Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

June 8, 2026

Bitcoin's block subsidy is down 93.75% from its original level after the April 20, 2024 halving, falling from 50 BTC at launch to 3.125 BTC today according to Lightspark's block reward overview. Traders who still treat the Bitcoin block reward as background trivia are missing one of the cleanest structural signals in crypto.

The reason is simple. The block reward isn't just a protocol detail. It changes miner cash flow, shifts the mix between fixed issuance and variable fee income, affects when miners are more likely to hold or sell, and shapes how on-chain analysts should read wallet flows around stress, congestion, and cycle transitions.

For DeFi analysts and copy traders, this matters even if you never touch mining stocks or operate hardware. Miners are among the most structurally important natural sellers in Bitcoin. Their behavior creates recurring pressure points that often show up on-chain before they become obvious in price. If you can read reward composition, fee conditions, and miner wallet movements correctly, you're no longer reacting to headlines. You're reading the supply machine directly.

The topic's usefulness becomes apparent. Not “what is a block reward?” but “what does the current reward regime imply for miner behavior, risk, and trade timing?” That's the difference between textbook knowledge and a tradable framework.

Practical rule: When protocol-level issuance is predictable, edge comes from watching how market participants adapt to it, not from rediscovering the schedule itself.

Most Bitcoin explainers stop at the definition. Miners validate blocks, receive newly issued BTC, and the reward halves on a schedule. All true, and not enough for trading.

The edge starts when you treat the Bitcoin block reward as a live economic input. A miner with a lower subsidy has less margin for error. If fees are quiet, treasury management matters more. If fees surge, miners can suddenly earn much more than the base subsidy from the same block. Those shifts influence wallet behavior, pool payouts, exchange deposits, and short-term sell pressure.

For on-chain traders, the useful question isn't whether the reward exists. It's how the current reward structure changes incentives right now. That's especially relevant after the latest halving because the fixed subsidy is smaller, while the fee component can vary sharply with block space demand.

Three practical consequences matter most:

That's why serious analysts track miner behavior alongside price, open interest, and exchange flows. The block reward is one of the few parts of Bitcoin's economy that is fully programmatic. You know the schedule. You know the base issuance. The uncertainty sits in behavior around it, and that's where trades get shaped.

