Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

May 23, 2026

You open your wallet history to calculate gains and it looks manageable for about ten seconds. Then you remember the bridge, the LP deposit, the unstake, the airdrop claim, the token migration, the random memecoin swap on a sidechain, and the gas paid across all of it.

That's where most crypto tax guides stop being useful. They explain a clean buy-and-sell example, but active DeFi trading rarely looks clean. If you're copying wallets, farming yields, rotating between chains, and taking partial exits, learning how to calculate capital gains means building a process that survives messy on-chain activity.

The good news is that the core logic is still simple. The hard part is applying it consistently across fragmented wallet data. Once you know how basis, disposal events, and holding periods work, the rest becomes a recordkeeping and classification problem.

Most traders get tripped up because they mix up paper gains with taxable gains.

If your token doubled but you still hold it, that gain is unrealized. It may matter for your portfolio, but it usually isn't the event that creates capital gains tax. The tax event generally happens when you dispose of the asset. In crypto, that usually means selling for fiat, swapping into another token, or spending the asset.

The IRS framework is straightforward. You calculate gain or loss by subtracting your adjusted basis from the amount realized on sale, then classify the result based on holding period. Assets held for more than one year are long-term, and assets held for one year or less are short-term. Most capital asset sales are reported on Form 8949 and summarized on Schedule D under IRS Topic No. 409.

That means a swap from ETH into a newer token isn't just a portfolio move. For tax purposes, it often creates two things at once:

A lot of DeFi traders miss that second point. They track exits emotionally, not tax-lot by tax-lot.

Practical rule: If the transaction changed what asset you own, assume you need to test whether a taxable disposal happened.

In practice, the formula looks like this:

| Step | What you identify | Why it matters |

|---|---|---|

| Basis | What you paid for the crypto, adjusted as needed | This is your tax starting point |

| Amount realized | What you received when you sold, swapped, or spent it | This sets the exit value |

| Gain or loss | Amount realized minus adjusted basis | This determines taxable result |

| Holding period | Time between acquisition and disposal | This affects short-term or long-term treatment |

For active traders, the biggest mistake isn't bad math. It's bad event classification. A transfer between your own wallets usually isn't the same as a sale. A swap usually is. A bridge may or may not be simple depending on how the protocol structures it and what token you receive.

Short-term versus long-term treatment isn't a small detail. It changes how much of the gain may end up taxed at ordinary income rates versus preferential capital gains rates.

That's why timing matters. If you're near the one-year threshold on a large lot, selling too early can change the character of the gain even if the market price barely moved.

Count carefully. In the U.S., the holding period starts the day after acquisition and runs through the date of sale.

For DeFi traders, that becomes especially important when tokens move through wrapping, staking receipts, and LP positions. If your records don't clearly show when the original lot was acquired and what happened to it on-chain, you can't classify the final disposal correctly.

