Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

March 7, 2026

A crypto arbitrage scanner is your secret weapon for hunting down fleeting price differences across multiple exchanges. Think of it as an automated tool that constantly scours the market, looking for chances to buy a crypto asset low on one platform and sell it high on another. It does this thousands of times per second—a speed no human could ever match.

Before you even think about writing code, you need to get your head around why these opportunities exist in the first place. Price gaps in crypto aren't just random glitches. They're a natural byproduct of a fragmented and wild market. When you build a scanner, you're essentially building a system to systematically cash in on these temporary inefficiencies.

So, what causes them? Here are the primary drivers:

Your scanner's logic needs to be laser-focused on specific types of opportunities. While there are tons of complex strategies out there, most arbitrage plays fall into a few key buckets. It's best to start with the fundamentals.

Let's break down the most common arbitrage strategies your scanner will be designed to find. Each has a unique mechanism and presents a different kind of opportunity in the market.

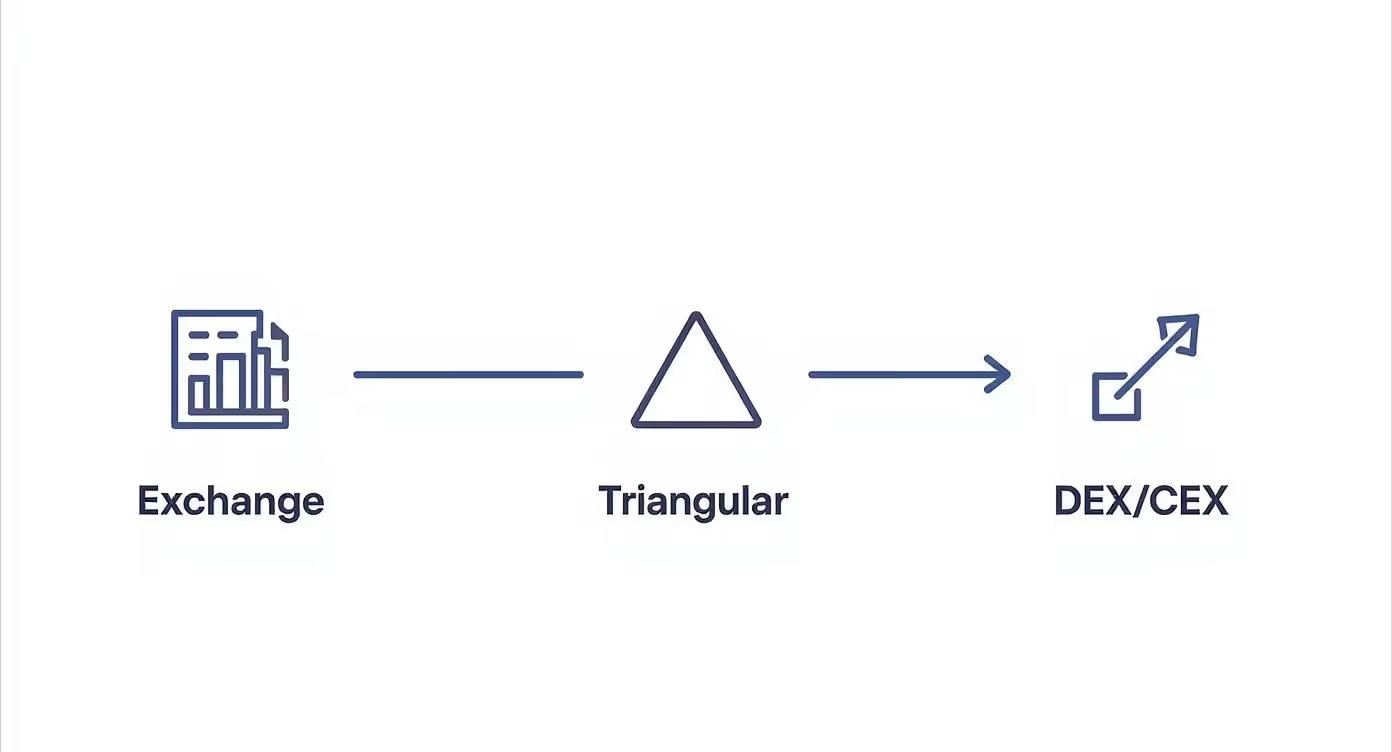

Arbitrage TypeMechanismExample ScenarioSimple Cross-ExchangeBuying an asset on Exchange A and immediately selling it for a higher price on Exchange B.Your scanner finds BTC is priced at $60,000 on Coinbase but is trading for $60,050 on Kraken. The play is to buy on Coinbase and sell on Kraken.Triangular ArbitrageExploiting a price discrepancy between three assets on a single exchange to make a profit through a circular trade.On a single exchange, you trade BTC for ETH, then that ETH for ADA, and finally trade the ADA back to BTC, ending up with more BTC than you started with.DEX-to-CEX ArbitrageCapitalizing on price differences between a decentralized exchange (DEX) and a centralized exchange (CEX).The price of LINK on Uniswap (a DEX) might temporarily lag behind the price on KuCoin (a CEX), creating a gap you can exploit.

These are the foundational plays. Mastering their detection is the first major step in building a profitable scanner.

The bottom line is that trying to find these opportunities manually is a losing game. The profit windows can last for just a few seconds, sometimes even milliseconds. A well-built scanner is the only way to spot these fleeting chances that are completely invisible to the naked eye.

In today's market, speed is everything. Crypto arbitrage is still a perfectly viable strategy in 2025, but the market has gotten way more efficient, squeezing profit margins down to the bone. This has made manual trading for most of these strategies flat-out impossible.

You’re not just competing against other traders; you're competing against their bots. Sophisticated tools can scan dozens of exchanges across multiple blockchains at once, and that's the level you need to be at. As this trader's guide for 2025 explains, managing fees and execution speed is now critical. An automated scanner isn't just a "nice-to-have"—it's the only way to get the edge you need to compete.

