Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

February 11, 2026

When you start exploring ways to make your crypto work for you, one acronym pops up everywhere: APY. So, what is APY in crypto? Think of it as the real return you can expect on your digital assets over a year, because it accounts for the powerful effect of compounding interest. It's the key metric for comparing staking, lending, or yield farming opportunities in DeFi.

Imagine a snowball rolling downhill. It doesn't just get bigger it picks up more snow faster and faster as it grows. That's compounding in a nutshell. Your earnings start generating their own earnings, creating a feedback loop of accelerated growth. This isn't a new concept; it's the foundation of wealth-building in traditional finance, too.

What’s different in crypto is the speed. A traditional bank might compound your interest monthly. A DeFi protocol, on the other hand, could compound your earnings daily, hourly, or even with every new block added to the blockchain—which is about every 12 seconds on Ethereum. You can see how crypto returns stack up against historical market data on platforms like CoinMarketCap. This rapid compounding is how a seemingly modest interest rate can balloon into an impressive annual yield.

This is where it’s super important to know the difference between APY and its simpler cousin, APR (Annual Percentage Rate). APR is just a flat rate. If a platform offers a 10% APR, you’ll earn exactly 10% on your initial capital over the year. Simple.

But a 10% APY that compounds daily will always result in a higher return because the interest you earn each day gets added back to your principal, and you start earning interest on that too.

The core takeaway is this: APY provides a more accurate picture of your potential earnings because it reflects the real-world impact of your returns generating more returns.

Getting this distinction right is the first step to properly comparing different yield opportunities across the crypto world. When you see a high APY, you know a big chunk of that projected return is coming from the protocol automatically reinvesting your profits for you. It puts your growth on autopilot, maximizing your potential without you having to lift a finger.

It's easy to glance at APY and APR and think they're just two ways of saying the same thing. But that common mix-up can be a costly one, especially in DeFi. The two metrics are fundamentally different, and knowing how they work is critical for figuring out what you’ll actually earn.

The entire difference boils down to one powerful concept: compounding.

Before we dive deep, let's get a high-level view of what separates these two core metrics. The main takeaway is that APY gives you a much truer picture of your potential earnings because it accounts for growth on your growth.

FeatureAPR (Annual Percentage Rate)APY (Annual Percentage Yield)CalculationSimple InterestCompounding InterestCompoundingExcludes the effect of compoundingIncludes the effect of compoundingReal-world ReturnDoesn't show the true annual returnShows the true annual returnUse CaseOften used for borrowing (loans, credit cards)Often used for earning (savings, staking)

Simply put, while both are annualized rates, APY will always be higher than APR for the same base rate, as long as interest is compounded more than once a year.

Let's break this down with a practical example.

Annual Percentage Rate (APR) is the straightforward, no-frills interest rate you earn on your principal investment each year. If a staking pool offers 10% APR on your $1,000 deposit, you'll walk away with exactly $100 in profit after one year. Clean and simple. Your earnings don't start earning anything themselves.

Annual Percentage Yield (APY), on the other hand, is the metric that shows you what you really get. It includes the magic of compounding interest. APY calculates the return you earn not just on your initial capital, but also on the accumulated interest that gets added back to your principal over and over again.

