Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

May 15, 2026

You catch a wallet buy, the token starts moving, and the next decision is where most copy traders give back their edge.

Hit market buy too late and you often pay up into momentum. Wait too long and the move is gone. Place a limit order too far below the market and you get the clean price you wanted, but no position. That tension is where the crypto limit order stops being a beginner concept and starts becoming an execution tool.

For traders who act on on-chain signals, this matters more than most guides admit. A signal can be right and still lose money if your fill is bad. A wallet can buy early, absorb slippage, and ride follow-through. You arrive later, submit into thinner liquidity, and end up owning a very different trade.

A familiar setup. You see a respected wallet rotate into a new token. The buy is real, the size is meaningful, and the chart is already lifting. You have two choices.

The first is speed. You slam a market order because you don't want to miss the move. The order fills, but it fills wherever liquidity is available. If the book is thin or the on-chain route is messy, that can mean paying materially more than the wallet you were trying to follow.

The second is discipline. You place a limit order near a level where you'd still like the trade if price retests. If it fills, your entry is cleaner. If it doesn't, you miss the trade entirely.

That isn't an academic difference. It's the practical split between traders who react to alerts and traders who manage execution.

Most copy traders don't fail because they picked the wrong wallet. They fail because they use the wrong order type for the situation.

Practical rule: If your entire edge depends on matching someone else's entry after the move has started, you don't have an analysis edge. You have an execution problem.

A limit order won't solve every one of these problems. It won't create liquidity, and it won't force the market to come back to your price. But it does one important thing. It makes your trade intentional.

That's why serious traders keep coming back to limit orders. Not because they're fancy, but because they force a decision about what price is still worth paying.