A crypto arbitrage scanner is only as good as the data it eats. Your algorithm can be a work of art, but if it's fed slow, unreliable information, you’re building on a foundation of sand. Designing a high-speed data pipeline isn't just a technical exercise—it's the first real step in turning a theoretical strategy into a system that actually hunts for profit. To understand how to safely manage funds and interact with decentralized platforms, What Is a DeFi Wallet? Your Guide to Web3 Finance provides a clear, beginner-friendly overview.

Think of this architecture as the central nervous system for your entire trading operation. Its job is to take the chaotic, noisy world of crypto markets and translate it into a structured format your scanner can act on in milliseconds.

Your first big decision is where to get your price data. This choice has massive ripple effects on the speed and reliability of your whole setup. You've got a few options, each with its own set of trade-offs.

WebSocket APIs are the gold standard for real-time CEX price feeds. Data is pushed directly to your scanner the instant a price changes, giving you ultra-low latency that polling methods simply cannot match. The catch is that managing persistent WebSocket connections takes real engineering effort — you need robust reconnection logic, heartbeat monitoring, and the ability to handle sudden bursts of data without your pipeline backing up. For any live arbitrage strategy, though, this complexity is non-negotiable. WebSockets are how you stay competitive.

REST APIs are the simpler option, and that simplicity comes at a cost. You send a request, you get a response, and then you wait before you can ask again — which means your data is always slightly stale, and exchange rate limits put a hard ceiling on how frequently you can refresh it. This makes REST perfectly adequate for pulling historical trade data, order book snapshots for backtesting, and non-urgent reference data like fee schedules. What it is not suited for is live signal generation. If you're relying on REST for real-time price comparisons, you're already behind.

Direct Node Access is the most powerful option and the most demanding to build. By running your own node — or connecting directly to a provider with raw mempool access — you can see pending transactions before they are confirmed on-chain. For DEX arbitrage in particular, this is the ultimate speed advantage: you can detect a large incoming swap that will shift a pool's price before that transaction lands in a block, giving you time to position your own trade to capture the spread it creates. The trade-off is significant hardware and infrastructure overhead, plus the engineering complexity of parsing raw transaction data in real time. If you want to dig deeper into how latency affects your bottom line at this level, it's worth analyzing latency in crypto trading patterns before committing to this path.

In practice, a production scanner uses all three in combination. WebSockets handle your live CEX price feeds. REST handles periodic reference data. Direct node access powers your on-chain DEX monitoring. The data pipeline you build needs to be flexible enough to ingest all three formats and normalize them into a single, consistent stream your detection logic can act on without caring where the data came from.

The visual below breaks down the different kinds of arbitrage opportunities your data pipeline needs to be able to feed.

