Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

March 21, 2026

Here’s the deal: sharing your Zelle information is designed to be incredibly simple and secure. You only need to give someone the U.S. mobile number or email address you enrolled with. That's it. You should never, ever have to share your bank account number, login details, or password.

When someone wants to send you money through Zelle, the only piece of information they’ll ever need is your enrolled phone number or email. This is an intentional security feature built into the platform to protect your sensitive financial data while keeping payments fast.

Think of your Zelle contact info like a secure mailing address for your bank account. The money moves directly from their bank to yours in the background, but neither person ever sees the other's private banking details. It’s simple, direct, and private.

So, which one is better to share? Honestly, both are just as secure within the Zelle network. The choice really boils down to convenience and how well you know the person paying you.

This quick comparison can help you decide which is the right fit for your situation.

| Method | What to Share | Best For | Pro Tip |

|---|---|---|---|

| Phone Number | Your enrolled U.S. mobile number. | Quick payments with friends, family, or people you know and trust. | Ideal for splitting a dinner bill or paying back a friend who already has your number saved in their contacts. |

| Email Address | Your enrolled email address. | More formal or one-off transactions with people you don't know well. | Perfect for collecting rent, selling an item online, or receiving payment for freelance work. It keeps your personal phone number private. |

Ultimately, choosing between your phone number and email is a matter of personal preference. Both get the job done securely, so go with what feels most appropriate for the transaction.

The most important rule to remember is to only provide the information the sender actually needs. Zelle was built to work without you ever having to expose your banking password, debit card number, or any security codes.

The key is to use the platform as it was intended—for fast, simple payments between trusted individuals. For more tips on managing your digital wallet and personal finances, you can explore other guides on our blog.

It’s natural to be careful when your money is on the line. The great thing about Zelle is that it was designed from the ground up to keep your sensitive financial details private.

To get paid, all you ever need to share is the U.S. mobile number or email address you enrolled with. That's it.

Think about a friend paying you back for dinner. You just need to text them, "Hey, you can Zelle me at my number." They pop open their banking app, punch in your phone number, enter the amount, and hit send. Your bank account number and debit card info? They never even see it. This setup acts as a firewall, keeping your core financial data completely separate from the transaction itself.

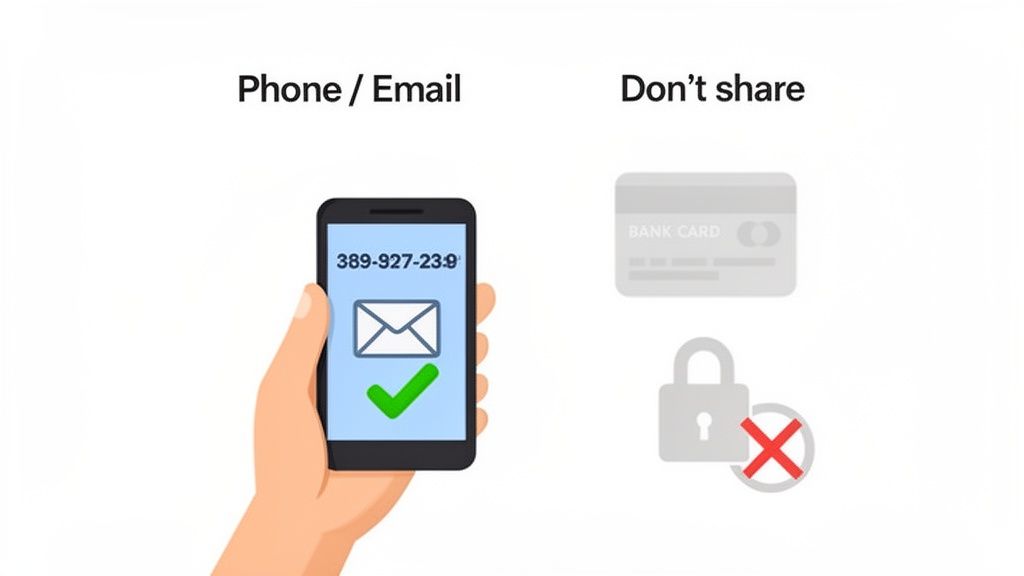

While your phone number or email is safe for receiving money, some information should always stay under lock and key. These are the details you guard no matter what.

