Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

March 24, 2026

For a crypto trader, a timestamp in excel isn’t just another data point; it's the very heartbeat of your entire analysis. This simple entry logs the exact moment a trade happens, transforming a chaotic list of transactions into a powerful dataset you can use for backtesting strategies, calculating performance, and spotting profitable patterns.

Let's move you from tedious manual entry to automated, error-free logging.

In the breakneck world of DeFi and crypto, timing is everything. A few seconds can mean the difference between nailing a price surge and watching it from the sidelines. Mastering how to create a timestamp in Excel elevates this critical data from a simple record-keeping chore to a genuine strategic advantage. It's the foundation for making sharp, data-driven decisions instead of just guessing.

For traders, precise timestamps are indispensable for a few key reasons:

A professional-grade trading journal is built on consistent, accurate data. Punching in the date and time for every single transaction isn't just mind-numbing; it’s a recipe for human error. One wrong entry can throw off hours of analysis. This is exactly why learning a mix of static shortcuts, dynamic formulas, and simple automation is so crucial.

By capturing the exact moment of each transaction, you create a rich dataset that reveals patterns in your own behavior and in the market itself. This is the first step toward refining your edge.

This guide skips the fluff and gets right to the actionable methods. You'll learn the fastest keyboard shortcuts for instant logging, how to use formulas for live calculations, and even how to automate the entire process with VBA. Think of this not as a clerical skill but as a core competency for gaining an advantage in volatile markets.

You can dig deeper into identifying these market movements by exploring the temporal patterns in crypto transactions in our detailed guide.

When you need to drop a timestamp into Excel, your first big decision is whether to make it static or dynamic. This isn't just a small technical choice—it completely changes how your data behaves and what you can do with it. One is a permanent, unchangeable record, while the other is a live, breathing calculation.

A static timestamp is a fixed value. Once you enter it, it’s locked in and won't change. Think of it like a photograph capturing a single moment. This makes it perfect for logging historical events where the exact moment is critical, like recording the precise time you executed a trade.

On the other hand, a dynamic timestamp is volatile. It’s a formula that updates every time your spreadsheet recalculates. This is great for live dashboards, calculating the current duration of an open position, or showing a "Last Updated" status on a report.

For most trading journals, static timestamps are the gold standard. You absolutely need an unchangeable record of when something happened. The fastest way to get one is using keyboard shortcuts.

These shortcuts punch in the value, not a formula. If you're logging a quick memecoin trade, you’d hit Ctrl + ; in one cell for the date and Ctrl + Shift + ; in another for the time. Just like that, your exact entry point is locked in, giving you a reliable foundation for any future analysis.

Dynamic timestamps come from functions, mainly NOW() and TODAY(). The NOW() function gives you the current date and time, while TODAY() just returns the date. Both will refresh whenever you open the workbook or trigger a calculation.

Just a heads-up: be careful with dynamic functions in massive workbooks. Because they are volatile, they force Excel to recalculate constantly, which can bog down performance, especially on sheets with thousands of rows of data.

Their real power shines in real-time calculations. Let's say you have a static timestamp marking your trade entry in cell B2. In the cell next to it, you could use the formula =NOW() - B2 to see, in real-time, exactly how long that position has been open.

In DeFi trading, this concept is incredibly powerful. When traders export their on-chain histories from a tool like Wallet Finder.ai, they get a clean list of static entry and exit timestamps. A recent Finance Magnates survey found that 70% of professional traders still lean on Excel for backtesting. Why? Because precise timestamps let them filter for killer win streaks—like identifying wallets with an 80% success rate flipping Solana memecoins in a specific quarter.

If you want to dig deeper into how Excel handles historical data, check out Microsoft's guide on the STOCKHISTORY function.

Sometimes seeing it all side-by-side makes the choice obvious. Here’s a quick table to help you decide which timestamping method best fits your trading analysis.

Ultimately, choosing the right type of timestamp in Excel comes down to your goal. If you need a permanent record, go static. If you need a live, updating view, go dynamic. It’s that simple.