As you can see, your data ingestion has to be flexible enough to spot opportunities, whether they happen on a single exchange or across multiple platforms at once.

In the arbitrage game, latency is the silent killer of profits. An opportunity that flashes into existence for 500 milliseconds is ancient history by the time your scanner sees it a full second later. Every single millisecond you can shave off your data pipeline is a direct competitive edge.

Your only goal here is to shrink the time between a price changing on an exchange and your scanner detecting it. A difference of just 10-20 milliseconds can be the deciding factor between capturing a profit and missing out completely.

One of the most powerful ways to fight latency is server co-location. This means renting server space in the exact same data center where an exchange houses its own servers. By physically putting your scanner next door to the exchange's matching engine, you cut network travel time down to the bare minimum. If you want to go deeper on this, it's worth analyzing latency in crypto trading patterns to really understand its impact on your bottom line.

Once you have your data sources locked in, you need a system to process all that information. A firehose of raw data is useless; it needs to be ingested, standardized, and analyzed methodically.

Here is a step-by-step actionable plan for your data pipeline:

BTC/USDT from Binance will look different from Kraken's. Your normalization stage must take all this messy, inconsistent data and convert it into a single, clean format that your core logic can easily work with.Alright, you've got a high-speed data pipeline humming along. Now it's time to build the engine room of your crypto arbitrage scanner—the part that turns a firehose of market data into real, actionable trading signals. This detection logic is the brains of the operation, tasked with spotting those fleeting price discrepancies in all the market noise.

We'll start with the most straightforward type of arbitrage and then ramp up to more complex strategies. While each algorithm uses a different mathematical approach, the core goal is always the same: find a circular path for your capital that leaves you with more than you started with, even after paying all the fees.

This isn't a niche hobby anymore. The global algorithmic trading market, which crypto arbitrage is a big part of, is expected to reach around $42.99 billion by 2030. That growth is fueled by sophisticated systems that can spot complex patterns humans would miss entirely.

This is the classic arbitrage play and the easiest place to start coding. The logic is simple: compare the price to buy a coin on one exchange with the price to sell it on another. You're hunting for moments where the ask price (the lowest sell price) on Exchange A is less than the bid price (the highest buy price) on Exchange B.

The basic formula is straightforward:

Profit = (Bid_Price_Exchange_B * Quantity) - (Ask_Price_Exchange_A * Quantity) - Total_Fees

But the real challenge is in that Total_Fees variable. It's not just one number; it's a messy combination of costs you absolutely must account for:

Your scanner's logic needs to be constantly pulling the latest fee schedules from each exchange's API. It has to bake those fees into every single calculation. Skipping this step is the fastest way to watch a "profitable" trade turn into a guaranteed loss.

Triangular arbitrage gets a bit more complex. It all happens on a single exchange, using three different currency pairs to exploit a pricing imbalance. Say you start with BTC and want to end up with more BTC. The trade loop might look something like this:

If the final BTC amount is higher than what you started with, you've found an opportunity. The calculation involves chaining the exchange rates for each pair. For a BTC -> ETH -> USDT -> BTC loop, the pseudocode to check this would be:

Amount_ETH = Start_BTC * Price_ETH/BTCAmount_USDT = Amount_ETH * Price_USDT/ETHFinal_BTC = Amount_USDT / Price_USDT/BTC

If Final_BTC > Start_BTC, an opportunity exists.

Of course, you have to subtract the trading fees for all three trades from your final profit. The good news is you avoid withdrawal fees since it's all on one exchange. The bad news is you're paying three separate trading fees.

Key Insight: Triangular arbitrage opportunities are incredibly brief—often lasting for mere seconds. They pop up from momentary imbalances in three different order books, and other bots pounce on them instantly. This means your data latency and execution speed have to be top-notch.

Mixing centralized and decentralized exchanges is where things get really interesting. This type of arbitrage brings a whole new set of headaches, mostly around liquidity and price impact. On a CEX, you have a nice, clean order book. On a DEX, the price is set by the ratio of tokens in a liquidity pool.

This means your scanner has to grapple with two huge variables:

Effectively analyzing liquidity flows for cross-chain arbitrage is a skill in itself. Your code has to look beyond simple price tickers and truly understand the on-chain environment, treating liquidity as a constantly changing variable, not a fixed number.

