Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

June 11, 2026

You line up a trade, the chart looks clean, the wallet you're watching just bought, and the quoted output seems good enough. Then the transaction lands and you get fewer tokens than expected, or you pay more than the screen showed a moment earlier. That gap is often where a decent trade turns into a mediocre one.

That hidden cost is slippage. In crypto, it shows up everywhere, but it hits hardest where many traders spend their time: fast-moving DEXs, copy trading setups, and low-liquidity memecoin markets. If you're chasing momentum on Solana, buying new launches on Base, or trying to mirror a smart wallet entry on Ethereum, slippage is part of your P&L whether you track it or not.

The practical problem isn't just that slippage exists. It's that many traders treat it like a technical setting instead of a trading cost. That's a mistake. Slippage changes your average entry, your average exit, and your ability to reproduce another trader's performance. A wallet can buy well and still be impossible to copy profitably if your execution is consistently worse.

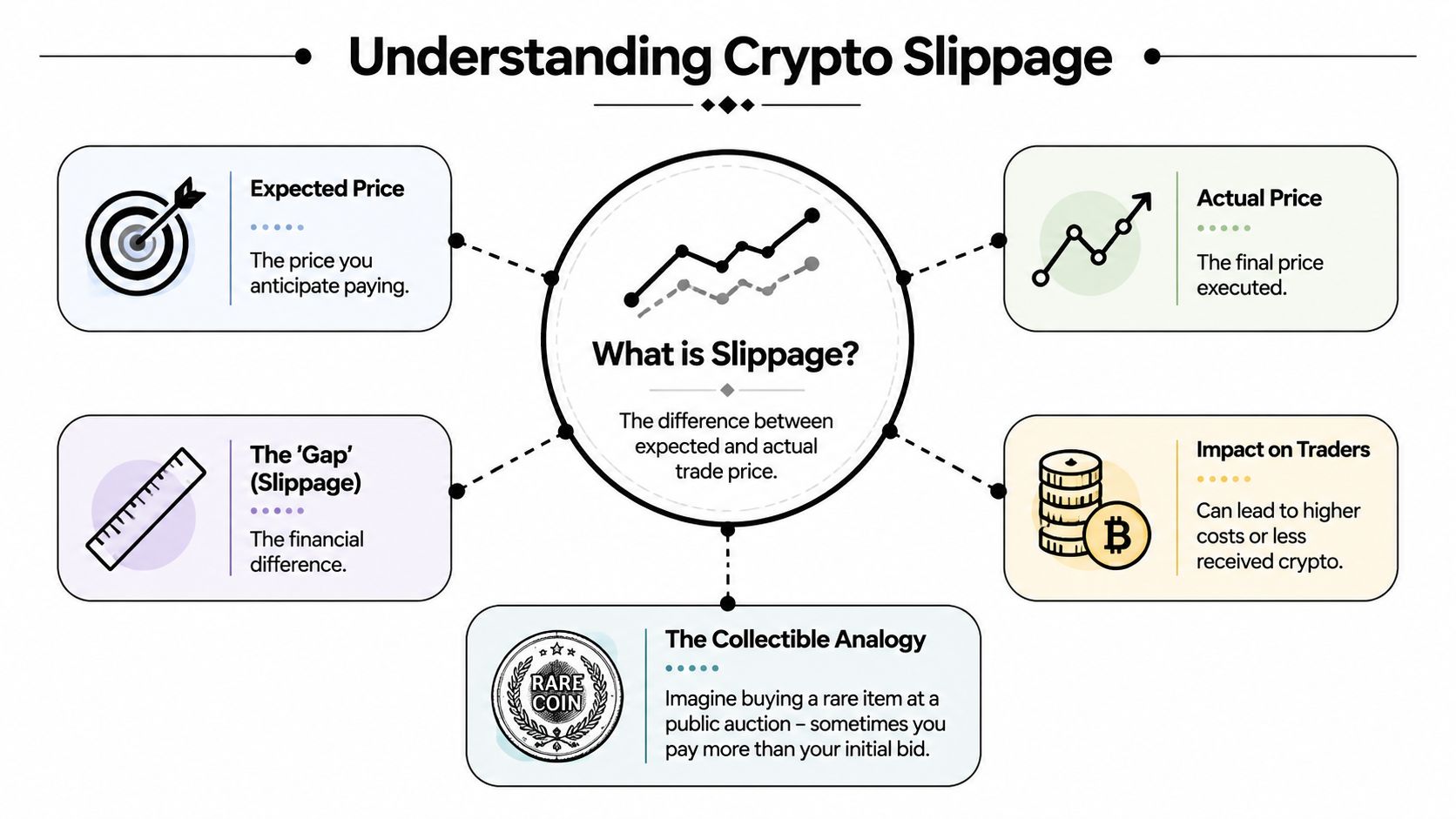

For less experienced traders, the most useful way to think about slippage is simple: it's the difference between the trade you planned and the trade you got. The rest of the details matter, but that framing keeps you focused on what counts. Execution quality.

