Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

February 28, 2026

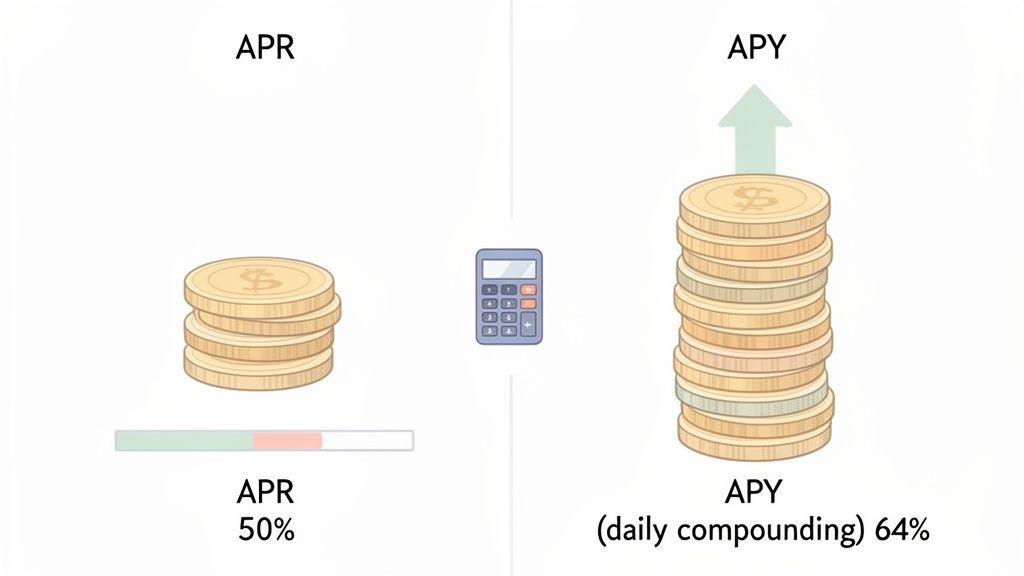

The real difference between APR and APY boils down to one crucial thing: compounding.

APR (Annual Percentage Rate) is the simple, flat interest rate you earn or pay over a year. Think of it as the sticker price. APY (Annual Percentage Yield), on the other hand, is the actual rate you get after factoring in the magic of compounding. For anyone serious about crypto, especially in DeFi, understanding this distinction is non-negotiable for calculating real returns.

When you're navigating the world of decentralized finance (DeFi), you'll see APR and APY everywhere. Getting them mixed up is a rookie mistake that can lead to costly errors and missed gains. While they sound alike, one tells you the advertised rate, and the other reveals your true earning potential.

An APR vs APY calculator is the essential tool that bridges this gap. It translates a simple rate into the effective yield you can actually expect. This is especially vital in crypto, where compounding can happen daily or even multiple times a day, dramatically amplifying your returns.

Let's break these down into simple, actionable terms.

APR (Annual Percentage Rate) represents the yearly interest on your money without any frills. It's a straightforward number that ignores the effect of compounding within that year.

APY (Annual Percentage Yield), however, shows you the total interest you'll earn in a year, including the effects of compounding. Compounding simply means you're earning interest not just on your initial principal, but also on the interest that has already piled up.

Key Takeaway: APY shows the true growth of your investment. Because it accounts for interest earning its own interest, APY will always be equal to or higher than the APR.

This is where the real gains are made. A 50% APR might not seem that different from a 60% APY at first, but the compounded growth over time can be massive. For a deeper dive, you can learn more about what APY in crypto means and how it’s calculated.

This table helps you understand the fundamental differences between Annual Percentage Rate and Annual Percentage Yield at a glance, so you know which metric to focus on.

For active DeFi traders using platforms like Wallet Finder.ai, internalizing this table is non-negotiable. It gives you the clarity to accurately compare yield farming opportunities and analyze the true PnL of top wallets you might be tracking.

To make money in crypto, you first have to understand the math behind it. Accurately forecasting your profits and making sense of the returns advertised on DeFi platforms comes down to knowing the difference between APR and APY. These two formulas are what turn those abstract percentages into real-world return projections.

While APR is just a simple interest rate, APY accounts for the powerful effect of compounding. Grasping this distinction is the secret to seeing the true growth potential of your crypto assets. Let's break down the formulas you need to know.

Calculating the Annual Percentage Rate (APR) is straightforward. Because it doesn’t factor in compounding, it’s simply the periodic interest rate multiplied by the number of periods in a year.