To help you decide where to focus your coding efforts, here’s a quick breakdown of the three logic types we’ve discussed. Each has its own trade-offs between simplicity and potential reward.

AlgorithmComplexityTypical Profit MarginKey ChallengeCross-ExchangeLow0.2% - 1.5%Managing withdrawal fees and transfer times.TriangularMedium0.1% - 0.75%Extreme speed requirements and fee calculation across three trades.CEX vs DEXHighVaries widelyAccurately predicting price impact and volatile gas fees.

For most builders, starting with cross-exchange logic is the most practical path. Once you've nailed that down, you can build on your existing framework to tackle the more demanding logic needed for triangular and DEX-based strategies.

Let's be blunt: deploying an untested algorithm with real money is just gambling. Before your crypto arbitrage scanner even sniffs a live market, it needs to go through a brutal trial by fire in a simulated environment. This is where backtesting—running your scanner against historical market data—becomes your single most important risk management tool.

Building a solid backtesting environment isn't about fancy code; it's about creating an honest simulation. The goal is to get a realistic preview of how your logic would have performed in the past, warts and all. A good backtest doesn't just flash potential profits. It shines a harsh light on flawed logic, uncovers hidden bugs, and forces you to confront the real-world costs that can bleed a seemingly great strategy dry.

The heart of your backtesting setup is its data. Garbage in, garbage out. You need high-fidelity, granular historical data that accurately mirrors the market conditions you want to test. This means getting your hands on tick-by-tick order book data, not just simple candlestick charts.

Here is an actionable checklist for setting up your backtesting environment:

For anyone working with on-chain data, building a reliable testing environment comes with its own unique set of headaches. To get a better handle on them, our guide on scalable backtesting for DeFi challenges and fixes dives much deeper into this complex process.

A backtest that only compares entry and exit prices is worse than useless—it's dangerously misleading. Real-world trading is filled with "frictions," which are the costs and delays that systematically chew away at your profits. Your simulation has to account for these with brutal honesty.

The most common failure point I see in new arbitrage systems is underestimating transaction costs. A strategy that looks like a goldmine on paper can instantly become a money pit once you factor in the true cost of execution.

Your model absolutely must include variables for:

Finally, your backtesting phase is the perfect time to validate your scanner's built-in safety features. Think of these as the circuit breakers that protect your capital when markets get chaotic or your own logic goes haywire.

Here are two non-negotiable safety nets to build and test relentlessly:

So, you've built and backtested your arbitrage scanner. The signals are looking sharp. Now for the exciting part: bridging the gap between those alerts and actual, live trades. This is where you decide just how much you want to let the machine take over.

The biggest fork in the road is your execution model. Are you going to run a semi-automated setup, where the scanner just alerts you and you pull the trigger manually? Or are you ready to go fully automated, letting your system trade on its own without any human input?

Honestly, there’s no right or wrong answer here. It all comes down to your comfort level with the tech and your tolerance for risk. Starting with a semi-automated approach is a great way to dip your toes in. It lets you build confidence in your scanner's signals while keeping the final say on every single trade.

But let's be real: in a market where the best opportunities vanish in milliseconds, manual execution is often just too slow. That's where a fully automated system shines, offering near-instant speed. If you're ready for that leap, you'll be looking at integrating with exchange APIs to place market or limit orders programmatically.

Here’s a quick breakdown to help you decide:

FeatureSemi-Automated SystemFully Automated SystemExecution SpeedSlower; you're limited by human reaction time.Near-instant; only bottleneck is API latency.Control LevelHigh; you approve every single trade.Low; the system acts on its pre-set logic.Risk of ErrorProne to manual errors (think fat-fingering an order size).Risk of a code bug causing rapid, unintended trades.Best ForNewcomers building trust in their scanner's logic.Experienced traders who have nailed down their risk controls.

Just spotting a price difference isn't enough to make you money. A truly great arbitrage system doesn't just find more opportunities—it finds better ones. The real secret sauce is in the signal filtering, where you enrich your scanner's raw output with outside data to confirm a trade's potential.

This means layering in other data points to make sure an arbitrage gap is legitimate and not just market noise. For instance, before firing off a trade, your system could quickly check for a sudden spike in gas fees or unusually low liquidity in a DEX pool. Both are huge red flags that could turn a profitable trade into a losing one.

