Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

June 20, 2026

Your wallet probably looks diversified on the surface. You hold an L1, a few DeFi governance tokens, a memecoin basket, an LP position, maybe an RWA token for “balance.” Then risk comes off across crypto and nearly everything drops together.

That's the problem. In DeFi, owning more tickers often just means you've spread the same risk across more wrappers.

A useful diversification tool isn't a magic dashboard that says “safe” or “unsafe.” It's a way to inspect correlation, concentration, protocol risk, and liquidity before the market forces you to learn what your portfolio really is.

A lot of traders build what looks like a broad book, then discover they were long one trade the whole time.

You can hold ETH, three ETH-beta governance tokens, two Solana memecoins, an L2 token, and a yield position that ultimately depends on the same risk-on flow. On paper, that's many positions. In practice, it's one regime bet with extra tabs open.

That's why “more coins” is a weak portfolio rule. It ignores what matters when the tape turns. A memecoin, a farm token, and an L2 governance token can all behave like amplified versions of the same market sentiment.

Recent institutional commentary argues for moving beyond simple stock and bond mixes to include alternatives. That same piece says such portfolios have shown the potential to achieve Sharpe ratios close to 1.0 and improve drawdowns over 20+ years, while focusing more on inflation hedges, tail-risk control, and total-portfolio design (Interactive Brokers on defensive alternatives). The lesson maps well to DeFi. If you want resilience, you need exposures that fail differently, not just more exposures.

A trader thinks they've diversified because they split capital across:

Practical rule: If several positions depend on the same liquidity conditions, the same user base, or the same chain health, treat them as related risk.

If you trade LPs, this matters even more. A lot of “hedged” LP books still hide directional exposure and correlation risk. That's where a deeper review helps, especially if you've been thinking about how diversification can reduce impermanent loss risks.

A real diversification tool starts with one blunt question: what survives when your main thesis is wrong?

Real DeFi diversification is about how positions behave relative to each other, not how many line items sit in your wallet.

The cleanest way to think about it is a basketball roster. Five centers don't make a complete team. They just give you five versions of the same strength and the same weakness. A DeFi portfolio built from assets that all rely on the same market mood has the same flaw.

The core benefit of diversification is reducing unsystematic risk by combining assets that move differently. But that benefit weakens when correlations rise during stress, which means the key test isn't asset count. It's how your positions co-move when everything sells off together (Saxo on diversification and correlation under stress).

You can own:

That isn't broad exposure. It's clustered exposure.

A smarter question is: what role does each position play?

A practical DeFi book often has different jobs assigned to different positions:

That framework forces discipline. Instead of asking whether a token is interesting, you ask whether it adds a new behavior to the portfolio.

Diversification only counts if the assets diversify when conditions get ugly, not when the timeline is euphoric.

Your article's central argument — that most portfolios that look diversified are actually one correlated bet with extra wrappers — is correct and well-made. What it does not give readers is the navigable map of which genuine diversification categories exist in 2026 and how each one behaves differently from the others. Without that map, the argument that you need true diversification is compelling but not actionable.

The 2026 crypto market has matured into six meaningfully distinct categories that experienced portfolio builders treat as separate exposure types rather than interchangeable lines on a holdings list.

The first is large-cap infrastructure — Bitcoin and Ethereum specifically. These behave differently from each other in certain regimes but share the property of being the primary destination for institutional capital, ETF flows, and risk-on rotation into crypto. They are the most liquid, the most regulated, and the most likely to be treated as macro assets rather than sector plays. They are the foundation of most portfolios precisely because their behavior in stress conditions is more predictable than anything else in the space.

The second category is Layer 1 and Layer 2 protocols — Solana, Avalanche, Arbitrum, Base, Optimism. These tokens represent infrastructure bets on which execution environments will attract developer activity and user volume. Their behavior is closely related to broad crypto sentiment but with additional idiosyncratic risk tied to ecosystem health. Solana and Ethereum L2s have diverged significantly in correlation from each other as the ecosystem competition has developed, which means owning both is not the same as owning the same bet twice — but owning three Ethereum L2 governance tokens often is.