Formula: APR = Periodic Rate × Number of Periods in a Year

Let’s say you find a DeFi protocol offering a 0.1% daily interest rate. To find the APR, you’d multiply that daily rate by the number of days in a year.

0.1% (daily rate) × 365 days = 36.5% APRThis number shows your simple annual return if you don't reinvest your earnings. But since most DeFi protocols let you compound, that brings us to the metric that really matters for investors: APY.

The Annual Percentage Yield (APY) shows you the actual return you can expect on an investment by including compound interest. The APY formula is your go-to tool, essentially acting as an apr vs apy calculator to reveal how your earnings can really pick up speed over time.

Formula: APY = (1 + r/n)^n - 1

Let's unpack what each part of this critical equation means:

The magic of this formula is all in the 'n'. The more often your crypto compounds—whether it's daily, hourly, or even more frequently—the higher your APY will be compared to the base APR.

Key Insight: The APY formula proves that how often you compound is just as important as how much interest you earn. Frequent compounding is what drives that exponential growth you see in DeFi.

Let's run the numbers with a real-world crypto scenario. Imagine a new staking pool on Solana is advertising a 30% APR with daily compounding. What's the actual yield?

Now, we just pop these values into the formula:

0.30 / 365 = 0.00082191 + 0.0008219 = 1.00082191.0008219 ^ 365 = 1.34981.3498 - 1 = 0.3498, which gives you 34.98% APY.See that? The advertised 30% APR actually becomes a much more attractive 35% APY just from compounding daily. This isn't just a math exercise; it's a fundamental skill for forecasting profits and is exactly how smart traders on platforms like Wallet Finder.ai vet new opportunities.