The goal is to create confluence—where multiple, independent data points all scream that an opportunity is solid. You're moving from a simple system that sees a price gap to a smarter one that understands the context around that gap.

One of the most potent filtering techniques is tracking the on-chain moves of proven, profitable traders—what many call "smart money." By keeping an eye on the wallets of top performers, you can see what they're buying and selling in real time.

This adds a powerful validation layer to your scanner. Let's say your system flags a CEX-to-DEX arbitrage for a particular token. Before executing, it could cross-check that signal against a watchlist of smart money wallets using a tool like Wallet Finder.ai. If you see that several of these top-tier wallets have also recently bought that same token on the DEX, it adds a massive dose of confidence to your signal.

This is how you cut through the low-probability noise and zero in on trades that have already caught the attention of successful market players.

The tooling in this space has exploded, especially in 2025. The best crypto arbitrage scanners now cover dozens of blockchains and exchanges, giving traders an incredible edge. As you can read more about these developments, some traders are hitting consistent daily growth by using AI-powered systems to run hundreds of trades a day—a scale that's flat-out impossible for a human. By combining your custom scanner with these broader market insights, you're building a system that hunts for high-probability trades backed by real, observable market momentum.

Once your scanner is live and generating signals, you've crossed the threshold most builders never reach. But being live and being consistently profitable are two different things. The difference between a scanner that breaks even and one that compounds real returns comes down to three layers of optimization that most tutorials never cover: protecting your trades from Miner Extractable Value (MEV) attacks, monitoring the mempool to see opportunities before they're confirmed, and building a dynamic gas strategy that stops fees from quietly eating your edge. These aren't advanced extras — in 2025's competitive on-chain environment, they're the baseline for any scanner that touches DEX arbitrage.

MEV is one of the most misunderstood threats to DEX arbitrage profitability. At its core, it refers to the profit that block producers — miners on Proof-of-Work chains and validators on Proof-of-Stake chains — can extract by reordering, inserting, or censoring transactions within a block they are assembling. For your arbitrage scanner, this creates a specific and very costly attack pattern called frontrunning: a searcher bot detects your pending arbitrage transaction in the public mempool, copies your logic, and submits an identical trade with a higher gas fee to jump ahead of you in the same block. The searcher captures the profit your scanner identified; you get a transaction that often executes at a worse price or fails entirely, but you still pay the gas.

The most practical protection available to independent arbitrage scanner builders is using a private transaction relay to submit your trades. Services like Flashbots Protect on Ethereum route your transactions directly to block builders without broadcasting them to the public mempool, which is where frontrunning bots trawl for opportunities. Your transaction is invisible to searchers until it is already included in a block, eliminating the window during which it can be observed and front-run. The trade-off is a slightly longer inclusion time compared to public mempool broadcasting in low-congestion periods, but for most arbitrage strategies the MEV protection value far exceeds the latency cost because a frontrun transaction that fails still costs you gas while generating zero profit.

Sandwich attack awareness is the second MEV variant your scanner needs to account for, particularly for DEX-to-CEX arbitrage where the on-chain leg involves an AMM trade. In a sandwich attack, a searcher places a buy order before your transaction and a sell order after it in the same block, using your trade's price impact to profit from the spread they've created around you. The defense is a combination of tight slippage tolerance settings — limiting the acceptable price impact of your DEX leg to the minimum required for the opportunity to remain profitable — and using AMM aggregators that split large orders across multiple pools to minimize the price impact concentration that makes sandwich attacks economically worthwhile for the attacker.

Most arbitrage scanners operate entirely on confirmed blockchain state — they see prices and liquidity as they exist in finalized blocks. The builders who consistently find the highest-value opportunities have upgraded to reading the mempool: the queue of pending, unconfirmed transactions waiting to be included in the next block. Because large trades that haven't been confirmed yet will change the price and liquidity state of a DEX pool the moment they are included, reading them before confirmation gives you a meaningful information advantage over scanners that only see confirmed state.

The practical implementation requires running your own node with mempool access, or using a specialized mempool data provider, and building a listener that filters pending transactions for those interacting with the specific DEX pools your scanner monitors. When you detect a large pending swap in a pool you're tracking — one large enough to create or close a profitable spread — your scanner can calculate the expected post-trade price state and evaluate whether an arbitrage opportunity will exist in the block after that transaction confirms. If the opportunity passes your profitability threshold at the projected post-trade prices, you can submit your arbitrage transaction with a gas fee calibrated to land in the same block as the triggering transaction, capturing the spread the large trade creates the instant it is confirmed.

