside that bucket. That shows up here. This is often the part traders care about most because it's the cleanest signal of judgment within an opportunity set.

Interaction captures the overlap between choosing the right category weight and choosing the right assets inside that category.

A simple expression is:

Interaction effect = (portfolio weight - benchmark weight) × (portfolio category return - benchmark category return)

When you overweight a category and also pick the best names inside it, interaction is positive. When you overweight the wrong category and still pick weak names, interaction turns against you.

Allocation asks, “Where did you place the chips?” Selection asks, “Which chips did you choose?”

These formulas are only useful if they change behavior. Here's how they map to actual decisions:

If you already track core profitability metrics for trading analysis, attribution adds the missing layer. It explains how those profitability outcomes were produced.

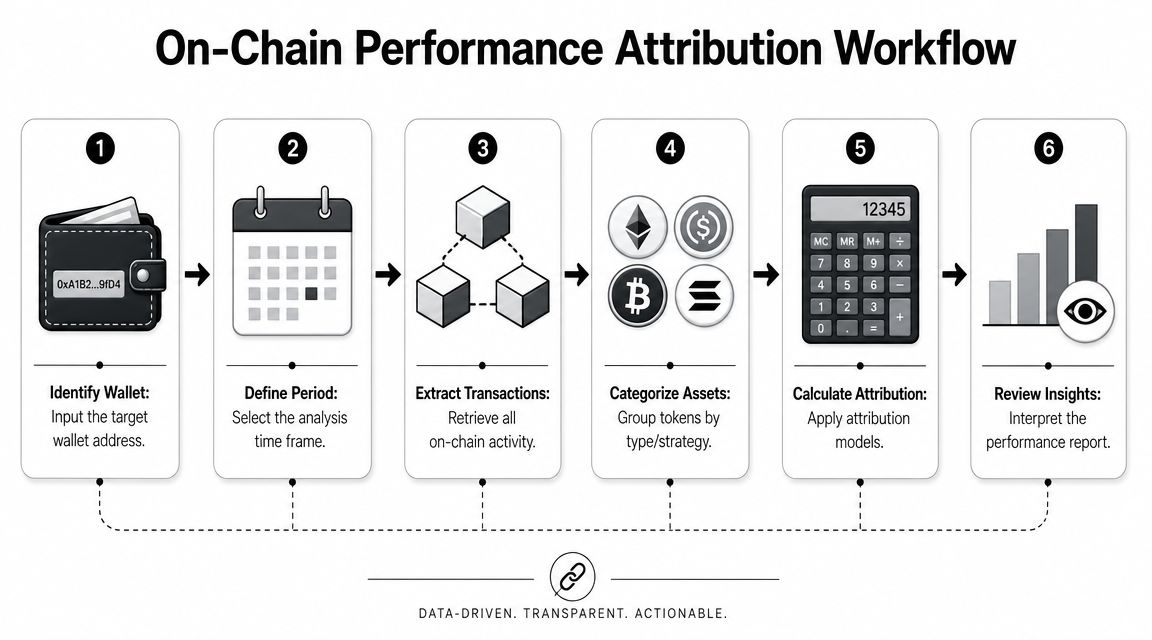

Running performance attribution on a public blockchain wallet is doable by hand. It's also more tedious than most traders expect.

The hard part isn't the theory. It's building a clean chain of evidence from raw on-chain activity to decision-level return drivers.

Start with the wallet and the period. Pick a clear date range and one wallet address. Don't analyze an address across multiple strategies unless you're prepared to segment them.

Then extract the full activity trail. For EVM wallets, that usually means token transfers, normal transactions, internal transactions, and swaps from a block explorer such as Etherscan, plus DEX-level details where needed. For Solana, you'll need equivalent parsed transaction data from a Solana-aware source.

The key is consistency. Attribution breaks when the data misses transfers, wraps, bridge events, or contract interactions that changed effective exposure.

Reconstruct PnL before trying to attribute it.

That means identifying:

A lot of wallet analysis stops too early. People sort trades by realized profit and call it insight. That's useful, but it's not attribution yet.

