Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

June 18, 2026

A familiar trade setup keeps repeating. A token rips on one chain, your feed fills with screenshots, and by the time you've mapped the wallets behind the move, capital has already rotated into the next expression of the same theme on another chain.

That second move is where a lot of traders get paid. It's also where a lot of traders stay late.

Most traders still treat Ethereum, Solana, Base, and other ecosystems as separate hunting grounds. That's too slow. In practice, DeFi behaves like a chain of markets: wallets, bridges, venues, and narratives connect assets that look unrelated if you only watch one execution venue at a time. When one link tightens, liquidity and attention spill into the next.

You've seen the pattern. A smart wallet accumulates a token on one chain before the broader market notices. Minutes or hours later, wallets with similar behavior begin bridging, rotating stablecoins, or buying adjacent assets somewhere else. The first chart gets the attention. The second chart often gets the cleaner entry.

The frustration isn't that the market is random. It's that the signal is distributed. Price moves on one chain. Wallet activity shows up on another. The narrative catches up on social channels later. If you only watch candles, you react after the repricing is already underway.

That's the cross-chain domino effect. One event starts the sequence, but the profitable part often sits one or two hops away from the original trigger.

Most traders don't miss because they lack conviction. They miss because they're reading isolated markets instead of linked ones.

In DeFi, these links are practical. Capital moves through bridges. Traders reuse collateral. Liquidity providers rebalance exposure. Market makers hedge where inventory is cheapest to move. A narrative that starts as a token-specific move can become a chain-wide repricing of related assets, wrappers, or infrastructure plays.

The useful question isn't “What's pumping?” It's “Which connected market hasn't repriced yet?”

That shift matters for copy traders, discretionary traders, and quant desks. Once you stop treating cross-chain activity as noise, you can start building a repeatable workflow around source wallets, transfer paths, liquidity migration, and destination trades.

A trader sees ETH ecosystem tokens bid on Arbitrum, then stablecoins leave the same wallets through a bridge, and the next buys show up in a liquid Solana meme or infra name. Those are not separate trades. They are one trade expressed across multiple venues.

That is the chain of markets in DeFi. It is a linked sequence of markets connected by participant overlap, capital transfer routes, and repeatable thesis propagation.