This is the same technique that sophisticated MEV searchers use to find sandwich opportunities, run in reverse to find legitimate arbitrage created by large user trades rather than to exploit those users. The key distinction in your implementation is that you are responding to the market conditions that large trades create, not inserting yourself between a user's transaction and the outcome they expected. Building this mempool monitoring layer substantially increases the frequency of high-quality signals your scanner identifies, because it surfaces opportunities that will exist for a single block rather than only opportunities that persist long enough to appear in confirmed state.

Gas fees are the single most consistent source of margin erosion for DEX arbitrage scanners, and most builders manage them with a static maximum gas price setting that either misses opportunities during congestion or overpays substantially during low-fee periods. A dynamic gas strategy computes the gas fee your transaction needs to pay at the moment of submission to achieve the block inclusion timing required for the specific opportunity, rather than applying a fixed maximum that is either too low to compete in fast markets or unnecessarily expensive in slow ones.

The core of a dynamic gas strategy is a real-time gas price oracle that tracks the current base fee, the distribution of priority fees in recent blocks, and any mempool congestion signals that predict near-term fee movements. For each arbitrage signal your scanner generates, you compute the maximum gas fee you can pay while keeping the trade profitable — the breakeven gas price for that specific opportunity — and compare it against the current gas price required for inclusion in the next one, two, or three blocks. If the required gas price is below your breakeven, you submit with a fee optimized for the target inclusion block. If the required gas price exceeds your breakeven, the opportunity does not meet minimum profitability after execution costs and should be skipped rather than forced through at a loss.

EIP-1559 fee structure optimization on Ethereum requires your dynamic gas strategy to separately manage the base fee and the priority fee components of the total gas cost. The base fee is burned by the protocol and is the same for all transactions in a block, determined algorithmically by recent block utilization. The priority fee is a tip to the block producer and is what actually determines your transaction's priority relative to other pending transactions paying the same base fee. For time-sensitive arbitrage transactions, setting the priority fee at the minimum required to place your transaction ahead of competing arbitrage bots in the same opportunity window — rather than at an arbitrary multiple of the current average — minimizes unnecessary fee expenditure while maintaining the competitive position needed to capture the opportunity.

Getting a single arbitrage strategy working profitably is a significant achievement. Turning that into a scalable, durable system that generates consistent returns across changing market conditions requires a second phase of development that most scanner builders never reach: expanding coverage systematically, diversifying across strategy types to reduce dependence on any single opportunity source, and building the performance monitoring infrastructure that tells you in real time whether each component of your system is working as designed. Scaling an arbitrage scanner is not simply running the same logic across more exchanges — it requires architectural decisions about how to manage the increased data volume, execution complexity, and capital allocation that come with a larger operational footprint.

The temptation when scaling is to add every exchange available and treat coverage breadth as a direct proxy for opportunity frequency. The reality is that adding low-quality exchanges to your scanner increases data pipeline complexity and maintenance burden without proportionally increasing profitable signal frequency, because many smaller exchanges have wide spreads that appear as arbitrage opportunities in raw price comparisons but are not executable at the quoted prices due to thin liquidity and high withdrawal fees. A disciplined exchange coverage expansion process prioritizes exchanges based on three criteria evaluated in combination: their liquidity depth in your target trading pairs, their API reliability as measured by uptime and rate limit generosity, and the profitability frequency of historical signals against them relative to the data pipeline complexity they add.

Building a standardized exchange integration template dramatically reduces the per-exchange development cost as you scale, because each new exchange connector only needs to implement the specific methods your template defines — price feed subscription, order book polling, order submission, and fee schedule retrieval — rather than requiring custom integration logic built from scratch for every exchange's unique API idiosyncrasies. Exchanges that support the CCXT library provide the fastest integration path because CCXT has already abstracted the API differences across hundreds of exchanges into a uniform interface, though at the cost of some latency compared to a direct, exchange-specific implementation optimized for speed.