Never, ever give out:

Protecting this information is non-negotiable. Zelle and your bank will never call or text you to ask for these sensitive details. Anyone who does is likely a scammer. To better understand how your data is managed, you can read more about our approach to user privacy.

The platform’s security is proven by its massive adoption and incredibly low fraud rates. To send or receive money, users just need an account with one of the over 2,200 participating banks.

With a projected 151 million enrolled users by the end of 2024, the platform's reliability is clear. In fact, over 99.98% of all transactions are sent without any report of fraud, a testament to its secure design. You can learn more about these Zelle statistics and how the platform maintains its safety record.

Sure, you can just rattle off your phone number or email address when someone needs to pay you with Zelle. But we’ve all been there—a single wrong digit or a simple typo, and your money could vanish into a stranger’s account.

Thankfully, there’s a much smarter way. Zelle has a couple of built-in features that are practically foolproof for preventing these kinds of mistakes: payment requests and QR codes.

Using the ‘Request’ function inside your banking app is easily one of the safest ways to get paid. Instead of giving your details to the sender and hoping they get it right, you kick off the process yourself. This sends them a notification with all your payment info pre-filled, which almost completely eliminates the risk of typos.

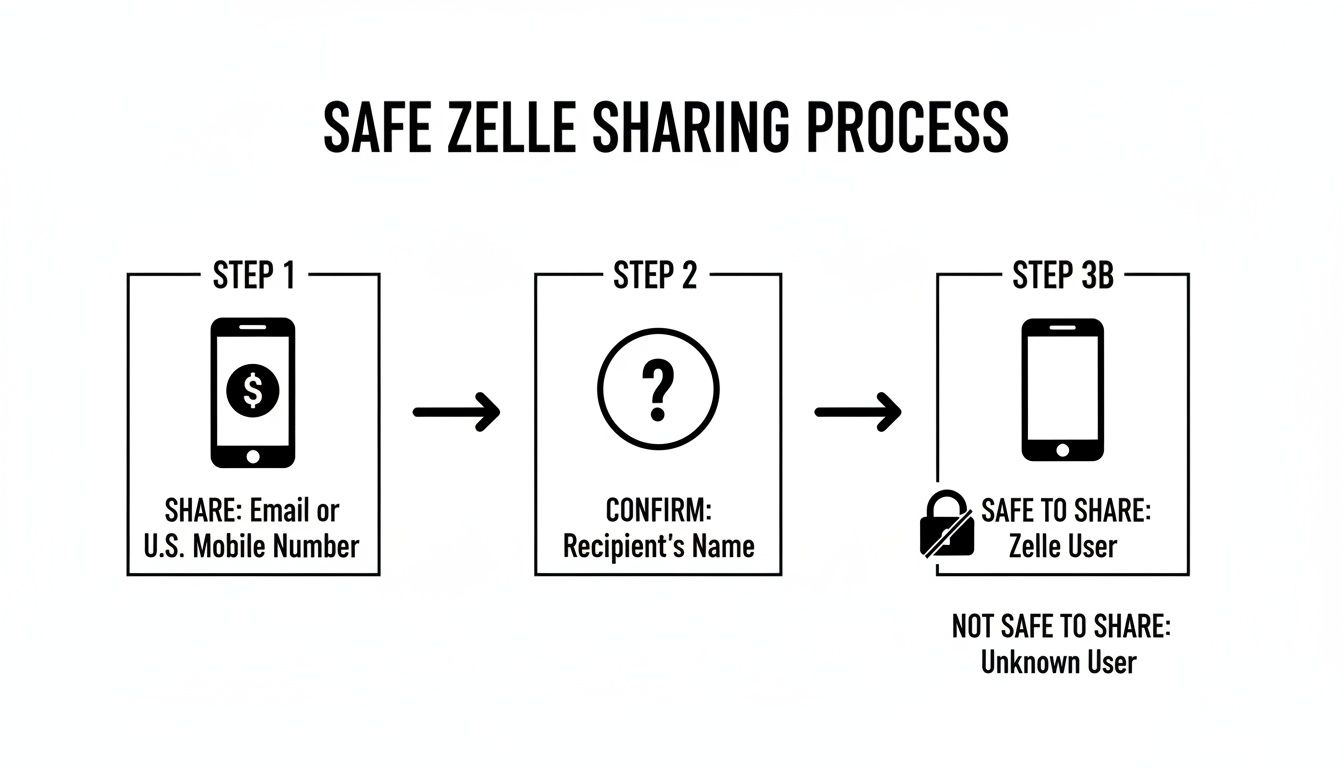

This simple diagram shows exactly what’s safe to share and what you need to keep private.

The main idea is to only share your enrolled contact information. Your sensitive financial data should never be part of the conversation.

Another fantastic, error-proof method is sharing your personal Zelle QR code. Most banking apps with Zelle integration let you generate a unique code that’s tied directly to your account. It’s a completely touchless and secure way to handle a transaction.

Here’s how simple it is:

Using a QR code or a payment request takes the guesswork out of the equation. Both methods ensure the sender's app has your correct, verified Zelle details before any money is sent, which is the best defense against payment errors.

This is especially handy when you’re dealing with someone you don’t know well, like when you're selling furniture on Facebook Marketplace. It feels more professional and secure, and you won’t have to chase them down later because they mistyped your email address.

Knowing which details to share is only half the story. To truly protect yourself, you need to build the right security mindset for using Zelle. Scammers love to exploit the platform's speed and finality, so you have to be one step ahead.

Here's the single most important rule: treat Zelle like digital cash.

Once you hit send, that money is gone in minutes. In almost every case, it's impossible to get back. That's why you should only ever send payments to people you personally know and trust—think family, close friends, or your landlord.

Scammers work by creating a false sense of urgency. They’ll pressure you to pay instantly for something like a concert ticket or a puppy from an online ad. A classic move is the "accidental overpayment" scam, where they send a fake alert saying they paid too much and beg you to send back the difference.

You have to be skeptical of unexpected payment requests, even if they look like they’re from someone you know. It’s shockingly easy for scammers to spoof phone numbers or hack social media accounts to impersonate people and ask for cash.

Keep an eye out for these warning signs:

Despite these risks, the system is surprisingly secure overall. You enroll once, share your number or email, and money arrives in minutes. While Zelle has grown massively, fraud remains negligible at just 0.02% of reported activity, meaning 99.98% of transactions are completed without issue.

The Golden Rule of Zelle: Only send money to people you know and trust. If you wouldn’t hand a stranger a wad of cash, don’t send them a Zelle payment.

This one principle is your best defense against phishing and impersonation schemes, which are rampant on almost every digital platform. The tactics are often the same, which you can see in our guide on how to spot a Coinbase phishing email.