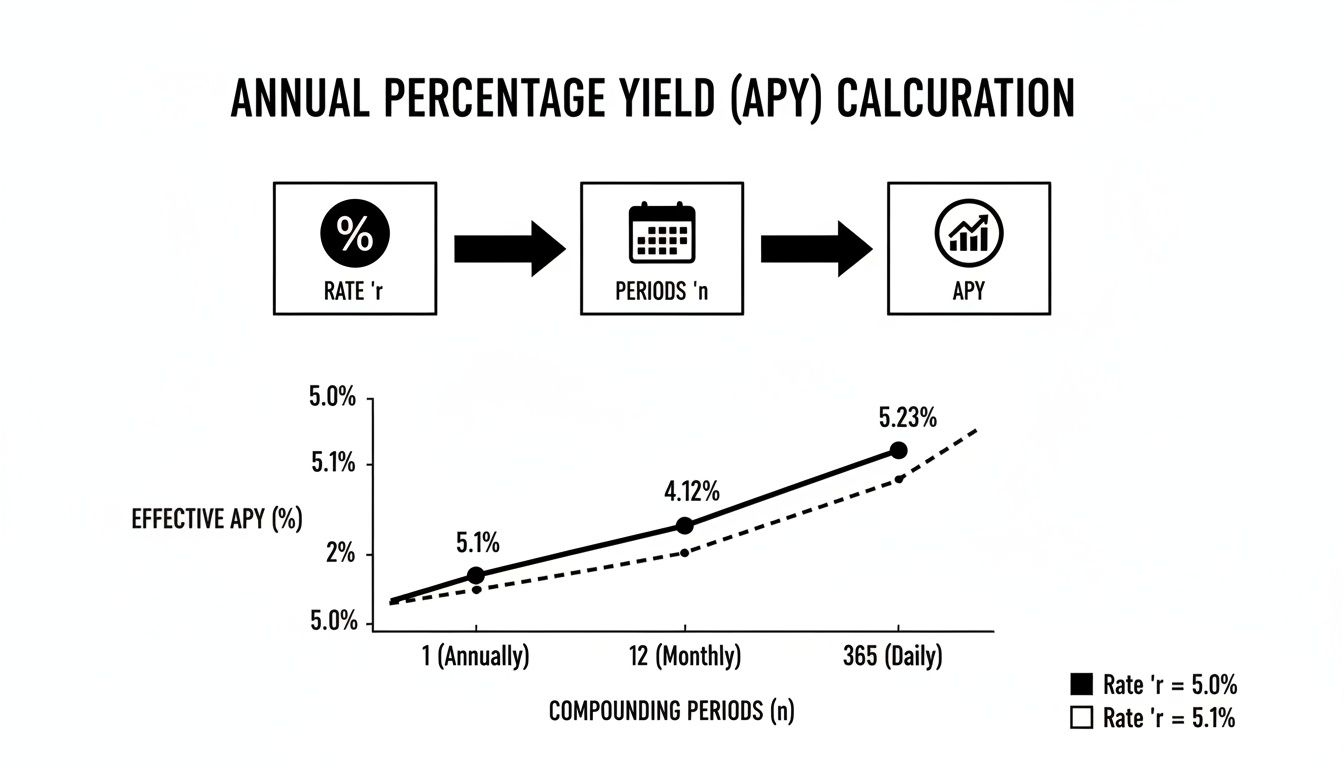

The secret ingredient separating modest returns from massive ones is compounding frequency. This concept—how often your interest earns interest—is the powerful "n" variable in the APY formula. Its impact on your portfolio can be dramatic, turning a simple APR into a much more significant real-world return.

Getting a grip on this isn't just theory; it's a core skill for any serious investor. The more frequently an investment compounds, the faster your principal grows. It’s a snowball effect that accelerates your gains over time, which is exactly why APY is the more critical metric for evaluating earning opportunities.

This simple visualization breaks down how the interest rate (r) and the number of compounding periods (n) work together to calculate your final APY.

As you can see, APY isn't a static number. It’s the dynamic result of both the base rate and how often it’s compounded, highlighting why more frequent periods always lead to higher effective yields.

Let's make this tangible. Imagine a fixed 10% APR. By itself, this number tells you very little about your actual earnings. The real story unfolds when we apply different compounding frequencies, and the difference between compounding once a year versus 365 times a year is substantial.

To illustrate, think about traditional finance. You're eyeing a high-yield savings account or a CD, and the bank quotes you a 5% APR. If it's compounded monthly, a quick run through an APR vs APY calculator shows it jumps to about 5.12% APY. This difference became especially stark during the rate spikes of 2022-2023 when competitive one-year CD APYs peaked. You can dig into more of these historical CD rate fluctuations on Bankrate.com.

The table below shows exactly how a 10% APR blossoms into different APYs as compounding becomes more frequent.

This table shows how Annual Percentage Yield (APY) increases as the number of compounding periods grows, even when the APR remains fixed at 10%.

As you can see, even with the same 10% APR, daily compounding yields a noticeably higher return than annual compounding. While a 0.52% difference might seem small, it adds up significantly on larger sums or over longer timeframes.

In DeFi, this effect is amplified. Unlike traditional banking where monthly compounding is common, many crypto protocols compound daily, hourly, or even per block. This aggressive schedule is a primary driver of the high yields you see in yield farming and staking.

For traders using tools like Wallet Finder.ai, understanding compounding frequency is critical for two key reasons:

Key Insight: When you analyze a top wallet's PnL on Wallet Finder.ai, don't just look at the final return. Dig deeper to see if the gains come from a sustainable high APR or from an aggressive, potentially riskier, compounding schedule.

This distinction is vital. A strategy based on a solid base rate is often more sustainable than one that relies purely on hyper-compounding, which can be subject to protocol changes or market volatility. By using an APR vs APY calculator to normalize returns, you can make more informed decisions about which strategies are worth replicating and which carry hidden risks.

Ultimately, mastering this concept helps you see beyond the advertised rates to understand the true mechanics of wealth generation in DeFi.

Turning financial theory into actual profit starts with getting your hands dirty. An APR vs APY calculator is a non-negotiable tool for any DeFi investor, but truly understanding what goes on behind the scenes is what solidifies your knowledge. Let's walk through a real-world scenario to see how to translate an advertised rate into the yield you'll actually pocket.

Imagine you've stumbled upon a new liquidity pool on an up-and-coming blockchain. It's flashing a very attractive 60% APR, and the protocol's docs confirm that rewards compound daily. To properly size this up against other opportunities, you need to find its APY.

Before you jump to an online tool, let's crunch the numbers by hand using the formula we covered: APY = (1 + r/n)^n - 1. Going through this process helps you internalize just how much compounding frequency can juice a simple rate into a powerful yield.

Here are the variables for our situation:

Now, let's plug these into the formula, step-by-step.

Define Your Variables:

Calculate the Periodic Rate:

0.60 / 365 = 0.0016438Add 1 and Compound:

1 + 0.0016438 = 1.0016438.(1.0016438) ^ 365 = 1.8219.Finalize the APY:

1.8219 - 1 = 0.8219.The final APY comes out to 82.19%. That means the advertised 60% APR is actually delivering a much higher real-world return, all thanks to the magic of daily compounding.