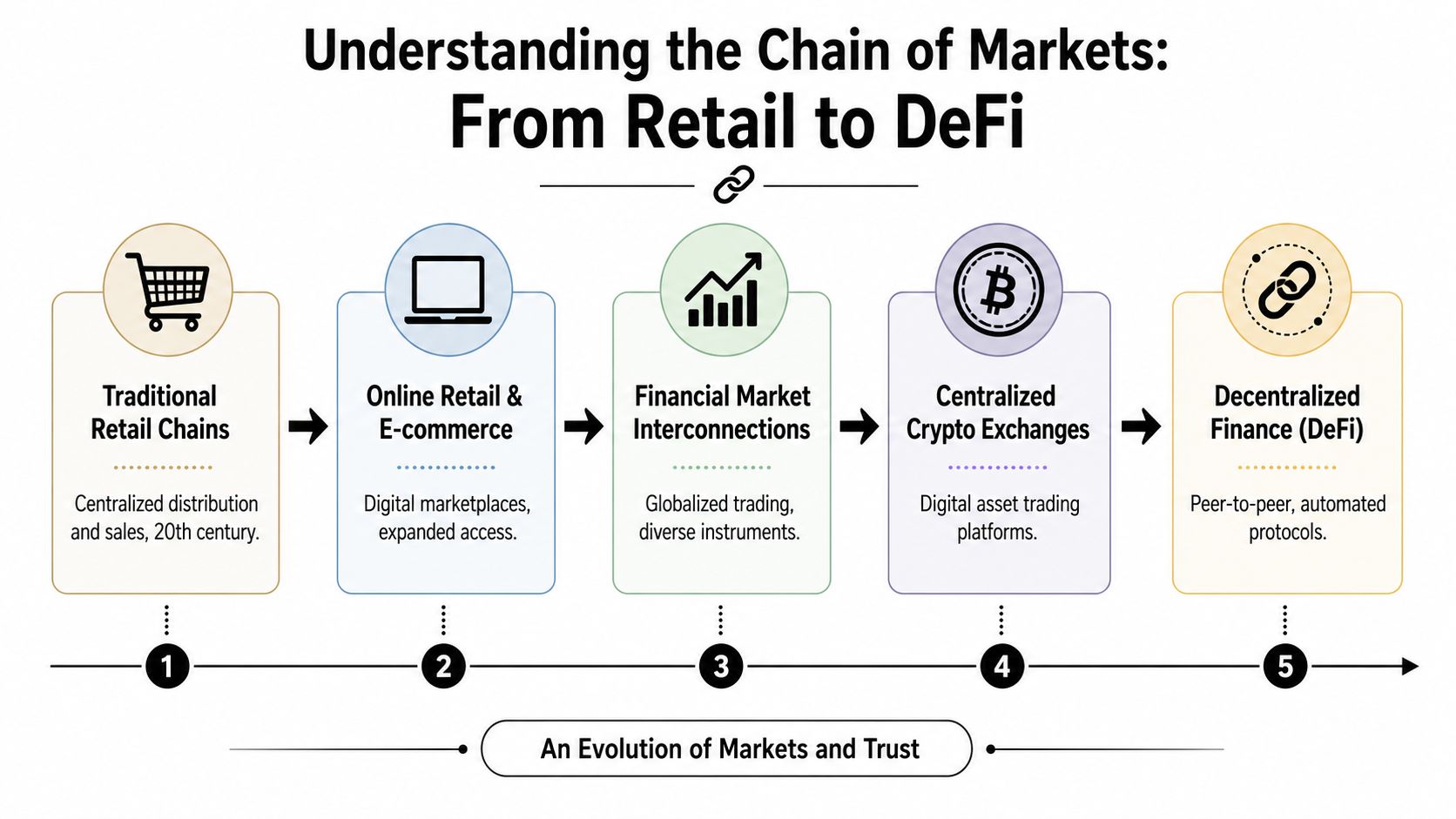

By 1930, chain grocery stores in the U.S. operated over 65,000 outlets and accounted for nearly 50% of all consumer grocery sales, showing how interconnected systems can dominate fragmented markets through scale and standardization, according to EBSCO's history of chain stores.

Retail chains coordinated pricing, inventory, and distribution across many local endpoints. A shopper interacted with one store, but the economics were shaped by a wider system.

DeFi has the same coordination problem with different rails. Chains have different fee structures, user mixes, and liquidity depth. Protocols specialize in spot trading, perps, lending, or staking. Bridges move inventory. Wallet clusters express the thesis before the ticker-level crowd sees it.

That framing matters because cross-chain trading is rarely isolated. A token on Ethereum and a related token on Solana can trade as part of the same market chain even if they share no governance or treasury connection. What links them is behavior. The same wallets rotate capital, use similar timing, and respond to the same catalyst.

Three conditions make the chain real enough to trade.

If one of those conditions is missing, the connection is weaker. If all three show up repeatedly, treat the markets as linked.

Discretionary traders often lose precision. They define the market by chart or ticker. For execution, the better unit is the wallet path. Markets belong to the same chain when the same capital repeatedly moves between them under the same setup.

Practical rule: Define the market boundary by repeated wallet behavior and transfer routes, not by chain labels.

For retail traders, a market chain was a corporate system. For DeFi traders, it is an observable flow map.

The operational question is simple. Where did the trade start, how did capital travel, and which destination market still has room to reprice? That is the shift from describing cross-chain activity to trading it.

A basic watchlist will not answer that. You need wallet-level attribution, bridge tracking, and destination-market confirmation. This guide on tracking smart money across blockchains shows the kind of monitoring stack that makes the framework usable in live conditions.

Most edge in DeFi comes from one of three places: better timing, better filtering, or better interpretation. The chain of markets matters because it improves all three.

If you can identify the source market, the transfer path, and the destination market, you don't need to chase the loudest chart. You can target the lagging expression of the same trade.