The third category is DeFi protocol tokens — Uniswap, Aave, Compound, Curve. These are claims on specific protocol revenues and governance rights. Their price behavior combines general crypto sentiment with protocol-specific performance, making them meaningfully different from their underlying chain tokens. Aave on Ethereum is not the same directional bet as ETH itself, even though they share some correlation during risk-off events.

Real-world assets represent the fourth category and the most institutionally distinctive one in 2026. Tokenized treasury products, private credit, and real estate exposure through blockchain infrastructure have been the fastest-growing sector by TVL in 2026, with the market reaching $29.2 billion by April. RWA tokens and the protocols that support them tend to have lower correlation to speculative crypto sentiment because their underlying assets are traditional financial instruments. When crypto broadly sells off, RWA-backed yield products are less likely to collapse proportionally.

AI and decentralized compute tokens form the fifth category — assets tied to machine learning infrastructure, decentralized data markets, and AI agent networks. These are correlated to crypto sentiment in bull markets but have an additional narrative driver in the form of the broader AI investment cycle, which occasionally causes them to diverge from crypto's direction when AI news is the dominant market theme.

Stablecoins are the sixth and most practically important category for portfolio construction — not as a return vehicle but as the liquidity buffer that makes everything else manageable. Maintaining 5-10% in stablecoins gives you the capacity to rebalance into weakness, cover gas fees during volatile markets, and avoid forced selling in a position you want to hold when a better opportunity requires capital. Nexo's 2026 portfolio guide and the Zipmex allocation framework both treat stablecoin allocation as a structural portfolio decision rather than an afterthought.

The sector map matters for diversification precisely because owning one asset from each of the first four meaningful categories — a large-cap anchor, an L1/L2 infrastructure bet, a DeFi protocol, and an RWA exposure — gives you genuinely different sources of risk and return than owning six tokens that all move on the same crowd attention signal. The framework your article uses to evaluate correlation behavior across market regimes is most powerful when applied to assets drawn from these distinct categories rather than to assets drawn from the same one. The trend identification guide covers how to track which sectors are attracting capital before prices reflect the rotation.

A useful DeFi diversification tool helps you inspect several layers at once:

If you want a practical framework for deciding those buckets, this allocation strategy guide is a useful companion.

The short version is simple. A diversified DeFi portfolio doesn't own everything. It owns a small set of exposures that react differently for clear reasons.