While doing the math yourself is a great learning exercise, speed and accuracy are everything in the fast-paced world of DeFi. This is where an online or embedded APR vs APY calculator becomes your best friend.

Let's use the same scenario to see just how much faster it is.

Input for the Calculator:

The calculator instantly runs the exact same calculation we just did manually, spitting out the immediate result: 82.19% APY.

Pro Tip: Bookmark a reliable APR to APY calculator. When you're digging into new DeFi projects or tracking wallets on a platform like Wallet Finder.ai, you can instantly convert any advertised APR into its true APY. This lets you make quick, accurate comparisons between different yield opportunities on the fly.

Mastering this simple two-step process—finding the APR and compounding frequency, then plugging them into a calculator—is a fundamental skill. It lets you vet opportunities in seconds, cut through the marketing hype, and focus on the numbers that actually grow your portfolio. For users of Wallet Finder.ai, this means you can instantly translate any advertised rate into the real-world yield you can expect, making your profit projections and trading decisions that much sharper.

Knowing the math behind APR and APY is one thing. Actually using that knowledge to turn a profit is a whole different ball game. This is where your understanding becomes a real edge in decentralized finance. With the right approach, you can vet opportunities more effectively, analyze top traders, and make smarter decisions to protect and grow your capital.

The core principle is simple but incredibly powerful: always use the right metric for the job. APY reveals your true earning potential, while APR shows the real cost of borrowing. Getting this right is the first step toward building a profitable on-chain strategy.

Heads up: not all high yields are created equal. The first step in effective yield farming is to look past the flashy headline APR and zero in on protocols that offer both transparency and frequent compounding. A protocol's willingness to clearly state its compounding schedule is often a good sign.

When you're sizing up a new farm or staking pool, ask these critical questions:

By prioritizing pools with transparent, frequent, and automatic compounding, you're setting yourself up for much more predictable and passive returns.

One of the smartest ways to find an edge is to study what profitable traders are actually doing. Tools like Wallet Finder.ai let you track the PnL of top wallets, but just glancing at the surface can be misleading. A sharp analyst uses their knowledge of APR and APY to dig deeper.

When you spot a wallet with impressive gains, don't just see the profit. Ask how they got there.

A key takeaway for every investor: 'When you invest, compare APY. When you borrow, compare APR.' This simple rule ensures you are always evaluating opportunities and obligations from the correct financial perspective, maximizing gains and minimizing costs.

This volatility highlights the danger of focusing only on APR—for instance, a standard 4% APR compounded quarterly becomes 4.06% APY, but if compounded annually, it stays at just 4%, costing long-term holders. In DeFi, where Wallet Finder.ai tracks Solana memecoin flips with 100%+ APRs, daily compounding on certain protocols can inflate that into a 150%+ APY, amplifying the win streaks for top wallets. This is a stark contrast to traditional markets, where historical stock data shows the S&P 500 returning 11.62% annualized over 50 years, and yet many investors miss out by sticking to "safe" assets. You can see how these rates have evolved by checking out historical CD rates on NerdWallet.com.

Let's say you're looking at two promising yield farming opportunities. They both advertise a similar APR, but they're on different blockchains and involve completely different assets. How do you decide?

Here’s a simple framework to guide your decision. Let's compare two hypothetical farms:

At first glance, the 120% APR looks like a no-brainer. But a smart investor always analyzes the risk-adjusted return.

For an investor who wants to preserve their capital, the stablecoin farm's 35% APY is the clear winner, even with its lower headline number. For a degen chasing high-risk, high-reward plays, the memecoin might be tempting, but they have to accept the massive underlying risk. You can sharpen your ability to make these calls by exploring our detailed guide on staking in DeFi and its associated risks.

