Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

April 19, 2026

You open a concentrated liquidity position, the pair looks healthy, volume is active, and the APR on the front end seems good enough to justify the click. A few days later, price drifts, your range goes stale, fee generation slows, and your PnL starts reflecting a problem you didn’t sign up for. Not because the pool is broken. Because passive LPing in volatile markets usually is.

That’s the fundamental approach for dynamo pool management in DeFi. It isn’t about picking a pool and hoping the math carries you. It’s about treating liquidity like a trading operation. You define ranges with intent, monitor when those ranges stop working, and rebalance before a decent setup turns into dead capital.

Most LPs learn the same lesson the expensive way. The edge doesn’t come from the first deposit. It comes from what you do after entry.

A bad LP trade rarely blows up all at once. It leaks.

You deposit into a concentrated liquidity pool around the current price because you want stronger fee density. At first, it works. Swaps hit your range. Fees come in. Then price trends in one direction, your inventory shifts toward the weaker side of the pair, and the position stops earning the way the dashboard promised. You haven’t exited, but you’re no longer really participating either.

That’s why I use the phrase dynamo pool management as a mindset. The useful metaphor comes from a real company named Dynamo Pool Management, which operates as a for-profit subsidiary of a non-profit, with profits supporting the Dynamo Swim Club, as described on the Dynamo Pool Management about page. In DeFi terms, that’s the right mental model. Your liquidity positions should feed your broader portfolio. They shouldn’t become isolated bets that gradually drain it.

The common mistake is assuming fee income will compensate for poor positioning. Sometimes it does for a while. Over longer stretches, weak range placement and slow reaction times usually hand the advantage to more active participants.

A strong LP setup does three things:

Practical rule: If you can’t explain when you’ll adjust a range before you enter it, you don’t have a liquidity strategy. You have a deposit.

What works is narrow focus with active oversight. Pick pools you understand. Know why that pair trades. Know who uses it. Know what kind of movement invalidates your current range.

What doesn’t work is copying broad LP advice from social posts that treat all pools the same. A stablecoin pool, an ETH-stable pool, and a volatile alt pair each punish different mistakes. The traders who stay profitable don’t “set and forget.” They decide what the position is supposed to do, then they manage it like it matters.

Concentrated liquidity rewards precision and punishes laziness. That’s the appeal and the trap.

When you provide liquidity in a concentrated AMM, you choose a price range instead of supplying capital across the full curve. That gives you more fee efficiency inside the range, but once price leaves it, your capital stops working as intended. So the first job isn’t hunting for the highest displayed yield. The first job is understanding the setup you’re entering.

There’s a useful metaphor from the labor market. Some roles pay about 25% below the national average, and the point for LPs is obvious: uninformed participants often earn meaningfully below what a better setup could have produced, as framed in this salary comparison discussion. In DeFi, below-average execution usually comes from poor pool selection, bad range width, and mismatched fee tiers.

A narrow range increases fee concentration, but only while price stays inside it. That makes narrow bands better for pairs with cleaner structure and more predictable trade flow. Wider ranges reduce how often you need to intervene, but they dilute fee density.

Ask one question before setting width: Am I trying to maximize fee capture or maximize time in range?

If you can’t monitor actively, don’t pretend you’ll maintain a very tight range well.

Higher fee tiers can work when the pair is volatile and traders will tolerate more slippage. Lower fee tiers fit pairs where efficiency matters more than margin per swap. The wrong fee tier can make even a decent range underperform because your position isn’t aligned with the pair’s trading behavior.

The true impact of this is frequently underestimated. Some pairs move with each other. Others only look attractive because the fee number is large. Correlated assets usually create cleaner LP conditions. Uncorrelated assets can still work, but your range and rebalance plan have to be sharper.

Use this before every new deployment:

Check the pair’s behavior

Read the volume pattern

Match the pool to your time horizon

For a broader grounding in LP mechanics, this guide to crypto liquidity pools is worth reviewing before you size up a new position.

I don’t start by maximizing. I start by validating.

| Decision | Good starting bias | What to avoid |

|---|---|---|

| Pair choice | Assets with understandable trade flow | Tokens you can’t value outside the pool |

| Range width | Wide enough to survive normal movement | Hyper-tight bands without monitoring time |

| Position size | Small enough to observe behavior first | Full allocation on first entry |

| Rebalance trigger | Predefined before deposit | Making it up after price moves |

Start with a position size that lets you learn the pool’s rhythm without forcing emotional decisions.

That last point matters. A first deposit should tell you how the pair behaves in practice. If the pool trades the way you expected, then scale. If not, you’ve paid tuition cheaply instead of committing serious capital to a weak read.

Every concentrated liquidity position has an expiration point. Not on-chain. In practical usefulness.

The position becomes inefficient when price approaches the edge of your range, when inventory drifts too far toward one asset, or when the fee opportunity no longer compensates for the risk you’re carrying. That’s why active rebalancing sits at the center of good dynamo pool management. It’s the difference between managing a strategy and babysitting a stale position.