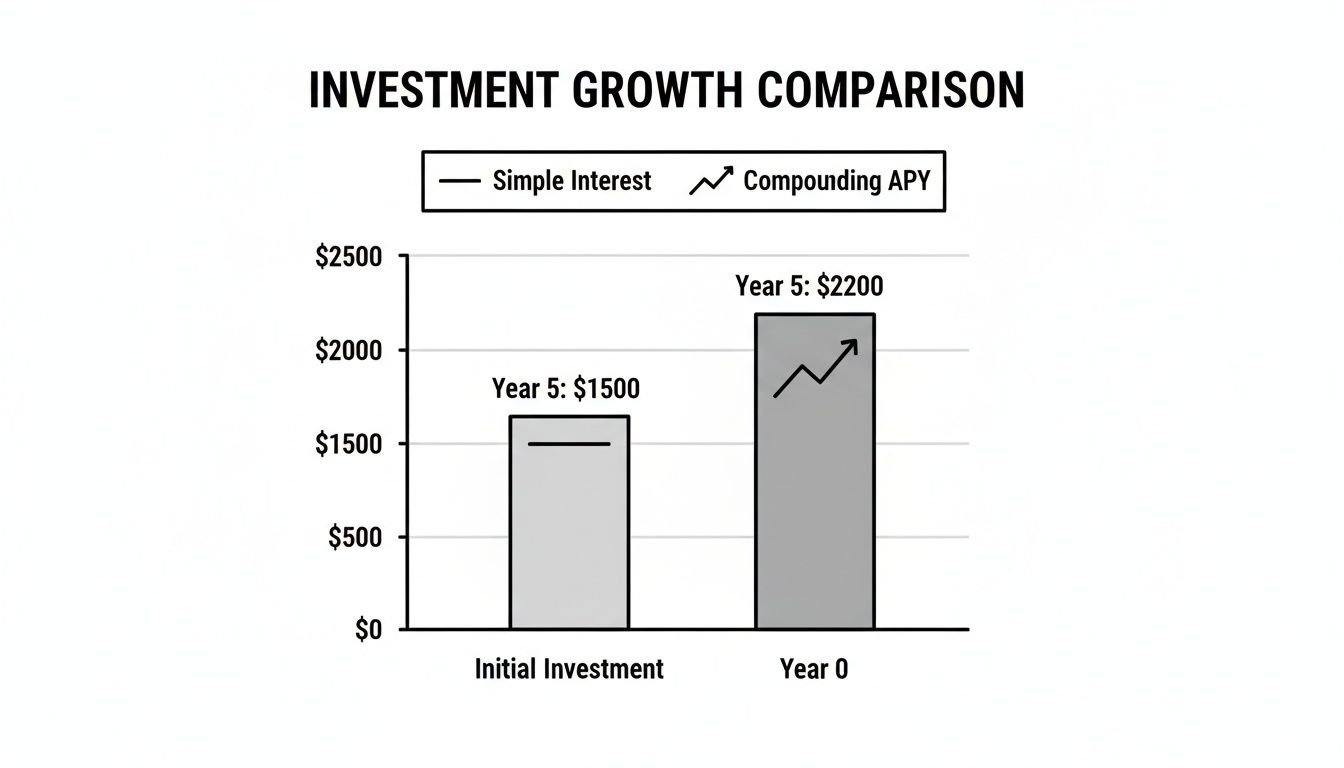

Imagine you have two protocols to choose from. Both offer a 10% rate on a $1,000 investment.

Sure, an extra $5 might not sound like much, but that gap gets exponentially wider with larger investments, higher rates, and longer time horizons.

The key takeaway is simple: For the same stated interest rate, an investment calculated with APY will always yield a higher return than one calculated with APR because your earnings start working for you.

This chart shows it perfectly. Look at how an initial investment grows with simple interest versus the accelerating curve you get from compounding APY.

As you can see, the space between those two lines just keeps growing. That’s the power of compounding in action. When you're evaluating crypto opportunities, always hunt for the APY to understand the real potential of your investment.

Those eye-popping APY figures you see in crypto aren't just pulled out of thin air. They might seem too good to be true, but every single yield opportunity is backed by real economic activity happening on-chain. Getting a handle on where this yield comes from is the first step to understanding what you’re actually putting your money into.

At its core, the APY you earn from a DeFi platform is a reward. You're being compensated for providing something of value to the network, and this usually happens in one of three main ways. Each method is a critical gear in the decentralized machine, and you get paid for helping keep it running.

One of the most foundational ways to earn in crypto is through staking. This is the lifeblood of Proof-of-Stake (PoS) blockchains like Ethereum, Solana, and Cardano. When you stake your tokens, you’re locking them up to help verify transactions and secure the entire network.

Staking is what keeps a PoS network decentralized and strong. As a result, its APY is often seen as one of the most straightforward and fundamental forms of crypto yield.

Another huge source of crypto yield is lending. DeFi platforms like Aave and Compound essentially act as decentralized money markets. You can deposit your crypto into a lending pool, and it becomes available for other users to borrow.

Finally, many of the most attractive APYs come from being a liquidity provider (LP) on a decentralized exchange (DEX) like Uniswap or PancakeSwap. Instead of using old-school order books, DEXs use "automated market makers" (AMMs) that are powered by pools of tokens supplied by users like you.

If you want to go deeper, you can learn more about how crypto liquidity pools work and the mechanics that drive them. They are a cornerstone of the DeFi ecosystem.