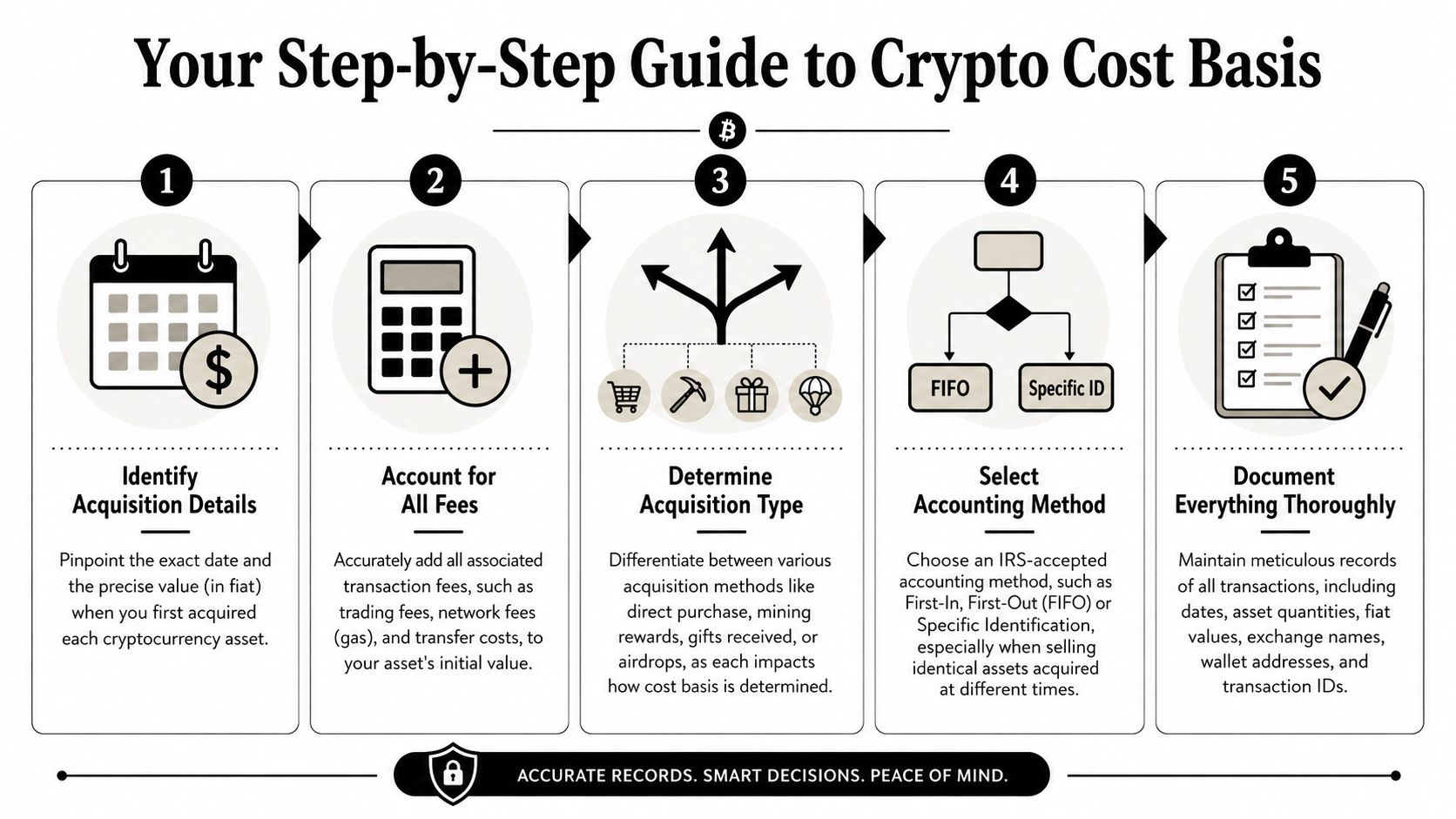

If you want accurate gains, start with accurate basis. Everything else sits on top of it.

Crypto traders often remember what they paid for the token and forget everything around it. Fees matter. Gas matters when it's part of acquisition cost. Lot-level detail matters. If your basis is wrong on entry, every later gain calculation is wrong too.

The IRS states that basis is generally what you paid for the asset, including commissions and certain acquisition costs, and that basis must be adjusted in some situations. For crypto, the practical takeaway is simple: using purchase price alone instead of adjusted basis can overstate gain and tax liability, as noted in IRS Topic No. 703 on basis of assets.

For a straightforward crypto purchase, basis usually includes:

When I review a trader's records, I usually want each acquisition lot to answer five questions cleanly:

If you can't answer those for every lot, you don't have a basis system. You have fragments.

Here's the operational version that works:

If you want a simpler way to reason through lot pricing assumptions before filing, this crypto average calculator guide is useful for organizing acquisition data, especially when your entries happened across multiple buys.

Basis gets messy fast when the acquisition wasn't a plain exchange buy.