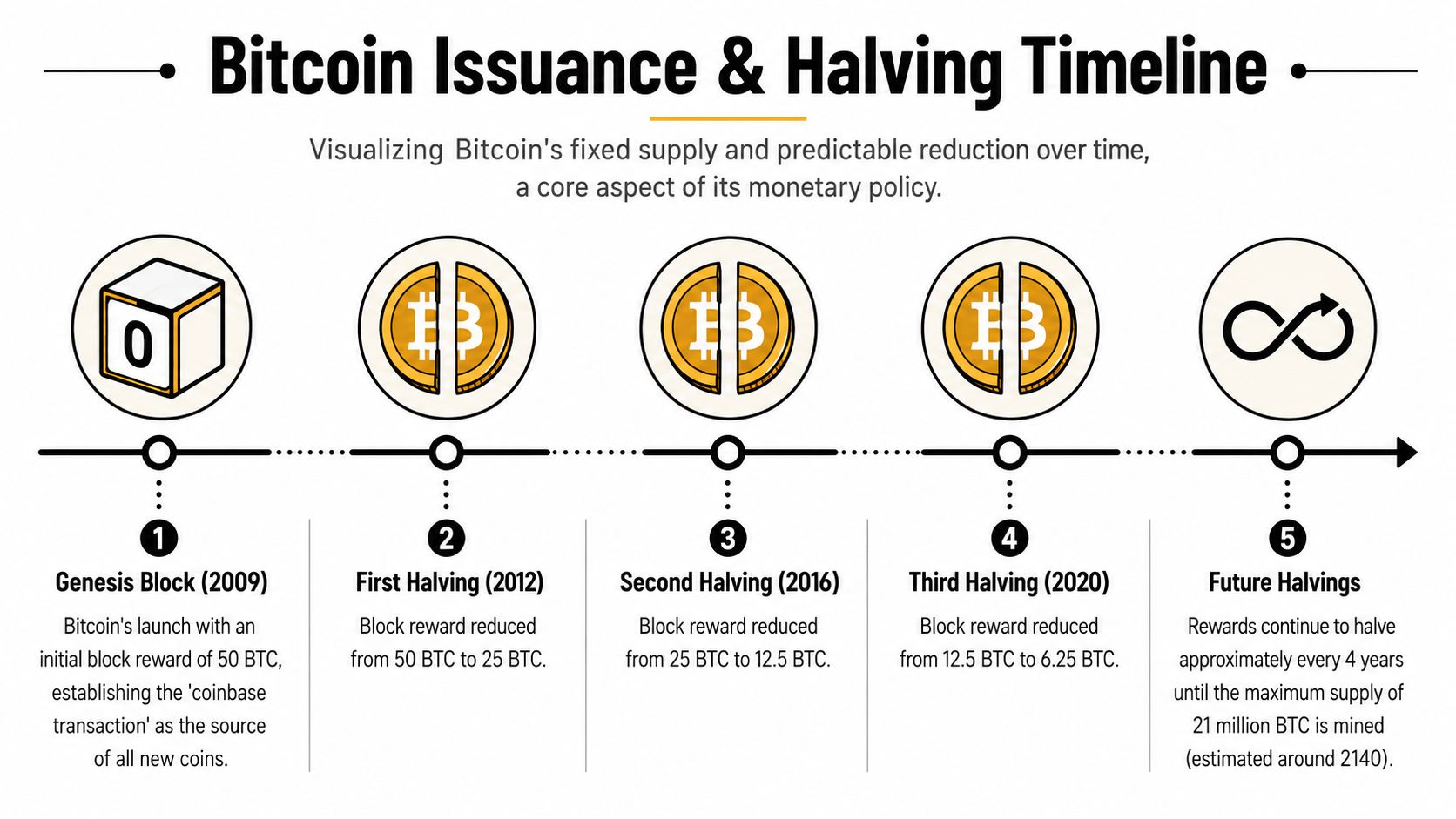

Roughly every 210,000 blocks, Bitcoin cuts new issuance in half. That single rule changes the daily inventory miners can bring to market and gives traders a supply calendar that few other assets offer.

New coins enter circulation through the coinbase transaction, which pays the miner who produces a valid block. The block subsidy started at 50 BTC in 2009 and steps lower on a fixed schedule written into the protocol. For trading, the practical takeaway is simple. Future base issuance is visible well before it arrives, so analysts can model the shift instead of reacting after the fact.

Predictable issuance does not give a clean price forecast. It does give a clean change in sell-side flow. After each halving, miners receive fewer new BTC from subsidy alone, which means the natural source of fresh supply tightens.

That shift matters most when you connect protocol rules to wallet behavior. A miner running on thin margins after a halving has fewer easy choices. Treasury draws, hedging, payout timing, and exchange deposits start carrying more signal. For DeFi analysts and copy traders, that is the useful frame. The halving is a scheduled supply shock, and the edge comes from tracking how miners adjust around it.

Bitcoin also targets an average block time of about 10 minutes, which is what keeps issuance relatively stable over longer periods even as short-term block production varies. That consistency is why halving dates can be estimated closely enough for positioning months in advance.

| Halving Event | Date (Approx.) | Block Height | New Block Reward (BTC) |

|---|---|---|---|

| Network launch | 2009 | N/A | 50 |

| First halving | November 2012 | 210,000 | 25 |

| Second halving | July 2016 | 420,000 | 12.5 |

| Third halving | May 2020 | 630,000 | 6.25 |

| Fourth halving | April 20, 2024 | 740,000 | 3.125 |

A quick visual helps if you want the timeline in another format.

The useful way to trade around halvings is to treat them as supply regime changes and then test whether miner behavior confirms the shift. Price can front-run the event, fade it, or ignore it for stretches. Miner wallet outflows, fee support, and post-halving treasury stress usually offer better confirmation than the calendar alone.

A weak approach is reducing the setup to a one-line rule such as “halving means up.” That misses the variables that shape execution, including operating costs, fee income, derivatives positioning, and liquidity conditions across the market.

The halving is predictable. The trade comes from measuring miner response after the issuance cut.

Post-halving, Bitcoin miners collect 3.125 BTC in subsidy per block, plus whatever the mempool is paying for priority. That second piece now matters more for trade timing than many market participants price in.

The working model is simple. The Bitcoin block reward has two parts: fixed issuance and variable fees. Subsidy changes on the halving schedule. Fees change with user demand, congestion, inscription activity, and how urgently traders want block space. Two blocks can carry the same subsidy and produce very different miner revenue.