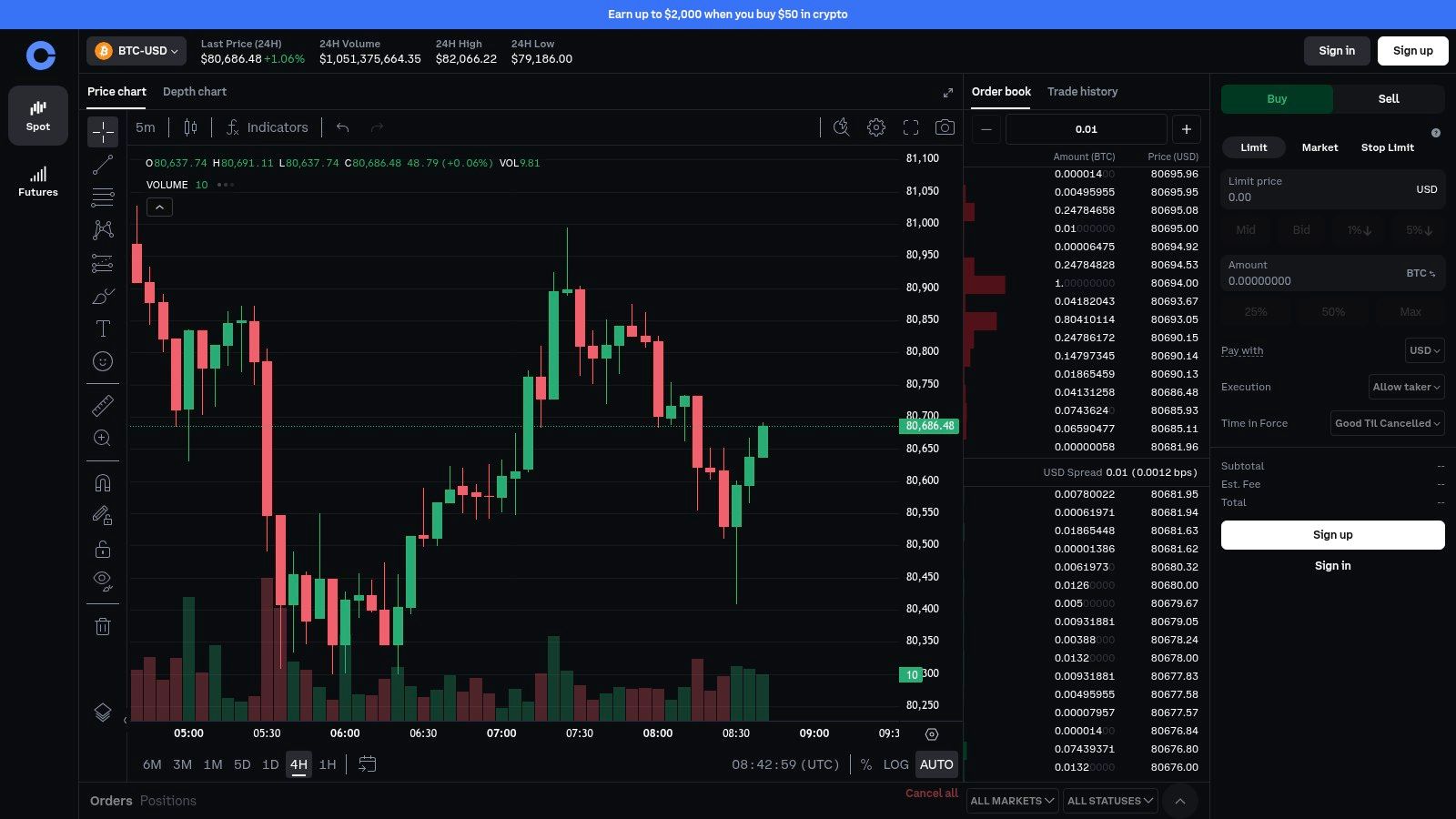

A crypto limit order is a price-controlled trade instruction. You choose the worst price you're willing to accept, then let the market come to you.

For a buy, you set a maximum price. For a sell, you set a minimum price. CoinTracker's explanation of limit orders gives the clearest basic example: if Bitcoin is trading at $29,000 and you place a buy limit order at $28,500, the order only executes if BTC trades at $28,500 or lower. If price never gets there, the order stays unfilled.

That single mechanic is the whole point. A limit order is price first, speed second.

The easiest mental model is an auction bid. You don't tell the auctioneer, "Get me the item right now at any price." You say, "I'm willing to pay up to this amount."

Trading works the same way.

That waiting is a feature, not a flaw. It gives you control over entry quality.

Limit orders are widely used to target support and resistance, reduce slippage, and avoid paying worse prices during volatile moves, as described in this walkthrough of limit buys. In practical terms, they let you say no to bad fills.

They also help form the market itself. Resting limit orders sit in the order book and advertise trading interest at specific prices. That's part of how visible liquidity gets built.

A market order asks, "Can I get in?" A limit order asks, "Can I get in at a price that still makes sense?"

A limit order gives you better price control than a market order, but it does not guarantee execution.

And even when it does fill, it may not fill all at once. Some venues note that limit orders can be partially filled if only part of the requested size is available at your price, with the rest left resting in the book. That's normal market behavior, especially when size is larger than local liquidity.

If you're acting on a wallet signal, that trade-off matters. The cleaner your target price, the greater the chance the market never comes back for you.

A limit order is useful because it solves one problem well. It doesn't solve every problem.

When traders misuse order types, they're usually asking one tool to do a different tool's job. A market order is for immediacy. A limit order is for price control. Stop orders are for reaction once price reaches a trigger.

| Order Type | Primary Goal | Execution Guarantee | Price Guarantee | Ideal Use Case |

|---|---|---|---|---|

| Market | Speed | High immediate execution intent | No | Entering or exiting quickly when getting filled matters more than exact price |

| Limit | Price control | No | Yes, within your stated limit | Buying pullbacks, selling into strength, passive entries around planned levels |

| Stop-Limit | Triggered price control | No after trigger | Conditional | Breakout entries or protective exits where you still want control over the final price |

| Stop-Market | Triggered exit speed | Higher execution intent after trigger | No | Risk management when getting out matters more than precision |

A market order tells the venue to fill your order immediately at the best available prices. That makes it the speed tool.