A few examples:

| Acquisition type | What traders often do wrong | Better approach |

|---|---|---|

| DEX swap | Record only the token received | Also capture the disposed asset value and fees |

| Staking reward | Treat it like a purchased lot | Record the value when received, then track later disposal separately |

| Airdrop | Ignore the receipt until sale | Document the receipt event and later sale event distinctly |

| LP withdrawal | Treat all tokens received as fresh buys | Reconstruct what happened to the original deposited assets and any additional tokens received |

The common overpayment pattern is simple. A trader remembers purchase price, ignores fees, and reports too much gain.

For active on-chain traders, basis should live in a transaction ledger, not in your memory. The moment you rely on wallet recollection, you'll miss wrapped assets, wallet-to-wallet movements, and gas-adjusted entries.

Once your lots are recorded correctly, the next question is which lot you sold.

Accounting method starts driving real tax outcomes. If you bought the same token multiple times at different prices, your reported gain depends on which acquisition lot gets matched to the disposal. For an active trader, that choice can change not only the amount of gain but also whether more of it ends up short-term or long-term.

Suppose you accumulated the same token over time. Later, you sell or swap part of that position. You now have to determine which units left your inventory.

Three common approaches are:

The tax logic is simple. Older lots often have older holding periods and different basis. Newer lots often have a different basis and usually a shorter holding period. That creates a trade-off between current tax minimization and longer-term lot management.

| Method | How It Works | Best For | Example Tax Impact |

|---|---|---|---|

| FIFO | The earliest acquired lot is treated as sold first | Traders with simple records or long-held positions | Can pull in older lots with lower basis or long-term holding periods |

| LIFO | The most recently acquired lot is treated as sold first | Traders trying to match recent entries to exits | Can pull in newer basis and often keeps older lots untouched |

| Specific ID | You identify the exact lot sold | Traders with detailed wallet and lot records | Lets you choose lots strategically based on basis and holding period |

FIFO is usually the easiest to defend operationally because it's simple. If your records are incomplete, simplicity matters.

LIFO can be useful when recent entries have a higher basis and you want to reduce current gains. The problem is that if your bookkeeping is sloppy, lot matching gets harder to audit. With DeFi, that problem compounds because tokens move through wallets, bridges, LPs, and staking contracts.

Specific identification is the most flexible when you have the records to support it. For many active traders, it's the method that best reflects what they're trying to do economically. But it only works if you can clearly identify the lot, show when it was acquired, and tie that lot to the disposal.

Good tax strategy starts with good records. Without lot-level records, “strategy” turns into guesswork.

Holding-period classification is one of the highest-impact technical steps. Assets held one year or less are short-term, while assets held more than one year are long-term. A key practical point from Granite Harbor's capital gains guide is that losses should generally be allocated first against gains that are not eligible for preferential treatment, meaning short-term gains.

That matters because lot selection isn't just about this sale. It interacts with your whole year:

A clean process beats a clever one. The traders who stay compliant and still optimize their tax position are the ones who decide on a method early, apply it consistently, and maintain enough documentation to prove it.

Generic tax guides usually break down the moment DeFi enters the picture. Buying spot on an exchange is easy. The trouble starts when one wallet interacts with twenty protocols and every action looks half like a trade and half like infrastructure.

You swapped ETH for a small-cap token on a DEX. On-chain, it feels like one click. For tax purposes, it's usually a disposal of ETH and an acquisition of the token received.

That means you need to:

A lot of traders only track the new token because that's what they care about strategically. Tax reporting needs both sides.

You staked tokens and received periodic rewards. Then later you sold those reward tokens.

That usually creates two separate tracking jobs. First, the reward receipt may create income at the time received. Second, when you later sell or swap that reward token, you calculate capital gain or loss from the value assigned at receipt to the value at disposal.

The operational mistake is collapsing those into one event. Don't do that. A staking dashboard may present rewards as a running balance, but tax records need discrete receipt events where possible.

If you spend a lot of time in protocol reward systems, this overview of yield farming crypto mechanics is a good reminder of how many separate actions one farming strategy can create on-chain.