A passive LP setup usually breaks in one of two ways. Price leaves the active range, so fee generation dries up. Or price grinds toward one side long enough that your asset mix changes into something you no longer want to hold at that weight.

Neither problem fixes itself.

If a trader actively manages entries and exits on directional trades, but treats LP positions as passive, they’re managing only half the risk book.

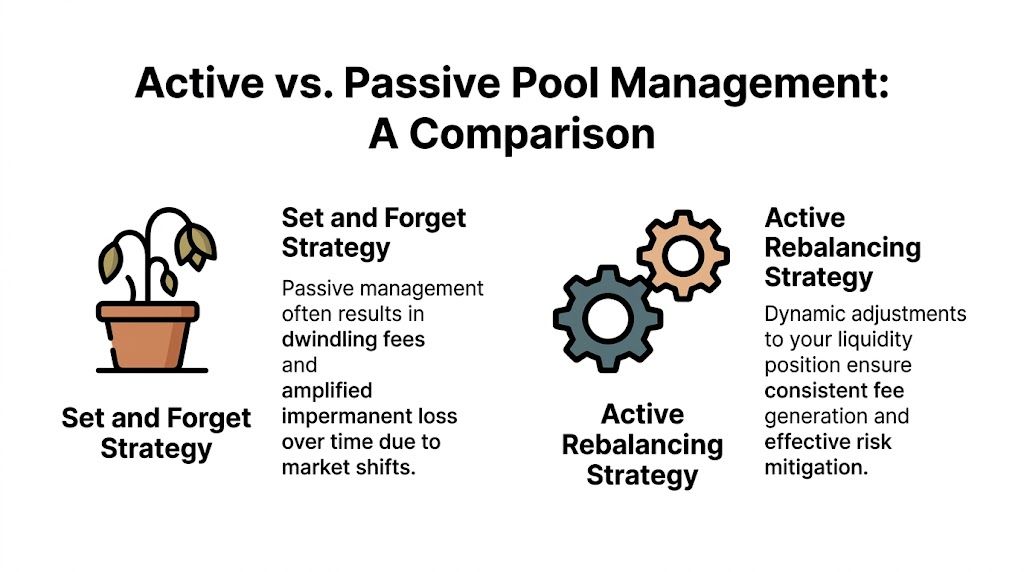

This is still the cleanest approach if you understand market structure and watch your positions. You move the range when price action invalidates the original placement, when volume migrates, or when the pair’s behavior changes.

What works here is flexibility. You can account for support and resistance, volatility compression, trend acceleration, and changes in sentiment. What doesn’t work is emotional intervention. If you rebalance only after frustration sets in, you’re late.

Manual rebalancing fits traders who already think in scenarios, not fixed rules.

Some LPs prefer a schedule. They review and adjust daily, every few days, or weekly depending on the pair. This is less precise, but it prevents total neglect.

The upside is discipline. The downside is obvious. The market doesn’t care about your calendar. A scheduled review may be too early and waste gas, or too late and leave you holding a dead range for longer than necessary.

Time-based methods work best when combined with basic price alerts.

Vault products such as Gamma and Arrakis reduce the operational burden by outsourcing part of the range management process. For many users, that’s a fair trade. You give up some direct control for simpler execution.

The issue is that automation follows a framework, not your full portfolio context. A vault might manage the position correctly on its own terms while still leaving you with exposures you wouldn’t have chosen manually.

| Strategy | Pros | Cons | Best For |

|---|---|---|---|

| Manual rebalancing | Highest flexibility, adapts to market context, supports custom risk views | Requires time, stronger judgment, and gas discipline | Active traders who already monitor charts and positions |

| Time-based rebalancing | Simple routine, easier to systematize, reduces neglect | Can miss fast moves, may trigger unnecessary adjustments | Part-time LPs who want structure without full automation |

| Automated vaults | Lower hands-on workload, convenient execution, easier for diversified users | Less control, strategy logic may not match your portfolio goals | Users who want exposure without frequent manual management |

I don’t use the same method across all pairs.

A lot of LP advice treats fees as a simple function of being closer to price. That’s incomplete.

Fee optimization comes from the interaction of four things:

That last point gets ignored. A brilliant rebalance plan can still underperform if you churn too much. Good LPs don’t just chase more fees. They ask whether the next adjustment has a positive expected impact after costs and inventory effects.

When I review a position, I’m usually deciding between three actions:

That third option matters. Not every pool deserves a rebalance. Some deserve capital withdrawal.

Most new LPs treat impermanent loss like a mysterious penalty that appears after the fact. In practice, it’s more manageable than that. IL is what happens when your inventory changes because price moves, and that new mix underperforms holding the assets outright.

The important part isn’t the textbook definition. The important part is recognizing when the fee opportunity is no longer compensating for the inventory shift.