According to CoinTracker's block reward explainer, current block rewards combine the 3.125 BTC subsidy with transaction fees, and those fees can vary meaningfully even in the same issuance regime. For trading, that means miner income is no longer a static output of the protocol. It is partly a live read on network activity.

That distinction improves execution. A miner receiving mostly subsidy is operating under a different cash-flow profile than a miner collecting a temporary fee boost during crowded blocks. Both may show wallet movement. The motive behind that movement can be very different.

As the subsidy shrinks over time, fee share becomes more important to miner margins. Analysts tracking miner stress should care less about the textbook formula and more about what mix of revenue miners are earning this week.

I separate miner income into base issuance and activity-driven fees because each one maps to different trade implications:

| Revenue input | What sets it | What traders should watch |

|---|---|---|

| Subsidy | Protocol schedule | Structural supply reduction after halvings |

| Transaction fees | Competition for block space | Congestion, fee spikes, and short-term miner cash-flow relief |

This becomes actionable fast. If BTC price is flat and fees jump, miners can get breathing room without any improvement in spot price. If BTC drifts lower while fees stay weak, treasury pressure can build sooner, especially for operators with higher power costs or thinner balance sheets. Pairing fee strength with a Bitcoin difficulty chart and miner cost pressure context gives a much better read on whether miner transfers reflect distress, routine treasury management, or opportunistic selling into strength.

When I assess miner-related flows, I separate base issuance from activity-driven fees.

That is the part many copy traders miss. “Miner selling” is too broad to trade on its own. The better question is whether miners are selling from pressure, from surplus cash flow, or after a fee-driven windfall that may not last.

A common assumption in Bitcoin commentary is that transaction fees will eventually replace the subsidy and the system will keep working the same way. That's too simple.

The deeper concern isn't just lower revenue. It's more volatile revenue. When block income depends more heavily on fees, rewards can become less stable from block to block. That matters because miners respond to incentives, not slogans.

Academic work from Princeton highlights a more nuanced risk. The concern is whether transaction fees alone can replace the subsidy without creating new attack incentives, and the issue turns on per-block reward thresholds and deviation risk rather than a generic story that “fees take over,” as discussed in Princeton's working paper on Bitcoin without the block reward.

For traders, that isn't just theory. Security assumptions influence long-duration conviction, the pricing of stress events, and how markets react when fee spikes become unusually concentrated.

If rewards become more dependent on sporadic fee bursts, miners may face stronger incentives to behave opportunistically around unusually valuable blocks. You don't need to model every game-theory branch to use the idea. You just need to understand that high-fee conditions aren't only bullish signs of demand. They also change incentive balance inside the network.

That's one reason I prefer reading miner economics alongside network conditions rather than in isolation. If you already monitor adjustment pressure through a Bitcoin difficulty chart for network context, add reward composition to that view. Difficulty tells you one part of miner stress. Reward variance tells you another.

Security budget analysis matters for traders because long-term confidence and short-term incentive distortions can coexist.

What works is thinking in conditional terms. If fees become a larger share of miner revenue, then fee stability matters more. If fee stability weakens, then miner incentives deserve closer scrutiny.

What fails is assuming the future fee market is automatically a clean substitute for the subsidy. The network may remain resilient, but the path is an incentive-design question, not a slogan about scarcity.