The problem is simple. If liquidity is thin, the "best available price" may move while your order is being filled. That is exactly why market orders can be expensive in volatile crypto.

Use market orders when the cost of not getting filled is higher than the cost of getting a worse price. That can be true during exits, invalidations, and fast breakouts where a passive bid has little chance of catching up.

Limit orders work best when you already know the price area where the trade still makes sense.

They are strongest in conditions like these:

They are weakest when the market is moving one way and not looking back.

These get confused constantly.

A stop-limit order has two parts. First, price hits your trigger. Then the venue places a limit order. That gives you more control, but it also creates the possibility that the trigger fires and you still don't get filled.

A stop-market is more blunt. Once price hits the trigger, the venue converts it into a market order. You lose price certainty, but you increase the odds of getting out.

If the trade thesis is broken, many traders prefer certainty of exit over elegance of price.

When deciding in real time, use this framework:

For copy trading, the key mistake is using market orders for every alert and limit orders for every retracement. The better approach is to map the order type to the signal condition, not to your emotion in the moment.

The mechanics look similar on the screen. The execution path isn't.

A centralized exchange runs an order book and matching engine. A DeFi interface often depends on smart contracts, routing logic, available liquidity, and whether anyone can fill or execute the order under current conditions.

Here is the familiar centralized layout most traders start with:

On Coinbase Advanced, Binance, Kraken Pro, and similar venues, placing a limit order is operationally straightforward.

The practical edge on a CEX comes from seeing the book. You can inspect nearby bids and asks, decide whether you're joining a crowded price level, and gauge whether your order is likely to sit behind a wall of earlier orders.

If you're automating entries or reacting to alerts through exchange infrastructure, crypto exchange APIs for trading systems matter because they determine how fast you can place, modify, and cancel orders without clicking through the interface.

On-chain limit orders look similar in the UI, but don't assume they behave like exchange-book orders.

A DeFi workflow on tools such as 1inch or Matcha usually looks more like this:

The important difference is underneath. Your result can depend on AMM liquidity, routing, and whether the order gets included and executed under favorable conditions.

First, liquidity isn't always sitting in one obvious book. Your execution may depend on pools, routes, and current reserves.

Second, gas and signing matter. Some systems use off-chain signed messages that are executed later. Others require direct on-chain actions.

Third, the price you target may be reachable in theory but poor in practice if liquidity vanishes or route quality changes before execution.

After you've used the interface a few times, this walkthrough is worth reviewing:

| Venue style | What you control clearly | What can still surprise you |

|---|---|---|

| Centralized exchange | Price, size, visible order placement | Queue delays, partial fills, book changes |

| DeFi limit interface | Target price and broad execution intent | Routing changes, liquidity gaps, on-chain inclusion risk |

For active traders, the main mistake is carrying CEX assumptions into DeFi. The button may say "limit," but the path from intention to fill can be very different.

Placing the order is easy. Living with how it fills is the hard part.

That gap is where many limit-order guides become too clean. In centralized markets, traders mainly worry about whether the order gets hit. In DeFi, the same idea can be affected by routing, liquidity changes, and block-level competition. This policy tracker discussion of crypto-asset transaction interfaces captures the practical issue well: many users assume crypto limit orders work like equity limit orders, but in DeFi the more useful question is whether the order gets front-run, partially filled, or left stranded if liquidity disappears.

A partial fill sounds harmless until you're trading a fast tape.

Suppose you place a buy limit near a retracement zone after a wallet entry. Price tags your level, but only a small portion of your size gets filled before it bounces. You now have the worst version of both outcomes. You didn't get full exposure, and your next fill may happen much higher.

Missed fills create a different problem. Traders often respond by moving the order up repeatedly. That can turn a planned passive entry into an emotional chase.