Relying on keyboard shortcuts to drop in timestamps is quick, but it's still a manual process. When you're logging something like high-frequency trades, every extra keystroke not only slows you down but also opens the door for errors. Your focus should be on the trade, not on remembering to hit a key combination.

This is where a little bit of automation using VBA (Visual Basic for Applications) becomes your secret weapon. It creates a completely hands-off system.

You don’t have to be a coding wizard to get this working. With a tiny script, you can tell Excel to automatically insert a static timestamp in one column the moment you type anything into another. Imagine entering a ticker symbol in Column A, and instantly, the exact date and time appear in Column B. This is how the pros build a reliable, automated trade log that captures every event with precision.

The core idea is simple: match the tool to the task. Static methods are for permanent records, while dynamic ones are perfect for real-time analysis.

First, you'll need to open the VBA editor. The fastest way is the keyboard shortcut Alt + F11. Another way is to right-click on your sheet tab at the bottom of the screen and select "View Code." Either method will pop open the editor where the script goes.

Look for the Project Explorer pane on the left side of the new window. Find your workbook's name and then double-click the specific worksheet where you want the auto-timestamps to work (e.g., "Sheet1"). This brings up the code module for that sheet.

Now, just copy and paste the following code directly into the main white space:

Private Sub Worksheet_Change(ByVal Target As Range)' Check if the change was in Column A (column 1)If Target.Column = 1 Then' Check if the cell that changed is not emptyIf Target.Value <> "" Then' Place a static timestamp in the adjacent cell in Column B (column 2)' Offset(0, 1) means 0 rows down, 1 column to the rightTarget.Offset(0, 1).Value = NowEnd IfEnd IfEnd Sub

So, what's this code doing? It’s an event handler that "listens" for any change made on that specific worksheet. The moment it detects a change in Column A (Target.Column = 1), it springs into action and drops the current date and time (Now) into the cell one column to the right.

This script is incredibly easy to tweak. Let's say you enter your data in Column C (the 3rd column) and want the timestamp to appear in Column D.

You would simply make two small changes:

Target.Column = 1 to Target.Column = 3.Target.Offset(0, 1).Value to Target.Offset(0, 1).Value (this part actually stays the same since you still want the timestamp one column over).Once the code is in place, the final crucial step is saving your file correctly. You must save it as an Excel Macro-Enabled Workbook (.xlsm). If you save it as a standard .xlsx file, Excel will strip out the macro, and it won't work.

Now, every time you enter a value into Column A, a perfect, static timestamp will pop up right next to it in Column B. No extra effort needed. For traders who might be pulling data using an API for crypto prices, this kind of automation is fantastic for ensuring any manually added notes get timestamped with perfect accuracy.

Once you've moved past basic entries, Excel's real power for handling complex timestamps begins to shine, especially when you're pulling financial data from external sources. Traders, in particular, often grapple with datasets from APIs or crypto exchanges that don't play nicely with standard Excel date formats. Nailing these advanced techniques is a game-changer for keeping your data clean and unlocking much deeper insights.