Your article correctly explains slippage as the gap between expected and executed price caused by volatility, low liquidity, and order size. There is a fourth cause that is not a market condition but a deliberate extraction mechanism — and it accounts for a significant portion of the slippage that DEX traders experience on Ethereum specifically. Understanding it changes how you set slippage tolerance from a passive preference into an active defense decision.

MEV stands for Maximal Extractable Value. It refers to the profit that bots and block producers can capture by reordering transactions within a block before they confirm. The most common and directly harmful version for retail traders is the sandwich attack. The mechanics are precise and repeatable. A bot monitors the public mempool — the queue of pending transactions waiting to be included in a block — for large DEX swaps. When it identifies a swap large enough to move a pool's price, it submits its own buy transaction with a higher gas fee to jump ahead in the queue. The bot's buy executes first, pushing the price up. The original trader's swap then executes at the now-worsened price. The bot immediately sells into the trader's transaction, capturing the price impact as profit. The trader receives fewer tokens than they should have, and the deficit is not random market movement — it is the exact amount the bot extracted.

The detail that connects this directly to slippage tolerance settings is critical: your slippage tolerance is the ceiling on how much a sandwich bot can extract from you and still have your transaction succeed. Arch's April 2026 analysis states this plainly — if you set 3% slippage tolerance, a sophisticated bot can push your execution price to within 2.9% of your expected price and your transaction will still confirm. You have, in effect, pre-authorized up to 3% extraction. A tighter tolerance shrinks the bot's profit window and makes your transaction less attractive to sandwich. A tolerance below what the pool's natural volatility requires will cause your transaction to fail — so the calibration is not zero, but it should be as tight as the market allows rather than as wide as you feel comfortable accepting.

Flashbots Protect on Ethereum routes your transaction directly to block builders without passing through the public mempool, eliminating the window in which bots can see and front-run your order. Jito on Solana provides equivalent protection for Solana-based trades. CoW Swap uses a batch auction model that eliminates the sequential transaction ordering that sandwich attacks depend on. DEX aggregators like 1inch and Paraswap route through private order flow paths when available, reducing but not eliminating MEV exposure depending on the specific path.

The practical rule for managing this is layered. Set slippage as tight as the pool's natural spread allows. For established tokens with real liquidity, 0.5% is a reasonable floor. For volatile or new tokens where 1% to 3% may be necessary to avoid failed transactions, use a private RPC or MEV-protected routing service to reduce the extraction risk that comes with wider tolerance. These two defenses — tight tolerance and private routing — work together rather than as substitutes. The wallet scanner protection guide covers the full threat landscape including honeypot contracts and approval scams that compound the execution risks your slippage settings alone cannot address.

A lot of traders first learn what does slippage mean in crypto after a frustrating swap. You expect one amount, approve the transaction, and receive less. Nothing looks obviously broken. The route worked, the tokens arrived, and the wallet updated. But your trade cost more than you thought.

That's slippage in its most practical form. It's not a fee line item in the same way a platform fee or gas fee is. It's a change in execution. That makes it easier to ignore and harder to manage unless you know exactly what to look for.

For DeFi traders, especially copy traders and memecoin hunters, slippage can impact the economics of an otherwise good idea:

Practical rule: If you don't account for slippage before you trade, you're letting the market choose part of your risk for you.

The fix isn't to avoid DEXs or stop trading volatile assets. It's to understand when slippage is acceptable, when it's a warning sign, and when it completely changes the trade. Good traders don't just find opportunities. They judge whether those opportunities can be executed at a price that leaves room for profit.

Slippage is the gap between the price on your screen and the price you get when the trade executes. For a trader, that gap is part of the trade cost. For a copy trader chasing a wallet entry or a memecoin hunter hitting a fast-moving pool, it can decide whether the setup still has positive expectancy.

Consider buying a rare collectible in a crowded market. You agree on a price, but while you step in to pay, other buyers push demand higher and the seller adjusts. The item is the same. Your timing changed, and so did your fill.