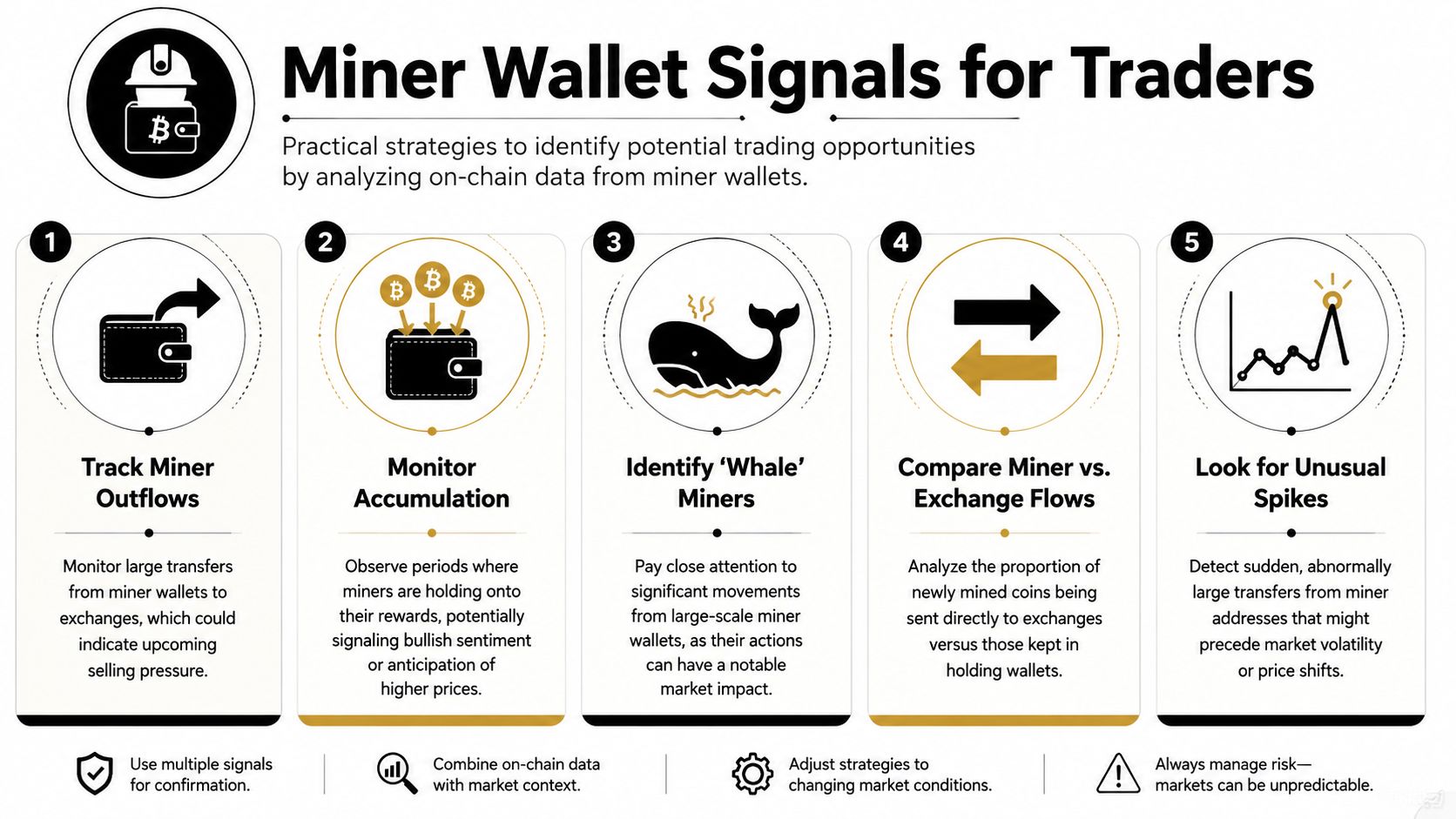

Miner wallets sit at the source of new BTC supply. That makes them one of the few on-chain groups that can shift short-term sell pressure without needing a change in broader investor sentiment.

For traders, the edge comes from tracking changes in miner behavior against the revenue environment they are operating in. A miner sending coins after a strong fee window means something different from a miner sending coins during weak fees and tight margins. The block reward matters here because it sets the cash-flow baseline. Wallet behavior shows how miners respond to that baseline in real time.

After the latest halving, miners had less room for error. The fixed subsidy dropped, fee income stayed uneven, and treasury decisions became easier to spot on-chain. That is why miner wallet analysis works well as a trading input. It helps separate routine movement from balance-sheet stress.

Large miner outflows to exchanges

This is still the cleanest signal. If known miner or pool-linked wallets start routing BTC toward exchange clusters, near-term supply may be coming to market. One transfer is noise. Repeated transfers across several miner entities deserve attention, especially if price is testing support.

Miner holding after reward receipt

Retained balances can matter more than many traders expect. When miners keep newly earned BTC instead of forwarding it quickly, treasury pressure may be easing. In practice, that tends to matter most after a period of weak price action, because reduced forced selling can improve the market's ability to absorb supply.

Divergence between fees and selling behavior

This is one of the better context signals. If fees rise and miner selling also rises, miners may be using a stronger revenue window to convert inventory into cash. If fees rise and coins stay put, miners may have less urgency to sell. The same outflow size can carry a very different read depending on the fee backdrop.