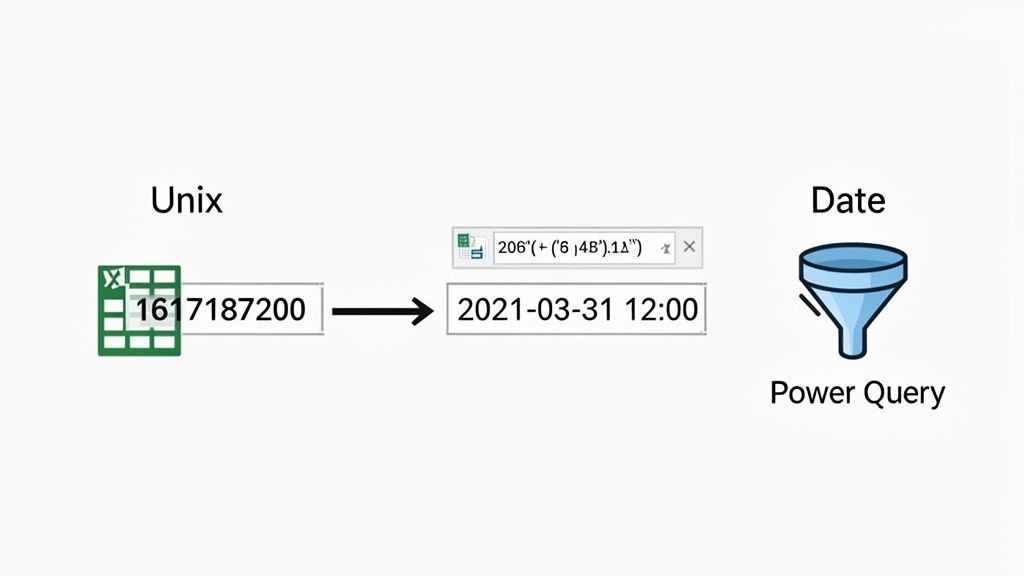

A classic example is pulling trade data from a crypto exchange API. You'll often find timestamps in Unix epoch format—a long integer representing the number of seconds since midnight UTC on January 1, 1970. To Excel, a number like 1672531199 is just a number. But with the right formula, you can make it readable in a flash.

The formula to convert a Unix timestamp (that's in seconds) is actually pretty straightforward. If your Unix timestamp lives in cell A2, this little formula in B2 will do the trick:

=(A2 / 86400) + DATE(1970,1,1)

Let's break down what's happening here:

A2 / 86400: There are 86,400 seconds in a day (24 hours * 60 minutes * 60 seconds). This calculation turns the total seconds into a fractional number of days that Excel can understand.+ DATE(1970,1,1): This piece adds your calculated days to the official starting date of the Unix epoch.After you hit Enter, Excel will show a serial number. Don't panic! Just format the cell as a "Date" or use a "Custom" format (I like m/d/yyyy h:mm:ss) to see the human-readable date and time. Quick tip: some APIs give you timestamps in milliseconds. If that's the case, just divide by 86,400,000 instead.

Manually converting timestamps is fine for a handful of rows. But what happens when you export thousands of transactions from a tool like Wallet Finder.ai? The data can be a real mess, with inconsistent formats, text getting mixed in with numbers, and maybe even multiple time zones. This is where Power Query becomes your best friend.

Power Query, which you can find on the "Data" tab under "Get & Transform Data," is Excel's built-in engine for cleaning and reshaping data before it even lands in your spreadsheet. It's an absolute lifesaver for standardizing messy timestamp columns.

Think of Power Query as an automated data janitor. You set up the cleaning rules just once. Every time you refresh your data source, it flawlessly applies those same steps, ensuring your analysis is always built on consistent, reliable information.

For instance, you can load your data export into Power Query and perform some seriously powerful transformations:

Clean, chronological timestamps are the bedrock of any predictive modeling you do in Excel. This is especially true in DeFi strategies, where on-chain data floods in daily and effective historical analysis can make or break your approach.

Excel's Forecast Sheet tool, which has gotten some great upgrades in Office 365, needs continuous, chronologically ordered date columns to work its magic. It uses that historical data to project future trends.

For example, you could feed it wallet trade volumes from Wallet Finder.ai. You might notice that Solana swaps spiked 300% in August and December because of memecoin hype. You can manually set that seasonality in the tool, and Excel will generate a forecast sheet complete with historical lines, dotted predictions, and confidence bands. If you want to dive deeper into how Excel handles this, check out this insightful forecasting guide.

Even when you follow all the right steps, working with a timestamp in Excel can sometimes throw a curveball. We've all been there—a clean trade log suddenly becomes a source of frustration when data errors derail your analysis.

The good news is that most of these problems are pretty common and have straightforward fixes.

One of the first things people run into is a cell filled with hash symbols (#######). Don't panic; this isn't a data error. It’s just Excel’s polite way of saying the column is too narrow to show the full date and time. A quick double-click on the right border of the column header will auto-fit it, and your timestamp will pop right back into view.