A DEX swap works the same way, except the repricing happens inside the pool and in a matter of seconds. Your quote reflects the pool state when you click swap. Before the transaction confirms, other orders can move the pool, outside markets can reprice the asset, or your own order can be large enough to shift the execution price against you.

If you want to see why the displayed quote often differs from the price you can trade at, this explanation of true market price in crypto trading gives the right framing.

Most of the time, traders mean negative slippage. You expected one outcome and got a worse one. On a buy, you pay more tokens or more dollars than planned. On a sell, you receive less.

Positive slippage also exists. The trade lands at a better price than quoted. It happens, especially in fast markets, but serious traders treat it as a bonus rather than part of the plan. P&L survives on costs you can control, not favorable accidents.

That matters even more if you copy wallets or trade fresh meme rotations. A smart wallet can buy early in a thin pool and still have room. Minutes later, the same entry copied at size can fill far worse. On paper you followed the right wallet. In practice you bought a different trade.

Crypto exposes slippage more clearly than many traditional markets because execution often runs through AMMs, liquidity can be uneven, and small-cap tokens reprice fast. On a deep pair, slippage may stay minor enough to absorb. On a new launch, a low-float memecoin, or a pool with shallow depth, it can wipe out the edge before the trade even starts.

Traders often get hurt by focusing only on direction. A token can still go up after your entry and the trade can underperform because your execution was too poor. I watch slippage as part of entry quality, not as an afterthought.

Tools that surface wallet behavior can help here. If Wallet Finder.ai shows a target wallet repeatedly entering before volume spikes and exiting into crowded follow-on flow, that is a useful signal. The wallet may be profitable. Copying it late may not be. Slippage turns the difference between those two outcomes into a real P&L problem.

Slippage is the gap between spotting an opportunity and capturing it at a price that still makes sense.

The formula is simple:

Slippage (%) = ((Executed Price - Expected Price) / Expected Price) × 100

That formula gives you a clean way to measure how far execution drifted from your quote. The key is to stop treating slippage as vague friction and start measuring it as part of trade cost.

For high-liquidity DEX pairs on Ethereum, slippage is typically 0.1% to 0.5% according to Changelly's guide to slippage in crypto. That's the environment where execution usually feels smooth because there's enough depth for normal-size trades.

A simple example from the verified data: if you expect to buy Bitcoin at $100,000 but the trade fills at $100,100, that's 0.1% slippage.

That kind of difference is annoying, but often manageable. If you're trading a liquid pair and your thesis depends on a move much larger than that execution gap, the trade may still make sense.

Now compare that with a thinner market. The same Changelly reference notes that volatile or low-liquidity tokens on chains like Solana or Base can see slippage of 1% to 3% or more.

A concrete example: you expect to buy a token at $2.00 and the execution lands at $2.06. The calculation is:

((2.06 - 2.00) / 2.00) × 100 = 3%

That's already large enough to matter. If your strategy depends on a quick flip, 3% on entry can wipe out a big part of the setup before fees and gas even enter the picture.

DEX traders also see slippage in output terms, not just quoted price. If you expected 100 tokens for 1 ETH but received 95 tokens, that's 5% slippage based on output discrepancy.

That format is often easier to feel because it hits the wallet directly. You don't need to debate price formulas when the end result is fewer tokens than expected.

A small slippage figure on a liquid pair is usually execution noise. A larger figure on a memecoin or new listing is often a warning about pool depth, urgency, or both.

For copy traders, that distinction is brutal. If the original wallet entered with low slippage but your mirrored order hits a thinner post-move pool, you're no longer in the same trade. You're in a weaker version of it.

A wallet you follow buys a fresh token on Base. The first fill looks sharp. Thirty seconds later, your copy order hits the same pool and the numbers are different enough to change the trade. That gap usually comes from a small set of causes you can identify before you swap.

Low liquidity is the first thing to check on any speculative token because pool depth sets the cost of being late. On DEXs using AMMs, Kraken's explanation of slippage in crypto notes that high-liquidity pairs such as ETH/USDC on Uniswap V3 can stay below 0.1% slippage for trades under $50K, while low-liquidity memecoins with <$1M depth can see 10% to 50% slippage even on $10K trades.

For copy traders, that difference is brutal. If the lead wallet got in before volume arrived and you follow after social traffic piles in, you are buying from a weaker pool at a worse point on the curve. That is how two traders end up with the same token and very different P&L.

If you need a quick refresher on why reserve depth matters so much, this guide on how crypto liquidity pools work is worth reviewing.