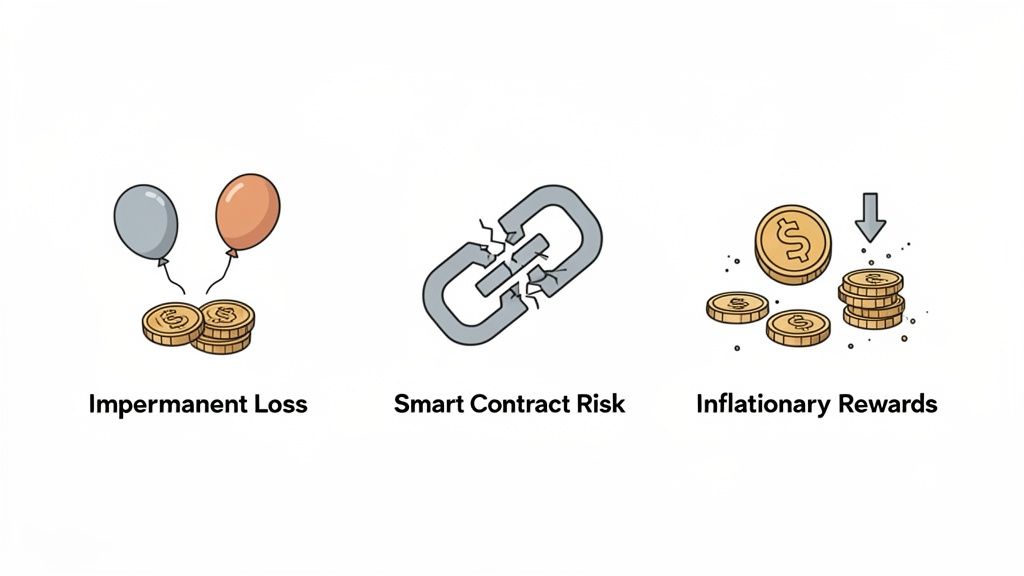

A massive, triple-digit APY looks incredible on paper, but in crypto, it’s almost never a free lunch. When you see a number that seems too good to be true, it’s usually a sign that you're being compensated for taking on serious, often hidden, risks. Understanding what is APY in crypto means digging deeper than the advertised rate.

The goal isn't to scare you away from high-yield opportunities. It's to give you a clear framework for making smart, risk-aware decisions. Let's pull back the curtain on the most common risks hiding behind those big APY numbers.

If you're providing liquidity, impermanent loss is one of the trickiest concepts to wrap your head around. It happens when the price of the tokens you deposited into a pool changes relative to each other. The bigger the price split between the two assets, the more "loss" you'll see compared to if you had just held them in your wallet.

When you eventually withdraw your funds, you could end up with less of the asset that performed well and more of the stable one. That difference in value is impermanent loss. It only becomes permanent when you cash out.

Every DeFi protocol is built on smart contracts—basically just lines of code running on the blockchain. While this code is what makes trustless finance possible, it can also have bugs, flaws, or exploits that hackers can target. A single vulnerability could be enough for a bad actor to drain every last dollar from a protocol.

Don't assume that only new, obscure projects are at risk. Billions have been lost to smart contract hacks, even on well-known platforms. This is why you should always check if a protocol has been audited by reputable security firms. You can learn more about these threats by reading up on smart contract security risks in liquidity pools.

Many DeFi protocols lure users in with insane APYs by paying them out in the protocol’s own native token. This reward mechanism, called token emissions, is really just a form of planned inflation. The project mints new tokens from thin air to reward you for participating.

The risk is basic supply and demand. If the protocol is constantly printing new tokens, it puts massive and continuous selling pressure on the price. Unless there's enough new demand to soak up all that new supply, the token's value is almost guaranteed to go down. This can create a brutal cycle:

An APY that comes entirely from inflationary rewards is often a ticking time bomb. Your real return could easily turn negative if the token's price crashes faster than you're earning it.

Here's an uncomfortable truth that nobody in DeFi marketing wants to discuss: many of the APY numbers you see are deliberately misleading, using clever accounting tricks and display manipulation to show rates that you'll never actually achieve. Understanding these manipulation tactics is essential for distinguishing between legitimate yields and marketing theater designed to extract your capital before the music stops.

The incentive structure creates this problem. Protocols compete desperately for total value locked because TVL is the primary metric investors use to judge legitimacy and potential. Higher displayed APY attracts more deposits, which increases TVL, which attracts more attention and investment. This creates powerful pressure to show the highest possible APY regardless of whether users can actually capture that rate in practice.