A weak market link often carries the best setup. In market-chain analysis, one important question is which segment has the weakest demand visibility or product availability. Applied to trading, that means the constrained link in a cross-chain event is often where the sharpest repricing happens once the bottleneck clears, as noted in Luth Research's discussion of underserved market segments.

In practice, that constrained link might be:

| Constraint | What it looks like in DeFi | Why traders care |

|---|---|---|

| Visibility gap | Early buying is obvious on one chain but ignored on another | The destination trade hasn't been crowded yet |

| Liquidity mismatch | Capital arrives faster than local liquidity can absorb | Price can move abruptly once inventory gets thin |

| Narrative lag | Social attention still points at the first token | Related assets can stay mispriced briefly |

| Routing friction | Bridging or wallet setup slows participants | Early movers get cleaner entries |

A copy trader uses this framework to answer a direct question: which wallet started the sequence, and where is that wallet likely to go next? The edge isn't blind imitation. It's selective anticipation. You don't just mirror the first fill. You watch whether the trader is reloading, rotating, or exporting the thesis to another chain.

A quant researcher uses the same framework differently. Instead of searching for one wallet, they model linked behavior across cohorts. They care about recurring bridge routes, wallet clusters with shared timing, and delayed correlation between source and destination assets.

That difference in style doesn't change the core idea. Both are exploiting market inefficiency created by fragmented observation.

What works:

What usually fails:

If you can't identify who moved, where they moved, and what they bought after moving, you don't have a chain thesis yet. You have a story.