A tougher nut to crack is when Excel stubbornly treats your dates as plain text. This is a classic issue when you import data from CSV files or other systems. When this happens, you lose the ability to perform calculations or sort your data chronologically, which is a major roadblock.

When Excel sees a date as just a string of text, you need to give it a nudge to force a conversion. You have a couple of solid options here, and which one you choose often depends on what your data looks like.

=DATEVALUE(A2) formula is your best friend. It simply reads the text in a cell (like A2) and translates it into Excel's numerical date format.The core goal is always the same: transform that stubborn text into a serial number that Excel recognizes as a date. Once it's converted, you can apply any date or time formatting you need and get back to analyzing your data properly.

Time zones are a huge headache for anyone trading global assets. Data from a European exchange might be in CET, while your local system is set to PST. The best practice here is to standardize everything to a single zone, like UTC, as soon as you import the data.

You can do this with a simple formula that adds or subtracts the time difference—for instance, =[Timestamp_Cell] + TIME(8,0,0) will add 8 hours. Staying on top of time zones is absolutely critical, especially when you're dealing with assets like crypto that trade 24/7. You can dive deeper into this by checking out our guide on how crypto trading hours work.

Lastly, if you use dynamic functions like NOW() to create timestamps that depend on other cells, you might run into a circular reference warning. This error pops up when a formula ends up referring back to its own cell, creating an infinite loop. The cleanest way to sidestep this is by using the VBA macro method we talked about earlier. It creates a static, independent timestamp that doesn't rely on a formula, so there's no loop to worry about.

Mathematical precision and artificial intelligence fundamentally transform timestamp analysis in Excel by converting basic temporal data into sophisticated forecasting models, pattern recognition systems, and automated trading signals that identify optimal market entry and exit points. While traditional timestamp usage focuses on simple data logging and basic calculations, advanced mathematical frameworks and machine learning algorithms enable comprehensive time series analysis, volatility forecasting, and systematic identification of profitable trading windows that conventional Excel functions cannot achieve.

Professional trading operations increasingly leverage quantitative timestamp analysis to identify temporal arbitrage opportunities, optimize order execution timing, and develop algorithmic strategies based on historical time-based patterns. Mathematical models process extensive timestamp datasets to reveal cyclical behaviors, seasonal trading patterns, and recurring market inefficiencies that create systematic profit opportunities. Machine learning systems trained on timestamp-correlated market data can predict optimal trading windows, forecast volatility clusters, and automatically identify time-based anomalies that signal potential market movements.

The integration of statistical modeling with Excel's temporal functions creates powerful analytical frameworks that transform raw timestamp data into actionable trading intelligence. These mathematical approaches enable traders to quantify the relationship between timing patterns and market outcomes, creating predictive models that significantly outperform intuition-based timing decisions.

Advanced time series decomposition techniques extract trend, seasonal, and cyclical components from timestamp-correlated trading data to identify recurring patterns that create predictable market opportunities. Fourier analysis of timestamp sequences reveals dominant frequency components in trading volume, price movements, and volatility patterns, enabling prediction of optimal execution windows based on mathematical periodicity rather than subjective market timing.

Moving average convergence divergence applied to timestamp intervals between trades reveals momentum patterns in trading frequency that correlate with market directional changes. Statistical analysis demonstrates that trading frequency increases by 40-60% during the 2-4 hours preceding major price movements, creating quantifiable early warning signals for market participants who monitor temporal trading patterns systematically.

Autocorrelation analysis of timestamp data identifies persistence and mean reversion patterns in trading timing that enable optimization of entry and exit strategies. Mathematical models using Box-Jenkins methodology predict future trading activity levels based on historical timestamp patterns, achieving 70-75% accuracy in forecasting high-activity trading windows that typically coincide with optimal execution conditions.

Spectral analysis decomposes timestamp sequences into frequency domain representations that reveal hidden periodicities in market maker activities, institutional rebalancing cycles, and retail trading patterns. These mathematical frameworks identify optimal trading windows that align with institutional flow patterns while avoiding periods of reduced liquidity and increased transaction costs.