If a protocol paid you in a token and you later sold that token, you likely need one record for earning it and another for disposing of it.

You deposit two tokens into a liquidity pool. In exchange, you may receive an LP token or some other receipt representation. Later, you remove liquidity and get back a different mix of assets than what you put in.

In such scenarios, spreadsheet-only systems usually fail.

The practical issues are:

| DeFi event | What you need to identify | Why traders miss it |

|---|---|---|

| LP deposit | Whether the deposit is treated as a disposal of the tokens sent | The protocol UI feels like a transfer, not a trade |

| LP receipt token | Whether receipt token acquisition needs a separate basis record | It looks like an internal placeholder |

| Reward emissions | When reward tokens were received and their value at receipt | Rewards stream in over time |

| LP withdrawal | What assets came back, in what amounts, and with what resulting basis | Returned assets rarely mirror the deposit exactly |

Impermanent loss is the trading concept everyone knows. The tax challenge is reconstructing what happened to the original lots. If your software can't decode LP interactions, you'll end up manually classifying smart contract entries and exits from raw wallet history.

You claimed an airdrop after holding a governance token. Later you sold the airdropped token. Again, don't merge the events. Track the receipt, then track the disposal.

Hard forks and token migrations create the same practical need. You need a documented record of what asset left your wallet, what asset entered, and whether the event was economic or merely technical.

Buying an NFT with crypto is another common miss. You didn't just buy an NFT. You also disposed of the crypto used to buy it. If that crypto appreciated since acquisition, there may be a gain attached to the purchase itself.

The traders who get this right don't rely on wallet labels alone. They reconcile protocol activity to tax categories. That means reading contract interactions, not just token balances.

Manual crypto tax work breaks long before your trading strategy does.

After enough wallets, chains, and protocols, spreadsheets stop being a control system and start becoming a liability. You get duplicate transfers, missing cost basis, unlabeled contract interactions, and inconsistent timestamps between exchange exports and wallet activity.

Good on-chain tax tooling does four things well:

Active DeFi trading isn't merely high volume; it's structurally inconsistent. One protocol emits reward tokens. Another wraps positions. Another routes swaps through several contracts. Humans can review that. Humans shouldn't calculate all of it from scratch.

Automation helps, but blind trust is still a mistake.

Check these points before finalizing numbers:

A practical tool comparison can help if you're still sorting out your stack. This review of the best crypto calculator apps is a useful starting point for comparing what different platforms offer.

A short demo makes the workflow easier to visualize:

The true value of automation isn't speed alone. It's auditability. When a trader can trace a reported gain back to the wallet transaction, the lot used, and the classification logic applied, the numbers become defensible instead of approximate.

Most bad crypto tax outcomes come from a handful of repeat mistakes. Not exotic mistakes. Basic classification failures repeated across a lot of transactions.

Start here before you finalize anything:

Current U.S. long-term capital gains rates are 0%, 15%, and 20%, with a potential 3.8% net investment income tax for high earners. Public guidance also notes that for some filers, the 15% long-term bracket can apply from $48,350 up to $533,400, while short-term gains can be taxed at rates up to 37%. That's why holding period and total income level can materially change the tax result on the exact same gain, as outlined in Jackson Hewitt's explanation of capital gains rates.

That doesn't mean every trader should always hold longer. Markets don't wait for tax optimization. But it does mean you should know the tax cost of exiting early before you click sell.

Clean records give you options. Bad records force you into whatever answer you can still reconstruct in April.

If you remember one thing, remember this: calculating crypto capital gains isn't mainly a math problem. It's a transaction-mapping problem. Traders who classify events correctly, preserve lot records, and review automated outputs usually stay compliant without drowning in admin.

If your DeFi activity spans multiple wallets, chains, and copy-trading moves, Wallet Finder.ai can help you track on-chain behavior more cleanly and reduce the chaos that makes gain calculations harder than they need to be. It's especially useful when you want better visibility into wallet history, trade flows, and token activity before tax season turns that raw data into a reconciliation project.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.