Create categories that match how crypto trades. Traditional sector tags don't help much on-chain. Group assets by something economically meaningful:

| Category approach | Example use |

|---|---|

| Narrative bucket | AI, memecoins, liquid staking, DeFi governance |

| Chain ecosystem | Ethereum, Solana, Base, Arbitrum |

| Strategy type | Perps collateral, spot swing, LP positions, farming |

| Risk bucket | Core, satellite, speculative, illiquid |

Different groupings answer different questions. If you're studying a copy trader, chain ecosystem may matter more. If you're reviewing your own book, strategy type might be more revealing.

Pick a benchmark that's close to the actual opportunity set. For a majors trader, a broad majors basket makes sense. For a Solana-native degen wallet, ETH-only benchmarking can be misleading. For thematic wallets, use a category-aware benchmark if you can build one.

Then calculate attribution. Apply contribution, allocation, selection, and interaction at the category level first. After that, drill down to token-level contribution inside each category.

A good on-chain attribution workflow moves from wallet, to category, to token, to transaction. Reversing that order usually creates noise.

The final review should answer a short list of trading questions:

That's the point where attribution becomes useful for copy trading, strategy review, and wallet ranking.

Most attribution errors don't come from bad formulas. They come from bad framing.

If the benchmark doesn't match the opportunity set, the output is cosmetically precise and economically wrong. Comparing a high-turnover memecoin wallet against a broad equity index would be absurd. Comparing it against a majors basket can also miss the point if the wallet lives entirely in one ecosystem and one risk regime.

A weak benchmark makes average behavior look like alpha or makes real skill disappear into the wrong comparison set.

On-chain trading has friction everywhere. Gas, routing quality, slippage, MEV exposure, bridge costs, and liquidity decay all shape realized outcomes.

If your attribution ignores those costs, you're evaluating an imaginary version of the wallet. This is especially dangerous when studying wallets that trade smaller caps. Gross selection may look excellent while net implementation quality is poor.

Traders often see a large interaction effect and treat it like proof of advanced skill. Sometimes it is. Sometimes it just means your biggest size happened to overlap with your strongest category return.

That overlap deserves interpretation, not celebration by default. Ask whether the position size came from a repeatable rule or from ad hoc conviction that happened to be right once.

This is the most overlooked issue in crypto attribution. Some return comes from what the wallet couldn't do.

Recent research highlighted by INFORMS proposes a framework for decomposing constrained portfolio outcomes into parts attributable to the unconstrained optimum, the constraints themselves, and the information embedded in those constraints. The practical takeaway is that some perceived alpha may come from rules such as no-shorting, borrowing limits, position limits, or other restrictions that removed bad choices rather than proving superior selection skill, as discussed in the INFORMS paper on constrained portfolio attribution.

In DeFi, constraints are everywhere even when traders don't label them that way. Wallets may avoid perps, refuse illiquid pools, cap position size by market cap, or only trade one chain because bridging is operationally messy. Those limits can improve results. That doesn't make the edge fake, but it does change the interpretation.

If you can't answer those questions cleanly, the attribution is still a draft.

Manual attribution works for one wallet and one period if you're patient. It breaks down fast when you're monitoring many wallets across chains.

The bottleneck is always the same. You spend most of your time cleaning data instead of analyzing behavior. Token transfers need interpretation. Cost basis has to be rebuilt. Swaps must be normalized. Position history needs to be reconciled before any benchmark-relative analysis can start.

That's why serious on-chain analysts eventually move toward tooling that handles ingestion, normalization, and wallet-level performance history for them.

A platform built for wallet analysis can shorten the path from raw transactions to usable attribution inputs. The useful outputs are the foundations you already need: token-level PnL, complete trading history, entry and exit timing, holding periods, win rates, position sizing patterns, and exportable data for offline research.

Those pieces matter because attribution isn't one metric. It's a layered analysis built on clean wallet history.

If you're comparing multiple smart money wallets, this kind of workflow also makes ranking more honest. You can start with a broad profitability screen, then inspect which wallets deserve deeper review based on consistency, category behavior, and sizing discipline. A practical place to start is a set of tools for wallet profitability benchmarking that helps narrow the field before you do the hard attribution work.

For DeFi traders, that's the shift that matters. You stop asking which wallet made money. You start asking which wallet made money in a way worth copying.

Wallet Finder.ai helps you do that work faster. If you want to analyze profitable wallets, inspect full trading histories, study token-level PnL, and build a cleaner performance attribution process from real on-chain behavior, explore Wallet Finder.ai.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.