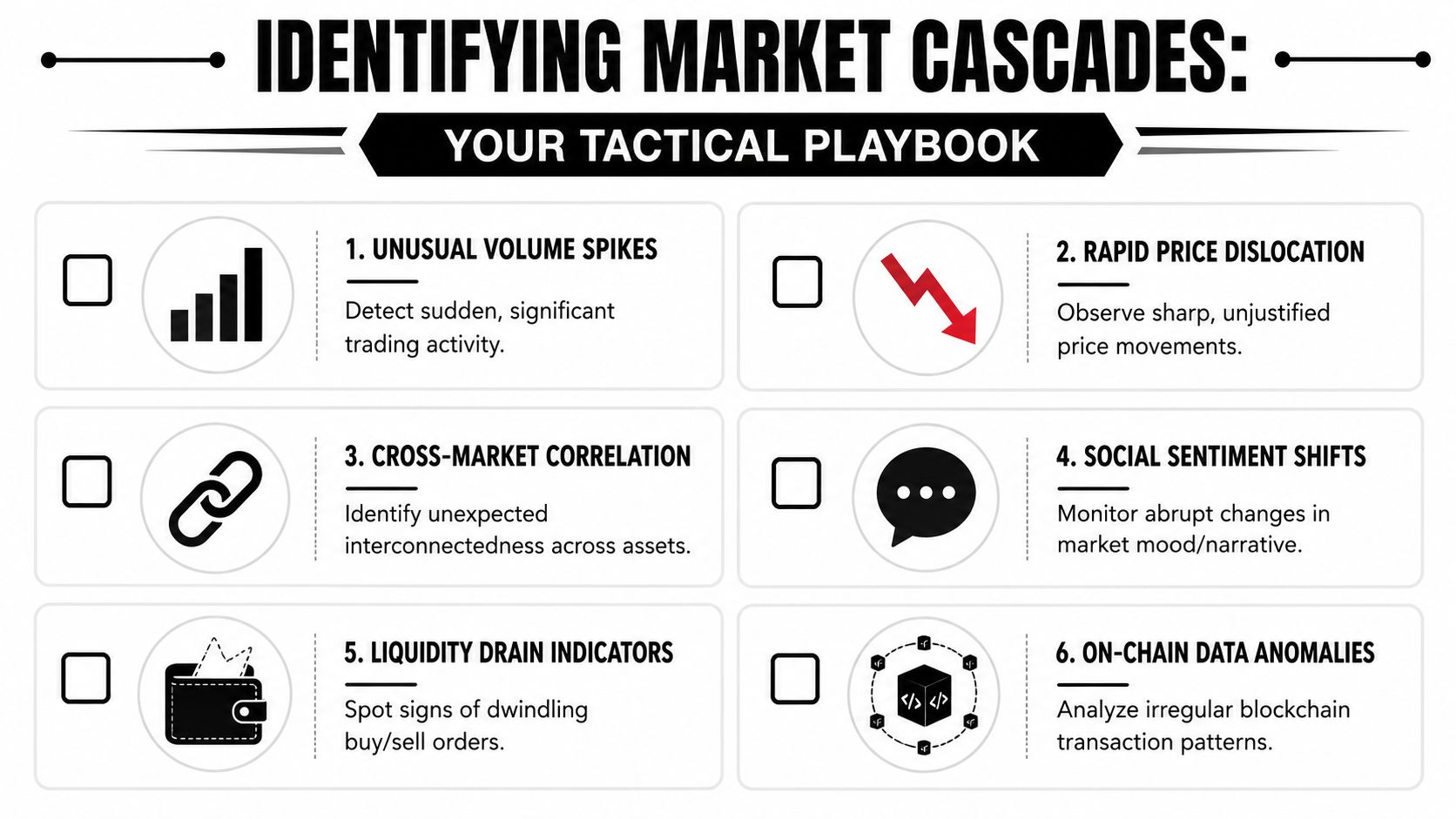

A profitable cascade usually starts before the chart looks obvious.

The pattern is familiar. A small group of skilled wallets accumulates on one chain. Capital leaves through a bridge route that those wallets have used before. Minutes or hours later, a thinner market on another chain starts to react. By the time social accounts explain the move, the easy entry is often gone. The job here is to catch the sequence early enough to act, and to separate real capital rotation from random cross-chain noise.

Start with the source chain. The first usable signal is not price alone. It is coordinated positioning that looks deliberate.

Useful signs include:

One large swap proves very little. A cohort of credible wallets building exposure inside a tight window is more interesting because it suggests shared conviction or shared information.

Size matters, but behavior matters more. I would rather track five wallets that consistently rotate capital well than fifty wallets reacting late to a breakout candle.

A cascade becomes tradable once capital moves. Source-chain strength without follow-through often produces false positives.

Focus on three questions:

Which asset moved

Stablecoins, native gas assets, wrapped majors, and governance tokens signal different intentions. Stablecoin movement usually points to fresh deployment. A governance token transfer may just be treasury management or internal routing.

Which wallets moved it

Bridge volume by itself is weak evidence. Known profitable wallets, or a repeat cohort that has traded the same route before, carry more weight.

What happened after arrival

Arrival alone is not enough. The useful pattern is bridge, short delay, then swaps into a specific destination asset or LP.

Execution improves when the route is familiar. If a wallet repeatedly buys on Solana, bridges to Base, and then concentrates into one sector, that path deserves a higher prior than a one-off transfer. Traders building route-based monitors should pair wallet tracking with liquidity-flow analysis for cross-chain arbitrage, because route efficiency and post-bridge deployment timing often determine whether the setup is still tradable.

The best destination setups usually look incomplete, not crowded.

What matters is the mismatch between incoming capital and local market depth. A destination token with thin liquidity, limited attention, and a clear recipient wallet cluster can move hard even before broader participation shows up.

| Signal | What it indicates | Possible action |

|---|---|---|

| New capital lands before social chatter follows | Information is still unevenly distributed | Build a starter position and wait for confirmation |

| Related tokens on the destination chain diverge | Informed flow is targeting one asset, not the whole basket | Focus on the direct recipient rather than broad sector exposure |

| Local liquidity is thinner than the source chain | Marginal demand can move price faster | Scale carefully and avoid forcing size |

| Known wallets add in tranches | They are still managing entry and still see upside | Watch for second-wave confirmation from similar wallets |

Many traders get sloppy; they buy every adjacent ticker and call it thesis expression. In practice, the cleaner trade is often the exact destination asset that received the first serious deployment.

Off-chain narrative still matters. It just works better as confirmation than as the trigger.