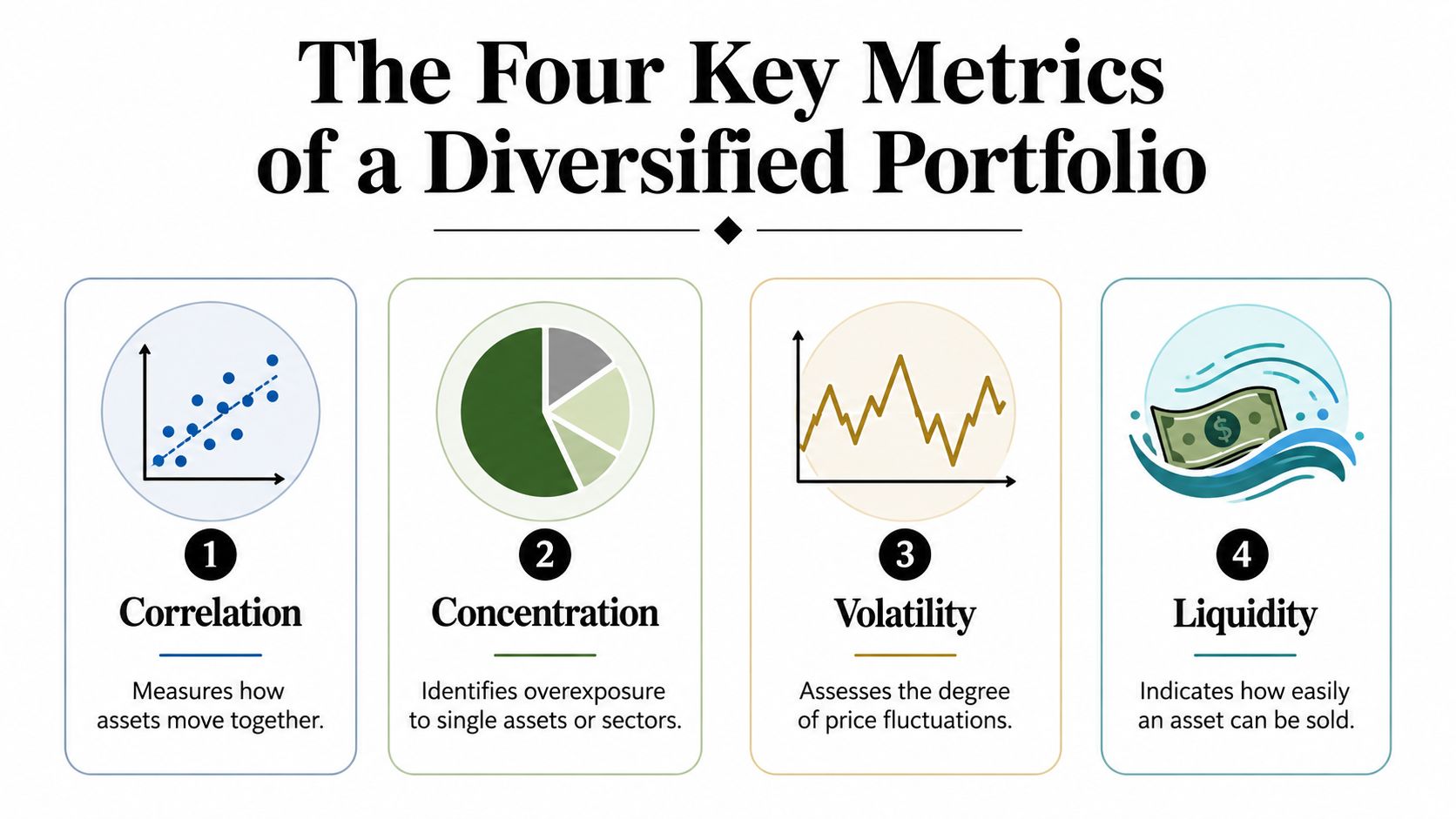

If you want to evaluate a portfolio like a practitioner, track four things: correlation, concentration, exposure, and rebalancing cadence. Without those, “diversified” is just a vibe.

Correlation asks whether assets move differently.

In DeFi terms, ETH, a fresh Solana memecoin, and an RWA token may look unrelated. Sometimes they are. But if all three mainly respond to broad crypto risk appetite, then the diversification benefit is weaker than it appears.

What works is comparing behavior across market regimes, not just calm periods. If two assets look independent only when everything is green, that's weak diversification.

Use this checklist:

Concentration is the fastest way to blow up a “diversified” book.

Most traders check single-token concentration and stop there. That misses the bigger issue. You can be diversified by ticker and highly concentrated by narrative, chain, or protocol family.

Common hidden concentration points include:

Hidden risk: When one narrative drives most of your unrealized gains, your portfolio is usually less diversified than your token list suggests.

Exposure is broader than position size. It includes what can hurt you indirectly.

For example, an LP might look neutral at first glance, but your real exposure can include directional token risk, impermanent loss, smart contract risk, bridge risk, and exit liquidity risk. A restaking or yield strategy may add counterparty and protocol dependency that doesn't show up in a simple wallet balance view.