Maintaining a tiered exchange roster separates your exchanges into categories based on their role in your scanner's operation: Tier 1 exchanges receive the lowest-latency direct WebSocket connections and are included in all real-time signal detection logic; Tier 2 exchanges are polled on slightly longer intervals and included in signal detection for opportunities where their specific liquidity or fee structure creates a unique advantage over Tier 1 alternatives; Tier 3 exchanges are monitored for market intelligence rather than active execution, providing broader price visibility without the full integration cost of Tier 1 connections. Reviewing and adjusting tier assignments on a monthly basis based on each exchange's recent signal quality and API reliability ensures your highest-resource connections remain allocated to the exchanges generating the most profitable opportunities rather than reflecting historical decisions that may no longer be optimal.

A scanner that relies entirely on a single arbitrage strategy type — say, simple cross-exchange arbitrage between the same two exchange pairs — has a profitability profile that is vulnerable to a single competitor or market change eliminating that specific opportunity source. Strategy diversification builds resilience by running multiple independently viable arbitrage strategy types simultaneously, with capital allocated across strategies based on their recent performance metrics rather than static weights set at deployment.

The most natural diversification path for a scanner that starts with cross-exchange arbitrage is adding triangular arbitrage detection on the same exchanges already integrated for price feeds, because the data infrastructure needed for triangular detection is largely identical to what cross-exchange detection already requires — the additional computational cost is the graph traversal algorithm for finding circular paths, not new data connections. Once triangular arbitrage is running on centralized exchange data, extending to DEX-to-CEX arbitrage requires adding on-chain data feeds for the specific DEX pools relevant to your target pairs, which is the most technically demanding integration step but also the one that opens the highest-value and least-competed opportunity categories.

Regime-conditional strategy weighting adjusts how much capital each strategy type is allocated based on current market conditions, because different arbitrage strategies are more or less productive depending on whether the market is trending strongly, consolidating, or experiencing high volatility. Cross-exchange price gaps tend to be widest and most frequent during high-volatility events when fast-moving markets leave different exchanges with stale prices for longer before arbitrageurs close the gap. Triangular arbitrage on a single exchange tends to be most productive during normal market hours when market makers are actively updating three related pairs but occasional imbalances briefly open profitable loops. Building simple market regime detection — using metrics like rolling 1-hour volatility and cross-exchange price correlation — into your capital allocation logic allows the scanner to automatically weight toward the strategy type that historically performs best in current conditions.

A production arbitrage scanner generates a continuous stream of operational metrics — signal frequency, execution latency, win rate per strategy, realized PnL per exchange, API error rates, gas cost as a percentage of gross profit — that collectively tell you whether your system is performing as designed or has developed a problem that is quietly eroding profitability. Without a structured performance monitoring system, these metrics exist only as logs that require manual analysis to interpret, which means problems can persist for hours or days before they are noticed and diagnosed.

Building a real-time strategy health dashboard consolidates the metrics that matter most into a view you can check at a glance, with automated alerts triggered when any metric deviates from its expected range. The most critical metrics to monitor continuously are the realized PnL per hour for each active strategy (a drop below the trailing 7-day average by more than one standard deviation warrants investigation), the ratio of gas cost to gross profit for DEX strategies (a sustained increase indicates gas optimization is needed or market conditions have changed), and the API error rate per exchange connection (elevated error rates predict imminent connection failures that will cause missed signals). Treating these as live operational metrics with alerting thresholds rather than historical data for periodic review transforms your performance monitoring from a diagnostic tool into a real-time early warning system.

A/B testing for scanner optimization applies the same framework to evaluating parameter changes — new signal filtering thresholds, updated fee calculations, modified slippage estimates — by running the proposed change on a portion of your capital allocation alongside the current production parameters and comparing outcomes over a sufficient sample of trades to determine whether the change produces statistically meaningful improvement. Making parameter changes without this testing framework risks deploying modifications that appear theoretically superior but perform worse in live market conditions due to factors the theoretical analysis did not capture, and the A/B structure ensures that even if the tested change underperforms, only the allocated test fraction of capital is affected while the production parameters continue operating normally.

Even with a solid plan, a few tough, practical questions always pop up when you move from theory to a live, operational system. These are the real-world challenges that can make or break your project. Let's tackle the most common ones head-on.

Yes, but the game has completely changed. The days of finding massive, obvious price spreads are long gone—market efficiency killed those opportunities.

Today, profitability comes from a combination of speed, low fees, and smart niche selection.