The most common manipulation involves displaying instantaneous rates that exist for minutes or hours rather than sustainable yields you could actually earn over meaningful timeframes. A protocol might show "473% APY" on their homepage, technically correct for that exact moment, but completely misleading about what you'd earn if you deposited funds today.

This happens because APY on many platforms gets calculated from the most recent reward distribution event, then annualized by multiplying that snapshot by the number of similar periods in a year. If a liquidity pool just had an unusually high-volume trading hour that generated triple the normal fees, the displayed APY temporarily spikes to reflect what would happen if every hour were equally profitable. But of course, trading volume isn't constant—most hours generate far less activity and thus far lower fees.

The manipulation becomes especially egregious during token launches or promotional events. A protocol might seed initial liquidity pools with heavy artificial incentives for the first week to generate explosive APY numbers that attract attention. Users see "2,000% APY" and rush to deposit, not realizing that rate only existed because the protocol was burning through marketing budget that won't last beyond the promotional period. Two weeks later, after everyone's already committed capital, the APY quietly drops to twenty percent—still decent, but nowhere near the advertised rate that convinced people to deposit.

Defending against this requires checking the APY history rather than just the current display. Many analytics sites show historical yield charts that reveal whether an APY has been stable or if it's wildly volatile with short-lived spikes. If you see a protocol advertising seventy percent APY but the historical chart shows it bouncing between ten and ninety percent weekly, you know the displayed number is cherry-picked from a temporary peak rather than representing sustainable returns.

The second major manipulation involves showing APY based on reward tokens you've accumulated but can't actually claim or sell yet. This "paper APY" looks fantastic in the protocol's interface but doesn't translate into real returns until those tokens unlock—which might be months or years away, if ever.

Vesting schedules create this problem. A protocol pays rewards in its native token, but those tokens are locked for six months before you can withdraw them. During that lock period, the protocol's dashboard shows your earned balance growing and calculates an APY based on that growing number. Technically accurate—you did earn those tokens at that rate. But functionally meaningless if you can't access the value.

The real manipulation happens when the protocol displays APY without clearly indicating that rewards are locked. Users see "80% APY," deposit funds expecting to harvest those rewards regularly, then discover their earnings are trapped in a smart contract for the next year. By the time tokens unlock, market conditions have usually changed dramatically—often the token's price has crashed from initial levels, turning that "80% APY" into a twenty-percent loss in dollar terms.

Even worse, some protocols implement partial unlock schedules where you can claim a small percentage of earned rewards immediately but the bulk remains locked for extended periods. The displayed APY includes all earned tokens, both locked and unlocked, creating the impression you're capturing the full rate when you're actually only accessing a fraction. A protocol might show "120% APY" when you can only claim fifteen percent of earned rewards monthly, making your effective accessible APY closer to eighteen percent.

The defense is reading the full terms before depositing. Always check whether rewards are immediately claimable, what the vesting schedule looks like if they're locked, and whether the displayed APY calculation includes locked tokens that you can't actually use. Protocols with transparent, user-friendly documentation clearly explain these mechanics. Protocols deliberately obscuring this information are usually hoping you won't notice until after you've already committed funds.

The third manipulation tactic involves advertising APY rates on pools with effectively zero liquidity, making the displayed numbers completely irrelevant to anyone considering meaningful deposits. A protocol might show "500% APY" on a brand-new token pair that has only ten thousand dollars in total liquidity. Technically true for someone depositing a hundred dollars. Functionally impossible for anyone wanting to deploy serious capital.

The math breaks down when you consider what happens if you try to deposit a meaningful amount into these tiny pools. That "500% APY" exists because rewards are distributed across a small existing liquidity base. When you deposit twenty-five thousand dollars into a ten-thousand-dollar pool, you've instantly tripled the total liquidity. The same reward emissions now get split among three times as much capital, immediately crushing the APY from five hundred percent down to around one hundred sixty-six percent for everyone in the pool, including you.

This dynamic creates a perverse situation where the displayed APY is only achievable if nobody actually tries to earn it. Small deposits from a few users maintain the high rate, but any substantial capital inflow destroys the economics. It's marketing bait—the high APY gets attention and drives traffic to the protocol, but users who actually deposit based on that rate immediately experience disappointment when their real yield is far lower than advertised.

Protecting yourself requires always checking total pool liquidity before trusting an APY figure. If a pool is advertising extraordinary rates but has less than one hundred thousand dollars in total value locked, that APY is essentially fake for anyone with real capital to deploy. The displayed rate only exists because the pool is empty, and it will collapse the moment you or anyone else actually uses it. Focus on pools with substantial liquidity—typically several million dollars minimum—where your deposit won't dramatically change the economics.