Fast price movement widens the gap between the quote you saw and the fill you get. In memecoin trading, that often happens during launches, influencer callouts, exchange listing rumors, and sharp market reversals.

The practical issue is timing. A quote can look fine when you sign, then become stale by the time validators include the transaction. Copy traders run into this constantly because they are reacting to someone else's entry, not initiating the first move. Wallet tracking tools such as Wallet Finder.ai help here by showing whether you are following a wallet that buys before crowd attention or one that buys after momentum is already obvious. That distinction matters because late copies are far more exposed to slippage.

On DEXs, slippage is built into the pricing model. AMMs like Uniswap use the constant product formula x * y = k. As your order removes tokens from one side of the pool, the execution price gets worse with each increment of size.

That means route quality matters as much as the token chart. A direct swap on a shallow pair can cost more than a multi-hop route through deeper pools. Aggregators often help, but they are not magic. On small caps and new pairs, the available route may still be poor.

Quoted price is a snapshot, not a promise.

That is why memecoin hunters should care about position sizing more than they think. A trader trying to hit a breakout with $500 may get a reasonable fill. The same wallet pushing $5,000 into the same pool can move itself into a bad trade before the market even reacts.

A useful visual refresher on how volatility and execution risk interact:

Some slippage comes from ordinary market movement. Some comes from traders and bots using the mempool against you. If your transaction is visible, large enough, and protected by a loose slippage setting, it can attract front-runs and sandwich attacks.

Kraken notes that MEV bots can amplify effective slippage by 2x to 5x in congested periods, according to Kraken.

The fastest punishment falls upon copy traders and memecoin hunters. A wallet alert goes out, followers rush the same swap, bots see predictable order flow, and the later fills absorb the damage. The setup may still look good on a chart, but your actual entry can be weak enough to ruin the trade before the thesis has time to work.

Most traders think about fees. Fewer think hard enough about execution. That's why slippage keeps showing up as a hidden tax on performance.

Every time your fill is worse than expected, your break-even shifts against you. On entry, you start from a weaker basis. On exit, you keep less of the move you captured. If both sides slip, the financial detriment to your net result escalates even if your directional thesis was right.

Copy trading adds a timing problem on top of an execution problem. You aren't just asking whether the trade is good. You're asking whether it's still good after another wallet has already moved first.

That distinction matters. A sharp on-chain trader can buy into a deep enough pool before the crowd notices. A follower who arrives moments later may face a thinner pool, more competition, and a worse route. At that point, the follower isn't copying the same edge. They're paying for evidence that the edge already existed.

Here's the practical truth: if you consistently enter worse than the wallet you're following, your P&L will diverge even when your token selection matches theirs.

Memecoin setups often rely on speed and asymmetry. The upside can be large, but the margin for a bad fill is small. If the token runs immediately, a sloppy entry still might survive. If it chops, a poor entry becomes dead weight.

That's why many memecoin traders mistake volatility for opportunity when it's really a warning about execution quality. The chart can look explosive and still be structurally hard to trade well.

Good calls don't automatically produce good returns. The fill has to leave room for profit.

Once you take slippage seriously, some trades stop qualifying. That's not conservative. It's disciplined.

A setup can look attractive on paper and still fail your execution test because:

That's why experienced traders reject more trades than they take. Not because they dislike risk, but because they know poor execution can invalidate the idea before the market even has a chance to prove them right.

A copy trader sees a smart wallet buy a fresh Base memecoin, fires a $5,000 market buy two minutes later, and gets a fill that is already several percentage points worse. The token can still go up and the trade can still lose money. That is the practical problem slippage creates. It eats the room your setup needed to work.

The fix starts before you click swap. Slippage control belongs in position sizing, venue choice, and timing. Traders who treat it like a last-second settings toggle usually pay for that mistake in basis points, then in full percentage points when the market is thin.

On DEXs, slippage tolerance is a risk setting, not a convenience setting. For liquid pairs, a tighter tolerance can protect you from paying far above the quote. For fast-moving or thin tokens, that same setting may cause repeated failures, wasted gas, and missed entries.

Use the setting to match the market you are trading:

That last point matters for copy traders. If you need a wide tolerance to get in, you are often entering after the clean money already entered.

On centralized exchanges, limit orders usually beat market orders for execution quality because they cap what you are willing to pay. Kairon Labs found that limit orders on CEXs like Kraken reduced slippage risk by 70% to 90% in backtests (Kairon Labs).

The trade-off is simple. Better price control can mean no fill. For liquid majors, that is often the right compromise. For breakout trades, you may accept partial fills instead of crossing the spread aggressively.

