Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

May 16, 2026

DeFi didn't become a serious trading arena because people suddenly loved passive yield. It became one because token incentives proved they could pull capital into protocols at extreme speed. When Compound launched COMP in June 2020, one account says its total value locked climbed from under $100 million to over $2 billion within weeks, which helped trigger DeFi Summer, and DeFi TVL broadly expanded from under $1 billion to over $10 billion within roughly three months according to this history of DeFi.

That matters because defi liquidity mining is no longer a side strategy. It's part market making, part token distribution, part competitive intelligence. If you treat it like a static yield product, you'll usually end up holding the bag after emissions fade, volatility expands, or smarter wallets rotate out before you do.

The edge comes from management. Strong miners don't just find pools. They track fee quality, reward durability, pool depth, volatility, and wallet behavior on-chain. They enter with a thesis, monitor like a trader, and exit before a farm turns into a subsidy trap.

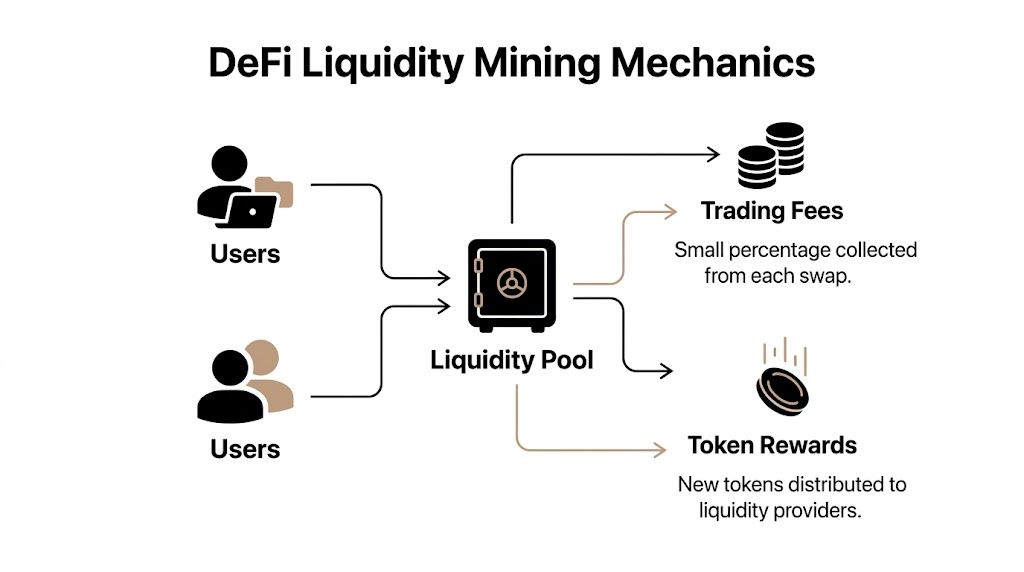

Liquidity mining changed how crypto protocols bootstrap markets. Before it, a protocol had to hope traders or lenders showed up on their own. After it, a protocol could pay users to supply the liquidity that made the product usable from day one.

The basic idea is simple. You deposit assets into a protocol, help it function, and earn two things in return. First, you receive the normal economic output of the venue, such as trading fees or lending interest. Second, you may receive governance tokens, which act a bit like early equity in the protocol.

Compound's COMP launch in mid-2020 gave the model its defining moment. Users weren't just earning from using the protocol. They were also accumulating ownership-linked tokens for participating. That incentive design became the template that many later protocols copied.

A useful way to think about it is this: liquidity mining is like being an early market maker who also gets startup-style upside. You provide the working capital, the protocol pays you for usage, and it may also hand you tokens that could matter if the venue grows.

Practical rule: If a protocol needs liquidity to function, token incentives are one of the fastest ways to buy that liquidity.

The headline opportunity isn't the old mania. It's what the model still does well today:

For traders, the key lesson from DeFi Summer isn't nostalgia. It's that incentives can rewire capital flows very quickly. If you understand where rewards come from and how they decay, you can treat defi liquidity mining as an active strategy instead of a passive promise.

At the mechanical level, liquidity mining is just pooled capital plus a reward schedule. The complexity starts when traders confuse gross yield with realized yield.

According to Amberdata, DeFi total value locked increased from $601 million at the start of 2020 to $239 billion near its 2022 peak, which shows how large this incentive-driven model became across AMMs and lending markets, as described in Amberdata's DeFi primer.

Most positions earn from two buckets:

Trading fees or lending interest

This is the organic part. Traders swap through the pool, or borrowers pay to access capital.