The signal to watch is timing. If wallets commit first, then the language on X, Telegram, or Discord shifts from silence to explanation, the cascade is advancing. That shift often marks the handoff from informed capital to reactive capital.

Useful forms of narrative acceleration include:

Ticker confusion is one of the better late-stage tells. Once traders start reaching for substitutes, the original move is no longer isolated. The cascade is broadening, and risk management matters more than aggressive chasing.

A workable process needs to do three things well: detect source wallets early, confirm whether capital crossed chains, and verify that the destination trade fits the same thesis rather than random wallet activity.

The most useful tools for this job combine wallet discovery, trade history, token discovery, and alerts. Wallet Finder.ai is one example. It surfaces wallet activity across major ecosystems, shows historical trading behavior, and lets traders build watchlists and alerts around wallets, tokens, and trades.

Start with the source chain, not the destination rumor. If a token starts attracting credible wallets, use a discovery view to identify which addresses entered first and which ones added rather than aped the first spike. Early adds matter more than late momentum fills.

Then tighten the list. You don't need every active wallet. You need a small cohort with repeatable behavior:

That filtered watchlist becomes the backbone of the strategy.

The second step is route confirmation. If a watched wallet exits or trims on Chain A, that alone isn't actionable. You want to know whether the wallet moved capital into Chain B and deployed it into a related setup.

A good review process looks like this:

Check the outbound transaction type

Was it a simple transfer, a bridge interaction, or internal wallet reshuffling?

Check the asset moved

Stablecoins often imply dry powder. Native gas assets can imply flexibility and fast redeployment.

Check the first destination action

The first post-bridge swap is frequently the highest-signal trade in the sequence.

For traders who want to get more precise about this stage, this guide on analyzing cross-chain bridge transactions helps separate operational transfers from thesis-driven rotation.

Most copy trading mistakes arise from this. A wallet can look smart in one move and still be uncopyable. You need context.

Check for:

| Validation point | Why it matters |

|---|---|

| Historical consistency | One lucky trade doesn't create a reliable signal source |

| Entry timing | Some wallets are good at discovery, others only chase strength |

| Position sizing behavior | Oversized bets can distort your own risk if mirrored blindly |

| Exit style | Some traders scale out methodically, others disappear into illiquidity |

The broader reason this workflow works is that trading infrastructure has become more data-driven. In the same way global supply chains evolved into network-driven systems supported by AI and machine learning, traders now use AI-powered tools and predictive analytics to interpret on-chain activity and extract value from those network effects, as discussed in Blume Global's history of supply-chain evolution.

Here's a short visual walkthrough of that workflow in action:

Once the setup is confirmed, execution should stay mechanical.

Enter on confirmation, not on hope

Wait for destination deployment, not just the bridge event.

Size for liquidity, not conviction

Secondary markets can move hard in both directions when books are thin.

Track the same wallets after entry

If the initiating cohort starts distributing into strength, your thesis may already be mature.

The chain thesis ends when the same wallets that created the dislocation begin unwinding it.

DeFi traders who still think chain by chain are usually late to the meaningful move. The visible pump is often just the first expression of a broader repricing event. The cleaner trade often appears where capital, liquidity, and attention are still converging.

That's the practical value of the chain of markets framework. It gives you a way to classify source markets, identify transfer paths, and find destination markets before the crowd fully maps the connection. The work is less about prediction in the abstract and more about reading linked behavior precisely.

Emerging opportunities often appear when rerouting in sourcing or distribution creates underserved markets. In DeFi, the equivalent is capital rerouting through bridges, which creates knowledge gaps and fresh demand on receiving chains, changing where traders should look for information and opportunity, as described in Circana's discussion of underserved markets and structural shifts.

The main shift is mental. Stop asking which token is hot. Ask which connected market hasn't repriced yet, which wallets are carrying the thesis across chains, and whether the destination asset still offers asymmetry.

Traders who do that consistently stop chasing confirmation and start trading transmission.

If you want to operationalize this cross-chain workflow, try Wallet Finder.ai to track profitable wallets, monitor token and trade discovery across ecosystems, and set alerts that help you catch the second move instead of reacting to it.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.