Every high-yield opportunity in crypto follows a predictable lifecycle from explosive launch rates through gradual decay to eventual stabilization or death. Understanding these decay patterns helps you time your entry and exit to capture maximum value while avoiding the disappointment of watching APY collapse after you've already committed capital.

The fundamental driver of APY decay is simple supply and demand economics. When a new yield opportunity launches with attractive rates, early users earn exceptional returns because they're splitting the reward pool among relatively few participants. As word spreads and more capital floods in, the same fixed reward budget gets divided among more and more depositors, mechanically crushing the individual APY that each participant receives.

APY opportunities move through four distinct phases, each with characteristic behaviors and strategic implications for when to enter and when to exit.

The discovery phase features the highest APY rates you'll ever see for a given opportunity—often hundreds or even thousands of percent annualized. These explosive numbers exist because reward emissions are substantial relative to the tiny amount of capital that's found the opportunity so far. Early adopters who discover the pool before it gains mainstream attention capture disproportionate value.

The strategic approach during discovery phase is moving fast but carefully. If you have strong conviction in a new protocol based on fundamental analysis, getting capital deployed during the first few days can be extraordinarily profitable. But you're also taking maximum smart contract risk before the platform has been battle-tested. The ideal risk-managed approach is deploying small test positions during discovery to verify the mechanics work correctly, then scaling up if the protocol performs well and security seems solid.

The discovery phase typically ends when the opportunity gets mentioned by influential crypto Twitter accounts, covered by news sites, or added to yield aggregator platforms. Once mainstream awareness hits, capital inflows accelerate dramatically and the transition to growth phase begins.

During the growth phase, APY steadily declines from the explosive launch rates as capital inflows accelerate. A pool that offered five hundred percent APY in week one might drop to two hundred percent by week three, then one hundred percent by week five as thousands of users pile in. The absolute reward emissions often remain constant, but they're getting split among exponentially more capital.

The strategic window during growth phase is recognizing when APY has stabilized at a level that still compensates you adequately for the risks but before it crashes to unattractive levels. If you enter during early growth phase—say when APY has already fallen from five hundred percent to two hundred percent but is still well above alternatives—you can capture solid returns for weeks before decay continues.

The challenge is knowing when growth phase is ending and saturation is beginning. Warning signs include TVL growth rate slowing, declining social media mentions as hype fades, and APY stabilizing in a tight range for several days rather than continuing its downward trajectory. When these signals align, it's often time to start planning your exit before the platform transitions to mature phase.

The mature phase is characterized by relatively stable APY that fluctuates in a predictable range rather than showing directional trends. A pool might oscillate between thirty and fifty percent APY based on normal fluctuations in trading volume or lending demand, but it's no longer experiencing the dramatic collapses of growth phase.

For many users, mature phase represents the sweet spot for actual deployment of serious capital. The protocol has been battle-tested for weeks or months without major exploits, the APY has stabilized at sustainable levels that adequately compensate for risk, and the wild volatility of early phases has passed. Conservative investors who missed the explosive early returns can still capture solid yields during maturity by deploying larger positions than they would have risked during discovery phase.

The strategic risk during mature phase is complacency. Just because APY has been stable for two months doesn't mean it will remain so indefinitely. Market conditions change, competitors launch new opportunities that pull liquidity away, and protocols adjust their reward emission schedules. Mature phase can persist for months or transition into decline phase surprisingly quickly if catalyst events trigger mass withdrawals.

The decline phase begins when some combination of falling rewards, rising competition, security concerns, or market sentiment shifts causes sustained capital outflows. As TVL decreases, the remaining capital is splitting the shrinking reward pool among fewer participants, but unlike early phases where this would boost APY, decline phase often features both falling TVL and falling total rewards as protocols cut emissions or users flee to greener pastures.

During decline phase, APY might remain nominally attractive, but this is usually a value trap. A pool showing eighty percent APY during decline might look better than new opportunities offering fifty percent, but that eighty percent is based on increasingly illiquid token rewards from a protocol losing market relevance. The real return in dollar terms is often negative as the reward token's price crashes faster than you can accumulate it.

The strategic approach during decline phase is simple: exit. Once clear signs of sustained decline appear—consecutive weeks of falling TVL, protocol tokens down seventy-five percent or more from peaks, major security incidents or team member departures—staying deployed hoping for a reversal is almost always a losing bet. Capital preservation becomes more important than squeezing out a few more weeks of diminishing rewards.