Sudden cluster activity from major pool wallets

Large pool wallets usually move for operational reasons, not impulse. That makes coordinated movement across a wallet cluster more useful than a single isolated transaction. Watch for bursts of transfers, repeated destination patterns, and interactions with known exchange-linked addresses.

Unusual wallet behavior after periods of margin compression

This setup often gives the best signal quality. Extended miner stress can lead to predictable distribution. If that pressure fades and wallet flows normalize while price holds firm, the market may already be absorbing supply that would have weighed on it earlier.

Miner wallet data should be used as a confirmation layer alongside other signals. For practical workflow ideas, combine miner monitoring with broader on-chain wallet flow checks.

A simple decision matrix helps:

| Miner wallet behavior | Fee backdrop | Trading read |

|---|---|---|

| Heavy exchange-bound outflows | Soft fees | Higher risk of pressure |

| Outflows rise | Strong fees | Could be revenue-taking, less bearish by itself |

| Rewards retained | Soft to improving fees | Potentially constructive |

| Erratic large transfers | Mixed | Wait for confirmation from price and exchange flows |

I trust miner-flow signals most when they line up with a market structure problem that already exists. That could be weak spot demand, crowded longs, or a price level that has failed several times. In those conditions, fresh miner distribution can become the marginal seller that matters.

The reverse also applies. Cooling miner outflows during a period of improving risk appetite can support continuation trades, especially when exchange inflows stay contained.

What fails is reading every miner transfer as directional. Pool payouts, wallet reshuffling, custody changes, and internal treasury moves can all create large transactions without changing the underlying supply picture.

The useful signal is behavior relative to miner economics, fee conditions, and market positioning.

Turning miner intelligence into a tradable workflow requires less theory and more operational discipline. The practical job is to identify relevant wallets, track them consistently, and get alerted fast enough to act before the move becomes common knowledge.

That process is where a dedicated tracking platform helps. A dashboard view makes wallet clustering, flow monitoring, and alerting much easier than trying to build the whole stack manually.

Use Wallet Finder.ai as an execution layer for the miner-flow framework above. The goal isn't to watch every Bitcoin address. It's to create a focused watchlist around wallets and entities that have the power to move sentiment or near-term supply.

Identify relevant wallets

Start with known miner-linked, pool-linked, or heavy BTC-moving wallets that fit your strategy. You want addresses with recurring operational significance, not random historical labels.

Build a watchlist by behavior type

Separate wallets into groups. One list for likely treasury wallets. Another for addresses that tend to send onward. Another for entities that matter only when they interact with exchange clusters.

Set real-time alerts

Alerts matter because miner-related signals decay quickly once public dashboards light up. If a tracked entity sends BTC toward a likely exchange path, you want that notification immediately.

The biggest mistake is acting on the first alert as if it were a guaranteed directional call. Instead, use a short checklist.

For copy traders, miner monitoring is useful as a macro supply overlay. It won't replace trade-by-trade wallet mirroring on fast chains, but it can help you size risk and avoid following aggressive longs into obvious distribution windows.

For analysts, the value is in building a repeatable playbook. Track wallets. Label outcomes. Compare miner flows with market reaction. Over time, you'll learn which miner entities are noise and which ones deserve respect.

The Bitcoin block reward starts as a simple concept. Miners receive newly issued BTC plus fees for producing blocks. But for traders, the useful part begins after the definition.

The reward schedule shapes structural issuance. The shrinking subsidy changes miner economics. The growing importance of fees adds variability to revenue. That combination affects how miners manage treasury, when they distribute coins, and how on-chain analysts should interpret wallet movement. Those are not academic details. They're live inputs into market behavior.

The strongest edge comes from reading the block reward indirectly through miner actions. A transfer to an exchange, a period of retention, or a burst of selling during weak fees all say something different. The signal isn't in the wallet move alone. It's in the wallet move relative to the current reward regime.

For DeFi analysts and copy traders, that's the upgrade in perspective. You're not just learning what the Bitcoin block reward is. You're learning how protocol-level issuance flows into observable behavior, and how that behavior can sharpen trade timing, risk management, and market context.

If you can track the supply engine, read miner incentives, and act before the crowd reframes the same data into a narrative, you're already operating with more structure than most market participants.

Wallet Finder.ai helps turn on-chain wallet activity into a usable trading workflow. If you want to track influential wallets, monitor smart money movements in real time, and build alerts around the kinds of flows discussed here, try Wallet Finder.ai.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.