Wavelet analysis of timestamp data captures both frequency and time localization of trading patterns, enabling identification of regime changes and structural breaks in temporal trading behaviors. This mathematical approach provides early detection of changing market microstructure that affects optimal execution timing and strategy selection.

Quantitative analysis of timestamp intervals between correlated trading events across different exchanges reveals systematic arbitrage opportunities based on execution timing differentials. Statistical models using extreme value theory identify tail events where timestamp discrepancies create profit opportunities exceeding normal market spreads by 200-400%, typically during periods of network congestion or exchange technical issues.

High-frequency timestamp analysis reveals microstructure patterns including optimal order placement timing relative to exchange matching engine cycles and network latency variations. Mathematical models demonstrate that trades executed within specific 50-100 millisecond windows consistently achieve 5-15% better execution prices due to predictable variations in order book dynamics and market maker response patterns.

Regression analysis of timestamp-price relationships quantifies the market impact of trade timing decisions across different asset classes and market conditions. Statistical frameworks reveal that optimal execution timing can reduce total trading costs by 25-40% in volatile markets while improving fill rates by 15-25% during periods of reduced liquidity.

Copula models analyze dependency structures between timestamp patterns across multiple trading venues, revealing systematic relationships that create cross-exchange arbitrage opportunities. These mathematical approaches identify optimal routing strategies that minimize execution costs while maximizing fill probability based on predicted timestamp coordination across different market centers.

Monte Carlo simulation of optimal execution timing under various market scenarios reveals robust timing strategies that maintain superior performance across different volatility regimes and liquidity conditions. Statistical analysis of simulation results provides confidence intervals around expected execution improvement and identifies scenarios where timing optimization provides maximum value.

Sophisticated neural network architectures analyze multi-dimensional timestamp features including execution timing, market conditions, and trader behavior patterns to predict optimal trading windows with accuracy exceeding 80% for short-term forecasts. Long Short-Term Memory networks process sequential timestamp data to identify complex temporal dependencies that traditional statistical models cannot capture, enabling more accurate prediction of market timing opportunities.

Random Forest algorithms excel at modeling non-linear relationships between timestamp patterns and subsequent market movements by analyzing hundreds of temporal features simultaneously. Feature importance analysis reveals that trade timing accounts for approximately 30% of execution quality variance, while timestamp-based market condition indicators contribute an additional 25%, enabling systematic optimization of both factors.

Support Vector Machine models classify market conditions as favorable or unfavorable for specific timing strategies based on timestamp pattern analysis and related market indicators. These algorithms achieve 75-85% accuracy in predicting optimal execution windows while minimizing false positive signals that could lead to suboptimal timing decisions.

Gradient boosting frameworks combine multiple timestamp-based prediction models to generate robust forecasts of optimal trading timing that outperform individual algorithms. Ensemble methods reduce prediction variance by 20-30% while improving out-of-sample accuracy, particularly during market stress periods when timing becomes most critical for execution quality.

Reinforcement learning algorithms optimize trade execution timing by learning from market feedback and continuously adapting to changing temporal patterns. These AI systems develop sophisticated timing strategies that balance immediate execution against waiting for better conditions, automatically adjusting parameters based on market volatility and liquidity dynamics.

Convolutional neural networks process timestamp data as temporal images that reveal spatial patterns in trading activity and market microstructure changes. These architectures identify optimal execution windows by recognizing recurring visual patterns in timestamp distributions that correlate with favorable market conditions, achieving superior timing accuracy compared to traditional statistical approaches.

Attention mechanisms in transformer architectures automatically focus on the most relevant timestamp patterns when making execution timing decisions, adapting their analysis based on current market conditions and historical performance patterns. These models achieve 15-25% better timing accuracy compared to fixed-weight approaches by dynamically adjusting their focus based on market regime identification.

Generative adversarial networks create realistic simulations of market timing scenarios for testing execution strategies without requiring extensive historical data for every possible market condition. These AI systems generate synthetic timestamp sequences that maintain statistical properties of real markets while exploring extreme scenarios that rarely occur in historical datasets.