Timing your participation based on APY lifecycle requires watching multiple signals simultaneously rather than relying on any single metric.

For entry timing, the ideal window is late discovery or early growth phase—after initial smart contract risks have been tested by early adopters but before mainstream capital inflows have completely crushed rates. Look for opportunities that have been live for one to three weeks, have attracted several million in TVL showing real user interest, ideally have a successful audit or experienced team giving security confidence, but haven't yet been featured by major crypto news outlets or added to yield aggregator frontpages.

For exit timing, the signals are more nuanced. You don't want to exit just because APY has fallen from initial levels—that's expected and normal. Instead, watch for inflection points: TVL growing but APY falling faster than the TVL growth rate would predict suggests reward emissions are being cut; consistent week-over-week TVL declines for three-plus weeks straight indicate sustained capital flight; reward token price performing worse than the broader market consistently signals loss of confidence. When multiple negative signals align, that's your cue to harvest accumulated rewards and redeploy capital to earlier-phase opportunities.

The single most devastating mistake crypto yield farmers make is confusing nominal APY (the percentage rate displayed) with real APY (what you actually earn in dollar terms). A protocol can advertise one hundred percent APY and you can earn exactly one hundred percent more tokens while simultaneously losing fifty percent of your initial capital in dollar value. Understanding this disconnection between nominal and real returns is essential for avoiding the trap that wipes out most amateur yield farmers.

The core problem is that the vast majority of DeFi yields are paid in the protocol's native token rather than in stablecoins or established assets like ETH or BTC. When you stake PROTOCOL tokens and earn one hundred percent APY in more PROTOCOL tokens, your real return depends entirely on what happens to PROTOCOL's price while you're earning. If the token's price falls fifty percent, your real return is zero despite earning one hundred percent more tokens.

The worst-case scenario—which plays out with alarming regularity—is the yield death spiral where high APY directly causes token price collapse, destroying real returns for all participants no matter how high the nominal rate climbs.

Here's how it unfolds. A protocol launches with attractive yields paid in its native token, let's say one hundred percent APY. Users deposit capital and begin accumulating tokens at this rate. Everything seems great initially—you're earning tokens and the price is stable or even rising from early demand. Then users begin taking profits, selling earned tokens to lock in dollar gains or rebalance their portfolio.

This selling creates downward price pressure, which the protocol tries to counter by increasing reward emissions to maintain depositor interest. The APY climbs from one hundred percent to one hundred fifty percent, then two hundred percent as the protocol adds more rewards. But these increased emissions mean even more tokens flooding into user wallets, which means even more selling pressure when people harvest and convert to stablecoins.

The price falls further, which triggers more users to exit entirely, withdrawing their principal and dumping both staked tokens and accumulated rewards. TVL collapses, which makes the protocol increase rewards even more desperately to retain remaining users. APY climbs to three hundred percent, five hundred percent, one thousand percent—but the token price is falling faster than the APY is rising. Users who stayed loyal through the cycle end up with massive quantities of tokens worth nearly nothing, while those who exited early captured real gains.

This pattern repeats across countless DeFi protocols. The displayed APY goes parabolic while real returns go negative. Your wallet shows you earned three hundred percent more tokens, but those tokens are worth seventy percent less than when you started, giving you a real return of negative forty percent despite the "300% APY" that attracted you.

Protecting yourself requires manually calculating real APY by factoring in token price performance alongside nominal yields. The formula is straightforward but requires discipline to actually run the numbers rather than just checking your token balance.

Real APY equals the nominal APY percentage you earned in tokens, multiplied by the token's average price during your holding period, minus the token's price decline percentage. Let's work through a concrete example.

You deposit one thousand dollars into a protocol offering one hundred percent APY paid in REWARD tokens. After one year, you've earned exactly one hundred percent more tokens as advertised—your token balance doubled. Nominal APY achieved: one hundred percent. But during that year, REWARD's price fell from one dollar to sixty cents—a forty percent decline.

Your calculation: started with one thousand dollars worth of REWARD tokens. Earned one hundred percent more tokens, giving you two thousand dollars' worth at original prices. But token price fell forty percent, so those two thousand tokens are only worth twelve hundred dollars at current prices. Real return: two hundred dollars profit on one thousand dollar principal, or twenty percent real APY. Nowhere near the advertised one hundred percent.