On-chain execution introduces a different kind of uncertainty. The issue isn't just "did price touch my level?" It's also "what state was liquidity in when the execution path became available?"

That matters because a DeFi limit order may rely on:

A simple version looks like this. You place or sign an order around a visible level. A bot or searcher spots profitable flow around that condition, acts ahead of it, and changes the execution environment before your trade settles.

You may still get a fill. It just may not be the clean one you expected.

On-chain, "limit order" describes your intent. It doesn't guarantee a centralized-order-book style outcome.

That doesn't mean DeFi limit orders are unusable. It means they need different expectations. In many liquid majors, the mechanics are manageable. In thin tokens, fresh launches, and memecoin rotations, the path from signal to fill gets much less reliable.

A few habits improve survival odds:

The best traders don't confuse order type with protection. A limit order protects your stated price boundary. It doesn't protect you from every path the market can take on the way there.

Once you stop treating a limit order as just "buy lower" or "sell higher," more strategic uses open up. Professional traders use variants of the same basic instruction to manage fees, queue position, and information leakage.

The deeper reason this works is structural. Resting limit orders add visible liquidity and help create market depth, and on many venues execution follows price-time priority, where better prices execute first and equal prices are then ranked by arrival time, as outlined in Amberdata's order book primer. That means a limit order isn't just a price preference. It's a place in line.

A post-only order is for traders who want to add liquidity, not accidentally take it.

On many exchanges, a normal limit order can still execute immediately if the market moves into it before it lands. Post-only adds a condition: if the order would remove liquidity on arrival, the venue rejects or cancels it rather than letting it execute as taker flow.

Use it when:

The trade-off is obvious. You preserve maker intent, but you may lose the fill entirely.

An iceberg order shows only part of the total size while hiding the rest.

Large traders use them because displaying full size can distort the local market. If everyone sees a large resting order, they may lean against it, avoid it, or react to it. By showing only a slice, the trader reduces how much information gets broadcast.

For smaller traders, the lesson isn't that you need iceberg functionality every day. It's that visible size changes behavior. If you're placing a larger order in a thinner pair, how much you reveal can affect how others trade around you.

Price-time priority changes how professionals think about passive entries.

Two traders can submit the same buy limit at the same price and get different outcomes because one arrived earlier. That's especially important in crowded levels where many participants are trying to buy the same pullback.

Execution edge often comes from being earlier in the queue, not just smarter about direction.

That insight matters for copy trading. If you're reacting after another wallet already moved the market, your limit order may sit behind a stack of traders who had the same idea faster.

The cleanest use of a crypto limit order is when you're not trying to mimic someone else's exact fill. You're trying to express your own acceptable entry after seeing their signal.

That distinction matters. This discussion of execution quality in fast-moving crypto markets highlights a neglected reality for copy traders: most guides explain placement, not what happens to your edge when the move has already started. For users of tools that surface wallet activity, including Wallet Finder.ai, a wallet's buy can still be a good signal while your limit order becomes a late fill or no fill at all.

Use them when the wallet activity suggests accumulation, not panic momentum.

Good setups include:

Sometimes the passive approach is just wrong.

If a token is moving hard on fresh attention and liquidity is running away, a low passive bid can leave you flat while the market reprices. In that case, a carefully monitored market order or tighter active execution may be safer than pretending patience is discipline.

That doesn't mean "always chase." It means match the order type to the microstructure in front of you.

Before placing a copy-trade entry, ask:

The best copy traders are selective. They don't try to mirror every transaction. They separate wallet discovery from order execution, then use limit orders when price discipline is the decisive advantage.

If you use Wallet Finder.ai to track smart-money wallets across chains, treat its alerts as inputs for your execution plan, not as automatic buy buttons. The platform helps surface wallet entries, timing, sizing, and trade history. Your job is to decide whether the signal calls for a passive limit order, an active entry, or no trade at all.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.