A useful analogy comes from real pool operations. In the physical world, 40% of community pools faced regulatory fines for protocol failures, and the lesson for DeFi is straightforward: when operators ignore controls, preventable damage follows, as discussed in this non-profit pool management note. In LPing, failing to monitor IL, smart contract exposure, and asset-specific failure modes is the financial version of skipping safety protocols.

I don’t start with formulas. I start with scenarios.

If token A runs hard against token B, ask what you’ll own after the move. If the answer is “mostly the asset I least want after that move,” the setup needs more caution. Wider ranges can reduce maintenance pressure, but they don’t erase the core inventory problem.

Pair selection does a lot of hidden work. Correlated assets generally make IL easier to live with. Highly divergent assets can produce fee numbers that look tempting while building a much worse inventory outcome underneath.

Before entering a pool, check these in plain language:

For a deeper playbook on offsetting LP risk, this article on dynamic hedging for impermanent loss is a strong companion read.

Risk lens: A pool can be profitable on a dashboard and still be wrong for your book if the inventory you’re accumulating makes the rest of your portfolio worse.

Some methods are simple and effective:

IL also isn’t the only hidden risk. Oracle issues, governance changes, thin liquidity in stressed conditions, and token-specific mechanics can all turn a decent LP position into a bad one fast. Good dynamo pool management means acting like a risk manager first and a yield farmer second.

The jump from competent LP to consistently strong LP usually comes from one shift. Stop guessing what good positioning looks like. Start studying wallets that already do it well.

That sounds obvious, but most traders still operate from front-end metrics, social posts, and delayed narratives. None of those show you how skilled LPs size, rebalance, and rotate. On-chain behavior does.

There’s a useful analogy from service operations. Manual, inefficient processes can lead to 60% annual turnover, which is a reminder that systems break down when people try to manage too much by hand, as framed in this staffing operations discussion. LP research has the same problem. If you manually scan wallets, piece together swaps, and try to notice position changes after the fact, you’ll miss the moves that matter.

When you study strong liquidity providers on-chain, you’re not looking for a magic wallet. You’re looking for repeatable behaviors:

That last point is where amateurs usually lose the plot. Good LPs don’t just find decent pools. They know when a good pool stops being good.

A strong primer on this workflow is learning how to structure your own on-chain analysis process.

I like a four-step workflow because it keeps the process practical.

Don’t chase one-off outliers. You want wallets that show coherent decisions across time. If a wallet repeatedly interacts with concentrated liquidity pools, adjusts ranges rather than abandoning them blindly, and avoids chaotic spray-and-pray behavior, it’s worth a closer look.

Once a wallet is on your watchlist, inspect the sequence of actions. Did they enter after volatility compressed? Did they tighten ranges after trend stabilized? Did they pull liquidity before a sharp directional move?

This reveals the true value. You’re not just copying destinations. You’re inferring the rules.

Good wallet tracking doesn’t replace judgment. It lets you borrow tested judgment while you sharpen your own.

Some wallets are profitable because they have speed, relationships, or private flow you can’t replicate. Others are profitable because they manage positions well in public liquidity. Focus on the second group.

For LP copy-trading, I care more about interpretable behavior than brand-name addresses.

The key isn’t discovering a wallet once. The key is knowing when it acts again. Real-time notifications matter because concentrated liquidity positions age quickly. If you learn about a range adjustment too late, the best part of the move is gone.

Here’s a useful walkthrough before you set that up:

Once you rely on on-chain intelligence, your LP process improves in three ways.

| Advantage | What changes |

|---|---|

| Better entries | You stop choosing pools in isolation and start using observed behavior from proven operators |

| Faster adjustments | Alerts cut the lag between a market change and your response |

| Cleaner exits | You learn to recognize when skilled wallets stop defending a thesis |

This approach also changes your psychology. You spend less time searching for perfect public frameworks and more time reacting to evidence. That’s a better fit for DeFi because high-quality LP data is often fragmented, delayed, or hidden inside transaction history rather than neatly summarized on dashboards.

Profitable dynamo pool management comes down to a simple truth. Liquidity provision is not passive income in any serious sense. It’s active inventory management wrapped in an AMM interface.

The blueprint is straightforward if you keep it disciplined:

Researchers have noted that thorough technical benchmarks for new DeFi pool management strategies are often scarce, which makes the most reliable edge the observable behavior of wallets that already execute well, as reflected in this research integrity note on following available data. That’s the practical edge. Public theory is incomplete. On-chain behavior is specific.

If you want to manage liquidity like a professional, stop treating LP positions like parked capital. Treat them like live trades that need context, rules, and evidence. That shift alone changes everything.

If you want a faster way to find profitable wallets, study their LP behavior, and react when they move, Wallet Finder.ai gives you a practical edge. You can track smart money across major chains, build watchlists, review full wallet histories, and get alerts when the wallets you follow buy, sell, or rotate. For traders who want to turn on-chain footprints into an actionable pool management workflow, it’s a strong place to start.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.