A custom-built scanner gives you an edge by letting you target opportunities that larger firms might ignore. Think about newly listed token pairs on DEXs or less liquid markets where automated systems can still find an advantage. The goal isn't a single massive payday anymore; it's about racking up a high volume of small, consistent wins. This demands constant optimization of your code, a relentless focus on minimizing latency, and ruthless management of every single transaction cost.

The top three project-killers you'll face are latency, API instability, and profit calculation errors. Get any of them wrong, and you're done.

First, latency is a constant battle where milliseconds matter. You need the fastest WebSocket connections and highly optimized code just to have a chance. A few milliseconds of delay is the difference between capturing a profit and missing out entirely.

Second, exchange APIs are notoriously unreliable. They have rate limits, become unstable, or fail completely during high market volatility. Your scanner absolutely must have rock-solid error handling and reconnection logic built-in to survive these outages without crashing or, worse, losing money.

Finally, calculating your true profit is much harder than it looks. You have to accurately factor in a complex web of costs:

A single miscalculation here can instantly flip a "winning" trade into a guaranteed loss.

You can technically start small, but it's important to be realistic. Your profit potential is directly tied to your available capital. While you could test a scanner with just a few hundred dollars, the numbers often don't make sense at that scale.

A 0.5% profit on a $100 trade is only 50 cents, which might not even cover your fees. To see returns that are actually meaningful, you should be looking at a starting point somewhere in the $2,000 to $10,000 range.

This level of capital allows for position sizes that can absorb fixed costs like withdrawal fees and still generate a worthwhile profit on small percentage gains. For any cross-exchange arbitrage strategy, remember you'll need to split this capital across multiple exchanges to be ready to trade the moment an opportunity appears.

MEV, or Miner Extractable Value, is the profit that block producers can extract by reordering or inserting transactions within blocks they are assembling. For arbitrage scanners specifically, the most damaging MEV pattern is frontrunning: a searcher bot monitors the public mempool, detects your pending arbitrage transaction, and submits an identical trade with a higher gas fee to execute before yours in the same block. The searcher captures the profit your scanner identified while your transaction either executes at a worse price — after the spread has already been closed — or fails entirely. Either way, you still pay the gas fee.

The most accessible protection for independent builders is routing transactions through a private relay like Flashbots Protect on Ethereum, which submits your trades directly to block builders without broadcasting them to the public mempool. Your transaction is invisible to frontrunning bots until it is already included in a block. Sandwich attacks are a related threat specific to AMM-based DEX trades, where a searcher places a buy before your transaction and a sell after it in the same block, profiting from the price impact your trade creates. The defense is setting tight slippage tolerances on your DEX legs — allowing only the minimum price impact required for the opportunity to remain profitable — and using AMM aggregators that distribute order flow across multiple pools to reduce the concentrated price impact that makes sandwich attacks worthwhile for the attacker.

The key to scaling without losing control is building with standardization and separation of concerns from the start. Each strategy type — cross-exchange, triangular, DEX-to-CEX — should run as an independent module that consumes data from a shared normalized data pipeline rather than maintaining its own exchange connections. This architecture means adding a new strategy only requires writing the detection logic and capital allocation rules for that strategy type, not rebuilding the data infrastructure it runs on. Similarly, building a standardized exchange integration template reduces the per-exchange development cost for coverage expansion, because each new connector only needs to implement the standard interface methods your pipeline defines rather than requiring fully custom integration code.

Tiered exchange roster management keeps operational complexity proportional to the value each exchange contributes: Tier 1 exchanges get low-latency direct WebSocket connections and are included in all real-time detection; Tier 2 exchanges are polled on slightly longer intervals for strategies where their specific liquidity creates unique advantages; Tier 3 exchanges are monitored for market intelligence without active execution integration. Reviewing tier assignments monthly based on recent signal quality and API reliability ensures your highest-resource connections remain on the exchanges generating the most profitable opportunities. Regime-conditional strategy weighting then automatically adjusts capital allocation across strategy types based on which performs best in current market conditions — weighting toward cross-exchange arbitrage during high-volatility periods when price gaps between exchanges widen, and toward triangular arbitrage during normal market hours when single-exchange imbalances are the more frequent opportunity source.

Ready to elevate your trading signals? Don't just find arbitrage opportunities—validate them with on-chain intelligence. Wallet Finder.ai helps you track smart money movements, see what profitable traders are buying, and get real-time alerts. Start your 7-day trial and turn market noise into actionable signals.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.