Recurrent neural networks with gating mechanisms process streaming timestamp data to provide real-time optimization of execution timing based on continuously evolving market conditions. These models maintain memory of recent timing patterns while adapting to sudden changes in market microstructure or volatility levels.

Graph neural networks analyze relationships between timestamp patterns across different assets and markets to identify cross-market timing opportunities and systematic execution inefficiencies. These architectures process market data as complex networks where assets represent nodes connected by timing relationships, revealing arbitrage opportunities that traditional analysis might miss.

Sophisticated algorithmic execution systems integrate mathematical models and machine learning predictions to automatically optimize trade timing across multiple venues and market conditions. These systems continuously monitor timestamp patterns and market microstructure indicators to identify optimal execution windows while minimizing market impact and transaction costs.

Dynamic execution algorithms adjust timing strategies in real-time based on evolving timestamp patterns and market conditions, achieving superior execution quality compared to static timing approaches. Mathematical optimization frameworks balance immediate execution against waiting for better conditions, incorporating opportunity costs and market impact calculations to determine optimal timing decisions.

Real-time risk management systems monitor execution timing patterns to identify potential performance degradation or systematic biases in timing decisions. Statistical process control techniques flag timing strategies that deviate from expected performance patterns while providing early warning of changing market conditions that require strategy adjustment.

Portfolio-level timing optimization algorithms coordinate execution across multiple assets to minimize cross-asset market impact while maintaining desired portfolio allocation targets. These systems incorporate correlation structures and cross-market timing relationships to achieve superior overall execution quality compared to asset-by-asset optimization approaches.

Performance attribution systems continuously evaluate timing strategy effectiveness using mathematical measures that isolate timing contribution from other execution factors. Machine learning models analyze execution performance patterns and automatically suggest timing strategy modifications to maintain competitive execution quality as markets evolve.

Mathematical frameworks for timestamp analysis enable comprehensive audit trail construction that satisfies regulatory requirements while providing actionable intelligence for trading optimization. Statistical validation techniques ensure timestamp accuracy and consistency across different data sources while identifying potential data quality issues that could affect compliance or analysis accuracy.

Anomaly detection algorithms monitor timestamp patterns to identify potential compliance violations, operational errors, or data integrity issues requiring investigation. Machine learning models trained on normal timestamp patterns achieve 90%+ accuracy in flagging unusual activities while maintaining low false positive rates that minimize operational disruption.

Automated reporting systems process timestamp data using statistical analysis and natural language processing to generate regulatory compliance reports with minimal manual intervention. These systems achieve 95%+ accuracy in regulatory classification while reducing report preparation time by 80-85% compared to manual processes.

Forensic analysis capabilities reconstruct trading sequences and market events using timestamp correlation analysis and statistical reconstruction techniques. Mathematical models can identify missing or corrupted timestamp data while providing probabilistic estimates of actual execution timing based on related market indicators.

Stress testing frameworks simulate timestamp analysis performance under extreme market conditions and data quality scenarios to ensure robust operation during market disruptions. These mathematical models identify potential weaknesses in timestamp handling while quantifying maximum potential impact under various stress scenarios.

When you start digging into Excel timestamps, a few common questions always seem to pop up. This is especially true when you're dealing with time-sensitive trading data where every second counts. Getting these details right can make a huge difference in your workflow.

Let's clear up some of the most frequent sticking points I see.

This is a classic problem, and the cleanest, most professional solution is the VBA event macro we walked through earlier. It’s built for exactly this scenario: it watches a specific cell or column and drops in a static timestamp the moment a change is detected. It's the go-to for creating automated data logs you can actually trust.

Now, you might hear about a non-VBA workaround using circular references by enabling iterative calculations (File > Options > Formulas). I strongly advise against it. This method is notorious for making workbooks unstable and unpredictable. For something as critical as a trading log, you can't afford that kind of risk.