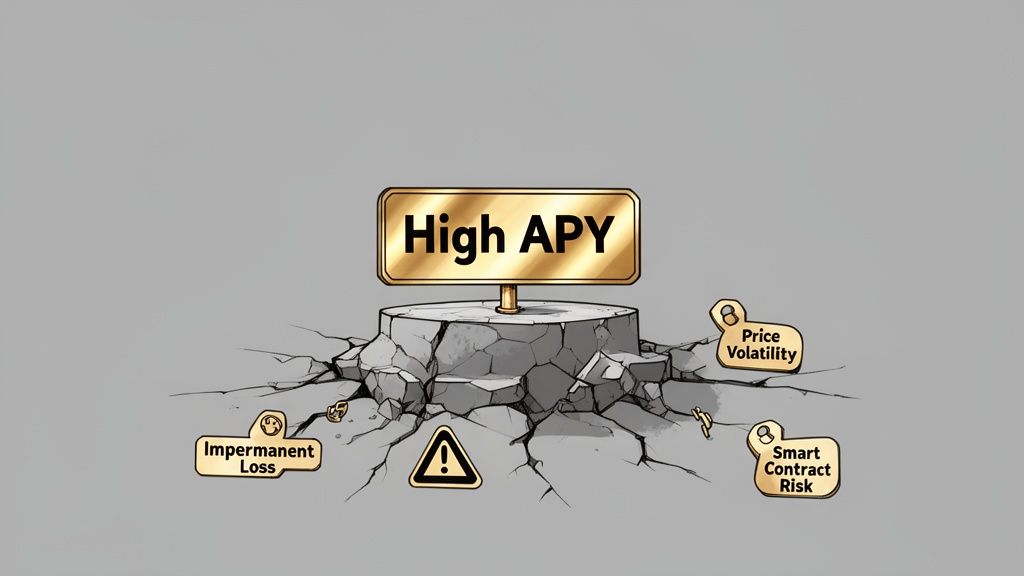

A massive APY can be a siren's call for crypto investors, but it often hides serious risks. Knowing how to use an apr vs apy calculator is a great start, but spotting the traps that can wipe out your gains is how you protect your capital.

Let's dig into the hidden dangers that can turn a promising yield farm into a financial black hole. Moving beyond just chasing the highest number to finding the highest risk-adjusted and sustainable yield is what separates novice investors from seasoned pros.

A jaw-dropping APY is the oldest marketing trick in the DeFi playbook. While it looks great on the surface, that number can be incredibly misleading if you don't understand the mechanics and risks involved. What you see is almost never what you get.

The most common trap is the disconnect between the advertised APY and the actual return you'll see. Most APY figures are calculated assuming the token's price stays perfectly stable. In the wild west of crypto, that's a fantasy, leading to massive gaps between expected and real returns.

Impermanent loss (IL) is easily one of the most misunderstood—and dangerous—risks in DeFi, especially for liquidity providers. It’s the loss you face when the value of your tokens in a liquidity pool drops compared to what they'd be worth if you just held them in your wallet. Even a crazy-high APY can get completely wiped out by IL if the token prices diverge.

Keep these points about impermanent loss in mind:

A sky-high APY means nothing if impermanent loss erodes your principal. Before jumping into any liquidity pool, you must weigh the expected yield against the potential for IL. To get a better handle on this, check out our guide where you can learn more about an impermanent loss calculator and how to assess your risk.

Even if you nail the token price predictions and impermanent loss is a non-issue, you’re still exposed to tech risks. The protocol with the highest yield could be a ticking time bomb if its smart contracts aren't locked down. A single bug can mean a total loss of your funds.

Before you deposit a single dollar, always vet the protocol’s security:

Even when you feel like you have a handle on the basics, applying APR and APY concepts out in the wild always brings up new questions. Let's tackle some of the most common ones I hear, so you can navigate DeFi yields with more confidence.

Nope, APY can never be lower than APR. Think of it this way: at the absolute minimum, APY will match the APR. This only happens if your interest is compounded just once per year.

The second compounding kicks in more often—whether it's monthly, weekly, or even daily—the APY will always climb higher than the APR. That’s because APY is designed to include the extra earnings you get from your previously paid interest, a detail the simpler APR metric completely overlooks. The more frequently it compounds, the bigger that difference gets.

You’ll definitely run into protocols that only list an APR, and it’s usually for a couple of strategic reasons.

Key Insight: When you only see an APR, take it as your cue to do some quick math. Your first move should be to plug the numbers into an apr vs apy calculator to see what you could actually earn based on the compounding schedule.

Finding out how often a protocol compounds your earnings is a critical piece of due diligence before you put any capital in.

There’s no magic number here—a "good" APY is completely relative and depends on the asset's risk profile.

Here’s a rough guide to put things in perspective:

Always weigh the shiny APY against the asset's volatility and the security of the protocol it's on.

Ready to stop guessing and start analyzing? Wallet Finder.ai helps you discover profitable wallets and mirror winning DeFi strategies in real time. Find your edge and act ahead of the market by tracking smart money movements. Start your 7-day free trial at Wallet Finder.ai.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.