A practical way to audit exposure is to map each position to these buckets:

Rebalancing is where good portfolio construction usually breaks down. Traders either never rebalance, or they touch the book every time the feed gets noisy.

A useful cadence is event-driven, not compulsive. Rebalance when the portfolio drifts from its intended role mix, when one narrative becomes too dominant, or when a position's risk profile changes.

Good practice usually looks like this:

A good diversification tool helps you see those four metrics quickly. It doesn't replace judgment. It sharpens it.

Most traders don't need one tool. They need a small stack where each tool does a specific job well.

Some tools show balances cleanly but miss wallet behavior. Others are strong at wallet discovery but weak at allocation review. Some automate portfolio maintenance but don't help you judge whether the underlying exposures are distinct.

Here's a practical comparison:

Portfolio analytics platforms work well for snapshot analysis. They're useful when you want to know whether your wallet is too heavy in one chain or one token family. They're less useful when you need to understand how a position was built and whether the wallet owner has process.

On-chain wallet trackers help with behavioral diversification. That matters if you copy trade or source ideas from smart money. A wallet that trades only one narrative isn't the same as a wallet that rotates cleanly across unrelated setups. For that use case, this overview of DeFi portfolio tracker options is a practical starting point.

Automated rebalancers are powerful if your rules are already good. They are dangerous if your rules are lazy. Automation can preserve discipline, but it can also industrialize bad portfolio design.

Multi-chain dashboards solve a different problem. They reduce operational blindness. If your exposure lives across several chains, you need one place to verify where risk is sitting.

A tool stack is only useful if each part answers a different question. Don't buy five dashboards that all show the same wallet balance.

Wallet-level analysis sits in a different category from standard portfolio tracking.

It's not just about what a wallet owns today. It's about:

That's where a diversification tool becomes an edge, not just an organizer. You stop looking only at your own positions and start studying how strong wallets distribute risk across markets.

If you use wallet tracking as a diversification tool, the goal isn't to copy every profitable address you find. It's to understand what kind of risk each wallet is taking, then build a watchlist with complementary strengths.

Start with the wallet discovery layer.

Use Discover Wallets to search for traders by behavior, not just headline returns.

A practical screen looks for wallets that appear strong in different ways:

That gives you a research basket, not a hero wallet.

The mistake is chasing the top PnL line without context. A wallet can look elite because one outsized trade dominates the history. That's not diversified skill. That's concentrated luck until proven otherwise.

Once you click into a wallet, ignore the temptation to judge it by total value or one recent win. Look at its PnL, trade history, and where gains originated.

Ask these questions:

Don't confuse visible PnL with transferable process. Your edge comes from identifying which wallet behavior can survive outside one hot regime.

Wallet-level analysis proves valuable. You can often tell when an apparently diversified wallet is still fragile.

Watch for patterns like:

A good review often ends with fewer wallets on your list, not more.

Here's a quick product walk-through if you want to see the workflow in action:

The strongest use of Wallet Finder.ai is building a watchlist of complementary wallets instead of mirroring one address wholesale.

That can look like:

Wallet roleWhat you want from itCore allocatorExposure to steadier, larger-cap positioningNarrative scoutEarly reads on new sectorsTactical traderCleaner entry and exit timingEcosystem specialistCoverage in a chain where you lack native feel

That structure matters because you're diversifying your idea flow, not just your token holdings.

Wallet Finder.ai fits the on-chain wallet tracker category. It lets users inspect wallet histories, trades, tokens, and PnL, then build watchlists and alerts across major ecosystems. Used this way, it becomes less of a copy-trading shortcut and more of a research layer for avoiding concentration in both positions and information sources.

Diversification in DeFi works when you treat it like risk engineering. It fails when you treat it like collecting ticker symbols.

The point isn't to remove risk. It's to avoid taking the same risk five different ways without realizing it.

Run this once before you add another position:

If those answers feel uncomfortable, your diversification tool isn't another token. It's better analysis.