If the token had fallen more severely—say from one dollar to twenty cents, an eighty percent decline—your math looks devastating. You doubled your tokens to two thousand dollars' worth at original prices, but token price fell eighty percent, so two thousand tokens are now worth four hundred dollars. Real return: six hundred dollars loss on one thousand dollar principal, or negative sixty percent real APY despite "earning" one hundred percent nominal.

Running this calculation monthly rather than just at the end helps you course-correct before small losses become catastrophic. If you check in month three and discover that your real return is already negative despite positive nominal APY, that's your signal to exit before the death spiral accelerates.

The contrast between token-denominated and stablecoin-denominated yields reveals exactly how much value the token price risk actually represents. When you see a protocol offering twenty percent APY in USDC versus one hundred percent APY in their native token, that eighty-percent differential is the market's estimate of how much the native token is likely to depreciate.

Sophisticated traders always compare stablecoin yields to token-denominated yields on similar-risk protocols. If the spread is too wide—say a protocol offers fifteen percent APY in stables but three hundred percent in native tokens—that's a flashing warning that the market expects catastrophic token depreciation that will wipe out the nominal gains.

Conversely, when the spread is narrow—a protocol offering eighteen percent in stables versus twenty-two percent in native tokens—that's a signal the market believes the token price will remain relatively stable, making the four-percent premium reasonable compensation for the additional price risk you're taking.

Using this spread analysis h

Now that you understand the risks, the next step is putting that knowledge to work to find good opportunities and sidestep the duds. Here is an actionable checklist for vetting any high-APY opportunity:

Actionable Checklist for Vetting Crypto APY

While metrics like TVL give you a bird's-eye view, a sharper strategy is to see where the seasoned DeFi pros are putting their own capital. By keeping an eye on the wallets of top traders, you can see:

This whole approach shifts your focus from chasing advertised numbers to following proven strategies. It’s a data-first way of thinking, based on what successful people are doing, not just what a protocol is promising.

Trying to track top wallets by hand is nearly impossible. That's where tools like Wallet Finder.ai come in, designed specifically to do the heavy lifting for you. They pull together all the on-chain data to show you exactly where the most successful traders are moving their funds, giving you actionable signals based on what's happening in real-time.

This level of analysis can uncover powerful trends. For instance, Wallet Finder.ai users who monitor winning wallet strategies often see top-tier traders rotating into new opportunities offering 25%+ APY right before those rates start to come down. The game has gotten so sophisticated that you can now even calculate risk-adjusted returns by looking at a protocol's historical performance.

By combining foundational metrics with the laser-focused insights you get from wallet tracking, you can build a repeatable process for vetting opportunities. This turns the question of "what is APY in crypto" into a practical strategy for finding legitimate high-yield chances. You can dive deeper with our guide to finding high APY crypto staking opportunities.

Even after getting the hang of the mechanics, a few questions always pop up when you're dealing with APY in crypto. Let's tackle the most common ones head-on to clear up any lingering confusion.

Yes, and you should expect it to. Unlike the fixed rates you might see at a bank, most crypto APYs are variable. They’re living numbers that can shift dramatically based on what’s happening in the market.

Several things can send an APY swinging, sometimes from one day to the next:

Because of this constant flux, you can't just "set it and forget it." You've got to keep an eye on your positions.

This is one of the most dangerous gaps in crypto investor knowledge—the tax implications of earning yield are complex and unforgiving, and most platforms provide zero guidance. In most jurisdictions including the United States, crypto rewards are taxed as ordinary income at the fair market value when you receive them, regardless of whether you immediately sell or continue holding.

The critical distinction is when the taxable event occurs. For staking and lending rewards, you typically owe taxes the moment rewards hit your wallet or become claimable, not when you eventually sell them. If you earn ten tokens worth one hundred dollars total in January but don't sell them until December when they're worth fifty dollars, you still owe ordinary income tax on the one hundred dollar value from when you received them. Then when you sell in December, you have a fifty-dollar capital loss that might offset other gains.

This creates a brutal scenario many yield farmers discover during their first tax season—you earned twenty thousand dollars in token rewards during the year, most of which you left staked to compound. The token price crashed and by year-end your entire accumulated balance is only worth five thousand dollars. But you still owe income tax on the full twenty thousand dollars of rewards you received throughout the year, creating a tax bill of potentially six to eight thousand dollars on tokens currently worth five thousand total. Many users end up forced to sell their entire position at depressed prices just to pay tax bills on earnings that evaporated.