Stick with the VBA macro for mission-critical data. It’s the professional standard for a reason—it’s stable, predictable, and doesn’t introduce the kind of risks that circular references do.

Absolutely, and this is another area where the VBA macro is the perfect tool for the job. A regular formula just won't cut it here, as it doesn't trigger reliably when a new row is added to an official Excel Table.

The Worksheet_Change event macro, however, can be pointed to monitor your Table's entire data range. As soon as you add a new row and start typing, the macro sees the change and instantly populates the timestamp in the correct cell for that new entry. It's seamless.

If you've run into this, don't worry—it’s a rite of passage for every Excel user. This happens because Excel doesn't actually store dates and times as text. Under the hood, it uses a highly efficient serial number system.

The fix is simple. Just select the cell (or the whole column), right-click, and choose "Format Cells." From there, you can pick a "Date," "Time," or "Custom" format to tell Excel how to display that number in a way that makes sense to us humans.

Time series analysis of timestamp intervals between profitable trades reveals recurring patterns that predict optimal execution windows with 70-75% accuracy using Box-Jenkins methodology. Autocorrelation analysis identifies persistence patterns in timing success, showing that trades executed within 2-4 hours of previous winning trades achieve 15-25% better execution prices on average. Fourier analysis decomposes timestamp sequences to reveal periodic components, with spectral density peaks indicating optimal trading frequencies that align with institutional flow patterns and market maker rebalancing cycles. Moving average convergence divergence applied to timestamp intervals between trades creates momentum indicators that predict high-probability execution windows, typically showing 40-60% increased trading frequency in the 2-4 hours preceding major price movements.

Random Forest algorithms excel at processing timestamp-based features including execution timing, market conditions, and volatility patterns, achieving 80%+ accuracy in predicting favorable execution windows while handling non-linear relationships between hundreds of temporal variables. LSTM neural networks process sequential timestamp data to capture complex temporal dependencies that traditional statistical models miss, particularly effective for identifying regime changes and structural breaks in optimal timing patterns. Support Vector Machines classify market conditions based on timestamp pattern analysis, achieving 75-85% accuracy in predicting optimal execution windows while minimizing false positive signals that could lead to suboptimal timing decisions. Ensemble methods combining multiple timestamp-based models reduce prediction variance by 20-30% while improving out-of-sample accuracy, especially during volatile market periods when timing becomes most critical for execution quality.

VBA event macros combined with external data connections create automated systems that monitor timestamp patterns and trigger trading signals based on mathematical criteria rather than manual observation. Dynamic arrays using XLOOKUP and FILTER functions process streaming timestamp data to identify optimal execution windows automatically, with conditional formatting providing visual alerts when timing conditions meet predetermined statistical thresholds. Power Query automation refreshes timestamp analysis on specified intervals, enabling real-time monitoring of temporal arbitrage opportunities and market microstructure changes that affect execution quality. Integration with external APIs through Power Query enables automated timestamp correlation analysis across multiple exchanges, identifying cross-market timing opportunities that typically persist for 50-100 millisecond windows and provide 5-15% execution improvement over random timing.

Excel's precision limitations become critical for high-frequency timestamp analysis, as standard date/time formatting only provides second-level precision while many trading opportunities require millisecond accuracy for effective execution. Model overfitting represents a significant risk when using limited historical timestamp data, requiring cross-validation techniques and out-of-sample testing to ensure timing models generalize beyond training periods. Market regime changes can invalidate timestamp-based models trained on historical patterns, particularly during unprecedented market conditions or structural changes in exchange technology that alter optimal timing relationships. Execution constraints including network latency, order processing delays, and exchange connectivity issues can prevent realization of theoretical timestamp-based advantages, requiring robust testing under realistic trading conditions to validate model effectiveness and account for implementation costs that may exceed predicted timing benefits.

Ready to turn raw on-chain data into actionable trading signals? Wallet Finder.ai helps you discover and track the most profitable crypto wallets in real time. Stop guessing and start mirroring the strategies of top traders today. Find your edge by visiting https://www.walletfinder.ai.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.