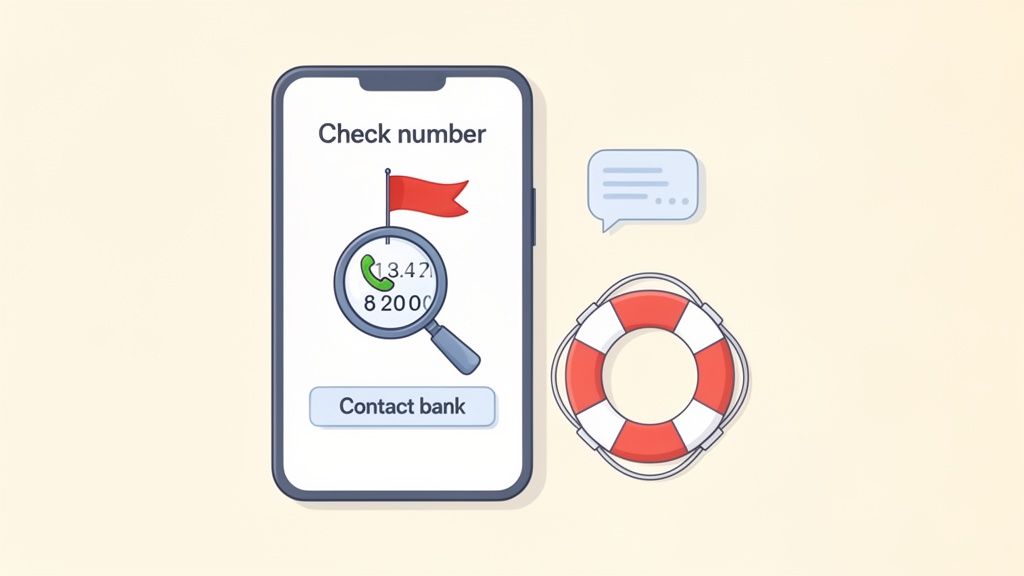

Even with the best intentions, things can go sideways. A simple typo can send your money to a complete stranger, or your friend might swear the payment never showed up. Don’t panic—let’s walk through how to sort out these common hiccups.

If you sent cash to the wrong person, your first move is to check the transaction status in your app. If it’s still marked as "Pending," you might be in luck and can cancel it. But if the recipient is already enrolled with Zelle, the money is gone instantly. It's just like handing someone cash. Your only real option here is to contact them, explain the mistake, and politely ask for your money back.

Sometimes the problem isn’t a typo but an enrollment snag. If the recipient claims the money never arrived, the first thing they should do is confirm they're enrolled with the exact phone number or email you used. It's a surprisingly common mix-up.

Here is a quick checklist to troubleshoot payment issues:

Always take a second to double-check every detail before hitting that "Send" button. Because Zelle payments are immediate, preventing a mistake is a whole lot easier than trying to fix one.

This straightforward process is a big reason why Zelle has become so popular, reaching 151 million enrolled accounts by 2024. By sticking to just a phone number or email, it keeps your more sensitive financial data out of the picture. You can learn more about the trends driving Zelle's massive growth and see why this simple approach works.

Getting paid with Zelle is fast, but it's normal to have a few questions before you share your details. Let's clear up some of the most common ones so you can send and receive money with confidence.

You sure can. If you send money to someone whose bank isn't in the Zelle network, they'll just get a text or email.

That message walks them through how to enroll with the standalone Zelle app to claim their money. It's a surprisingly smooth process.

This is a common and costly mistake. If that old number is still tied to a bank account you enrolled with Zelle, the money will go there.

It's crucial to update your contact information in your banking app the moment your phone number or email changes. A quick update can save you a huge headache.

Technically, both are equally secure within Zelle's system. But from a privacy standpoint, many people prefer sharing a dedicated email address for payments.

This is a smart move if you're transacting with people you don't know well. It keeps your personal phone number out of the hands of strangers.

Zelle, and legitimate organizations like charities, will never ask for payment or donations through unusual methods. For example, the No Kid Hungry campaign has warned that they will never request donations via personal Zelle accounts, gift cards, or Venmo. Always verify the source.

This is the big one: you can only cancel a payment if the recipient has not yet enrolled with Zelle.

If they're already set up, the money moves directly into their bank account in minutes and it's gone. That's why you have to double-check every detail—the name, the number, the amount—before hitting send.

At Wallet Finder.ai, we turn complex on-chain data into clear, actionable signals. Discover profitable traders and mirror their strategies in real time to get ahead of the market. Start your 7-day trial and see how smart money moves at https://www.walletfinder.ai.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.