The defensive strategy is setting aside a portion of earned rewards immediately to cover tax liabilities rather than compounding one hundred percent. If you're in a thirty-percent marginal tax bracket, you should be selling roughly one-third of earned rewards as you receive them to build your tax payment fund. This reduces your compound growth slightly but prevents the disaster of owing more in taxes than your entire position is worth.

No, and this is one of the most deceptive aspects of liquidity provision APY calculations. The displayed APY shows only the trading fees or reward tokens you earn, completely ignoring impermanent loss that might be simultaneously eroding your position's value. You can earn twenty percent APY from fees while suffering thirty percent impermanent loss, resulting in a net ten-percent loss despite the attractive displayed yield.

Impermanent loss occurs when the relative prices of the two tokens in your liquidity pool diverge from when you deposited. The automated market maker rebalances your position, giving you more of the token that decreased in price and less of the token that increased. When you withdraw, you have a different mix of tokens than you deposited, and if one token significantly outperformed, your final balance will be worth less than if you'd simply held the original tokens.

The problem is that impermanent loss only becomes visible when you actually withdraw from the pool. While you're providing liquidity, your dashboard shows your LP token value growing from earned fees, but it doesn't show the hidden impermanent loss accumulating behind the scenes. Users see their balance going up and assume they're profitable, not realizing they'd be even more profitable if they had just held the tokens instead of providing liquidity.

Calculating your true net APY from liquidity provision requires manually comparing your final withdrawn value against what you would have gotten by simply holding. If you deposited one thousand dollars of ETH and USDC, earned two hundred dollars from fees over the year (twenty percent APY), but the final withdrawn value is only one thousand fifty dollars because impermanent loss ate one hundred fifty dollars, your true net APY was five percent, not twenty. Many liquidity providers never run this calculation and therefore never realize their actual returns were far lower than the attractive APY suggested.

Auto-compounding and manual claiming represent fundamentally different approaches to managing earned rewards, with significant implications for your real returns over time. Auto-compounding protocols automatically harvest your earned rewards and immediately reinvest them into the same position, creating continuous compounding without requiring any action from you. Manual claiming protocols require you to periodically harvest rewards yourself and then manually reinvest if you want compounding benefits.

The mathematical advantage of auto-compounding is substantial over longer timeframes. If you're earning one hundred dollars daily in a manual-claim protocol and only harvest every seven days, those rewards sit idle for an average of three-and-a-half days before you reinvest them. That's three-and-a-half days where they're not generating any returns. Over a year, this delay costs you roughly seven to eight percent of potential compound growth compared to if those rewards were reinvested instantly.

Auto-compounding protocols eliminate this lag by reinvesting your rewards continuously—often multiple times per day as new rewards accumulate. This maximizes the compounding effect since your earnings start generating their own earnings with near-zero delay. However, auto-compounding typically comes with a cost—either explicit fees charged by the protocol for managing the auto-compound process, or indirect costs from the gas fees required to execute all those automatic reinvestment transactions.

The strategic decision depends on your position size and the specific fee structures. For small positions where manual harvesting would cost ten to twenty dollars in gas fees each time, auto-compounding protocols charging a one to two percent fee are usually economical because they save you far more in gas than they charge in fees. For large positions where gas fees are negligible relative to position size, manual claiming might be cheaper if you're disciplined about harvesting and reinvesting frequently enough to capture most compound benefits.

Definitely not. In fact, an absurdly high APY should be treated like a flashing red light—a signal to dig deeper, not ape in blindly. It's usually a sign that you’re being compensated for taking on a massive amount of risk.

An extremely high APY can be a red flag for issues like unsustainable token inflation, a new and unaudited protocol, or risky underlying assets. The highest numbers often come from projects where the risk of losing your entire principal is also the greatest.

Always weigh the shiny APY against the real risks we covered earlier. Grinding out a sustainable 5-15% APY from a battle-tested protocol is often a much smarter play than chasing a speculative 1,000% APY on a project that launched yesterday.

This varies all over the place; there's no single standard. What you'll find, though, is that it's almost always much faster than in traditional finance. Forget annual compounding. In crypto, it's common to see rates that compound daily, hourly, or even per block—which can mean every few seconds on some chains. The more frequent the compounding, the greater the effect on your total yield.

Ready to move from theory to action? Stop guessing and start tracking. With Wallet Finder.ai, you can see where the most successful DeFi traders are putting their capital, identify high-yield opportunities backed by real on-chain data, and mirror winning strategies in real time.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.