If you want a quick refresher, this guide on what a limit buy order is in crypto covers the mechanics.

For on-chain trades, reducing your footprint usually works better than giving the router more freedom to fill you badly. Kraken notes that splitting large trades into 10 to 20 smaller batches during low-gas windows on L2s like Base can reduce realized slippage by 40% to 60% (Kraken).

That matters most in the exact setups memecoin traders chase. Kraken also notes that for memecoins with less than $1M liquidity, trades as small as $10K can trigger 10% to 50% slippage, often amplified 2x to 5x by MEV bots (Kraken).

If you are using Wallet Finder.ai to track profitable wallets, this is one of the first filters to apply. A wallet's entry might be profitable because it bought early and small. Copying the same token later with 3x the size is a different trade.

Good timing is often just avoiding the worst execution window.

Execution usually improves when gas is lower, swaps are not piling into the same pool, and the route is not being competed away by a wave of followers. On fresh launches and hot meme rotations, waiting even five or ten minutes can change the pool depth, the route quality, and the bot activity around your trade.

That does not mean delay every entry. It means stop treating speed as the only edge. In a crowded copy trade, paying 6% more to be fast can wipe out the advantage of following the right wallet in the first place.

Before sending a DEX order, check a few things in order:

That process sounds basic. It saves real money.

StrategyHow It WorksBest ForKey RiskLimit ordersSets a maximum buy price or minimum sell priceLiquid markets and patient executionMay not fillSlippage tolerance controlRejects trades beyond your allowed execution gapDEX trading in changing conditionsToo tight can fail, too loose can overpayOrder splittingBreaks one large trade into smaller entriesLarge orders and thin poolsTakes longer and may miss a sudden moveBetter timingTrades during calmer network and market conditionsVolatile environmentsWaiting can mean no entrySmaller position sizingReduces your impact on the poolMemecoins and new listingsLower upside if the trade runs immediately

Keep this checklist next to your trade window. It prevents a lot of avoidable mistakes.

Manage slippage like a core risk variable, not a settings menu detail. Traders who do that keep more of the upside they were right to identify in the first place.

Your article's slippage management section covers tolerance settings and the decision to split large orders. There is a third lever that most traders underuse because it requires no settings adjustment at all: routing through a DEX aggregator rather than trading directly on a single protocol.

A DEX aggregator does not hold liquidity. It queries multiple pools and routing paths simultaneously and selects the combination that delivers the best output for your trade. The practical benefit for slippage is direct — instead of sending a large swap through a single Uniswap pool where it moves the price against you, an aggregator splits the order across multiple pools so no single pool absorbs enough volume to generate significant price impact. The aggregate output is better than any single route would produce.

1inch, Paraswap, and CoW Swap are the most widely used on Ethereum in 2026. For Solana, Jupiter is the standard aggregator. Each works slightly differently — 1inch uses Pathfinder to map routes across dozens of liquidity sources, CoW Swap uses a solver competition model where professional market makers compete to fill your order at the best price, and Paraswap's Velora iteration adds intent-based routing that finds optimal execution paths across both on-chain pools and off-chain market makers. The common benefit across all of them is that you are no longer limited to the liquidity depth of a single pool.

For trades in major liquid pairs — ETH/USDC, BTC/USDC on established chains — the routing improvement from an aggregator over a direct Uniswap swap is marginal because the individual pools are already deep enough to absorb normal order sizes without significant price impact. The improvement is still real, but it may represent fractions of a percent rather than multiple percentage points.

For the trades where slippage matters most — mid-cap tokens, new launches, thin DEX pools across multiple chains — the aggregator's routing improvement is most significant. Splitting a $50,000 trade in a token with $500,000 total pool liquidity across three separate pools rather than sending it through one produces meaningfully better output and reduces the MEV bot's opportunity because no single transaction is large enough to be an attractive sandwich target. FoxWallet's June 2026 comparison of DEX aggregators found that route quality, MEV protection mechanism, and gas cost are the three dimensions that determine which aggregator produces the best final output — not quoted slippage percentage alone, because a route with slightly more output may be worse after gas on congested chains. The DeFi analytics tools guide covers how to evaluate on-chain execution quality alongside the signal tools that identify which trades are worth making in the first place.

Wallet Finder.ai helps DeFi traders track profitable wallets, analyze entries and exits, and act faster on real on-chain moves across Ethereum, Solana, Base, and more. If you want a clearer view of wallet behavior before you copy a trade, explore Wallet Finder.ai.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.