Use an event-driven approach, not a fixed habit. Rebalance when a position grows far beyond its intended role, when your portfolio becomes too concentrated in one theme, or when a protocol's risk changes. Small drift usually isn't worth paying to fix.

Sometimes, yes. That's the trade-off. Real diversification usually sacrifices some top-end outcome in exchange for a better chance of staying solvent and adaptable. The practical fix is to isolate high-upside bets in a clearly sized speculative sleeve instead of letting them dominate the whole book.

Spread risk across different protocol designs, chains, and custody assumptions. Avoid stacking too much capital into positions that share the same technical or governance failure points. Price diversification helps, but operational diversification matters just as much in DeFi.

The number matters less than the correlation structure between what you hold. A portfolio of five assets drawn from genuinely different categories — a large-cap anchor, an L1 infrastructure bet, a DeFi protocol, an RWA exposure, and a stablecoin reserve — is better diversified than a portfolio of twenty tokens that all respond to the same crowd attention signal. Most experienced practitioners in 2026 suggest that 8-12 well-researched positions provide enough diversification to reduce concentration risk without becoming impossible to monitor meaningfully. Beyond 15 positions, the research burden per position usually drops below the level required to maintain genuine conviction in each holding — at which point the portfolio begins to resemble index exposure at worse risk-adjusted terms.

Diversification reduces concentration risk by adding assets that behave differently from what you already hold. Over-diversification occurs when additional positions reduce potential returns without meaningfully reducing risk — usually because the new positions are highly correlated with existing ones, or because they are too small to affect portfolio outcomes in either direction. The test for over-diversification is straightforward: if removing a position from the portfolio would not meaningfully change how the portfolio behaves in stress conditions, it is either too small to matter or too correlated to add genuine diversification value. Both conditions suggest the position should be eliminated and the capital concentrated in higher-conviction holdings that are already contributing to genuine diversification.

Yes — and not just as a defensive position waiting to be deployed. Stablecoins serve three active functions in a well-managed crypto portfolio. They provide the liquidity to rebalance into weakness without having to sell other positions at poor prices. They earn yield through DeFi lending protocols that compounds the portfolio's total return over time. And they give you dry powder for new position opportunities without triggering additional taxable events by selling existing holdings. Most structured portfolios in 2026 maintain 5-10% in stablecoins as a permanent allocation rather than a temporary cash position — treating it as the operational layer that makes everything else in the portfolio more manageable.

The test is behavior under stress, not the number of tickers. Pull your portfolio's performance during the three sharpest crypto drawdowns in the last 18 months and check whether your positions moved in the same direction and at similar magnitudes, or whether some held while others fell. If everything dropped proportionally in lockstep, you were effectively holding a single correlated position regardless of how many distinct assets appeared in your wallet. The more rigorous analysis involves checking whether each pair of holdings has a meaningfully different narrative dependency — whether both assets require the same crowd attention or institutional capital flow to generate positive returns. If they do, their correlation will be high in the conditions that matter most, regardless of how uncorrelated they look during calm periods.

The most reliable approach is threshold-based rather than calendar-based: review the portfolio whenever any holding drifts more than 5-10% from its target allocation, and conduct a qualitative regime review whenever a major market event changes the underlying premises of the allocation. Calendar-based quarterly rebalancing is a reasonable baseline for investors who want a simpler rule, but crypto markets can produce 5-10% allocation drifts in a single day, making a quarterly review schedule potentially too slow to catch significant structural imbalances before they compound. The practical constraint is transaction cost — each rebalancing trade incurs gas fees and a potential taxable event, so wider drift tolerances make sense for smaller portfolios where transaction costs represent a meaningful percentage of the rebalancing amount.

If you want to turn diversification from a slogan into a repeatable research process, Wallet Finder.ai is useful for studying wallet behavior, checking where PnL really came from, and building watchlists across different trading styles instead of copying a single concentrated bet.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.