Token emissions

This is the subsidized part. The protocol distributes its own token to attract liquidity.

That distinction matters because fee revenue reflects actual usage, while emissions reflect a temporary policy decision. If most of the yield comes from emissions, the position can weaken fast when incentives drop or when more capital crowds into the same pool.

For a broader primer on the pool side of the trade, this guide to crypto liquidity pools is useful background.

Your earnings depend on your share of the pool. If more liquidity enters, your share shrinks unless volume rises enough to offset that dilution. That's why TVL is a useful context metric but never a buy signal by itself.

A practical way to read the setup:

| Metric | What it tells you | What can go wrong |

|---|---|---|

| TVL | How much capital is competing for fees and rewards | High TVL can dilute returns |

| APR/APY | Advertised reward rate | Often changes quickly |

| Fee share | Whether the pool has real usage | Can be weak even in popular pools |

| Emission share | How much subsidy supports the yield | Usually decays over time |

When I evaluate a pool, I break it down like this:

High APR with weak fee generation usually means you're being paid to underwrite someone else's liquidity problem.

Not all liquidity mining is the same trade. The reward screen may look similar, but the operating model behind the pool determines how much work the position requires and where the risk sits.

| Model | How It Works | Best For | Primary Risk |

|---|---|---|---|

| Standard AMM LP rewards | Deposit both assets into a broad pool and earn fees plus any incentives | Traders who want simple deployment and easier monitoring | Impermanent loss and reward decay |

| Concentrated liquidity | Allocate liquidity inside a chosen price range for denser fee capture | Active traders who can rebalance and monitor price behavior | Going out of range and stopping fee generation |

| veToken models | Lock a governance token to boost rewards or direct emissions over time | Longer-term participants who want influence and stickier yield | Lockup risk, governance complexity, and lower flexibility |

This is the familiar model from early DEXs. You add both sides of a pair, receive LP exposure, and collect fees plus any farm incentives. It's simple, which makes it attractive to newer liquidity providers and to traders who don't want to babysit ranges.

The weakness is that simplicity attracts competition. Once a pool gets crowded, the advertised yield can compress quickly, especially if emissions were doing most of the work.

Concentrated liquidity changed the game for active LPs. Uniswap v3-style design lets you place capital inside a chosen price band instead of across the full curve. That can materially improve fee capture per dollar of liquidity, but narrower ranges also raise the odds that price moves outside your band and the position stops earning, as explained in this advanced liquidity mining guide.

This is why I treat concentrated LP positions like inventory management, not passive yield. You need a view on volatility, expected trade flow, and how often you're willing to rebalance.

The best concentrated range isn't the one with the highest theoretical fee density. It's the one you can actually manage.

veToken systems introduced a different logic. Instead of merely rewarding whoever arrives first, they reward longer commitment. Users lock a governance token, gain influence over emissions or reward boosts, and often align themselves with the protocol over a longer horizon.

These models can be attractive if you want to participate in a more stable incentive structure. They can also trap capital if governance turns messy or if the token's utility weakens. The trade is less about pure APR chasing and more about whether the incentive system creates durable demand.

Use the model that fits your operating style:

Liquidity mining can look profitable right up to the point where one risk overwhelms everything else. In practice, three risk buckets matter most: impermanent loss, protocol risk, and exit reality.

Impermanent loss happens when the two assets in your pool move apart in price. The pool rebalances automatically, which means you end up with a different asset mix than if you had held both tokens outside the pool.

A simple example makes the pain obvious. Suppose you deposit one volatile asset and one stable asset in equal value. If the volatile asset rallies hard, the pool systematically sells part of your winner into the weaker side. You may still earn fees, but you now own less of the asset that ran. If fees don't cover that shortfall, the LP position underperforms holding.

That's why an impermanent loss calculator is useful before entering any volatile pair. You want a rough sense of how much price divergence the fee stream can realistically absorb.

The highest advertised APRs often come from the newest protocols trying to attract TVL. The problem is that the newest protocol can also carry the highest risk of unknown vulnerabilities, and headline APR often says little about net realized returns after fees, slippage, and short holding periods, as noted in this De.Fi discussion of liquidity mining rewards.

Here's the defensive checklist I use before touching a new farm:

| Red flag | Why it matters |

|---|---|

| Very new protocol with extreme advertised yield | Often buying TVL before the market knows the real risk |

| Thin pool depth | Harder to exit without giving up a chunk of returns |

| Weak product usage | Fees may not survive once incentives fade |

| Confusing token emissions | Hard to estimate dilution and reward normalization |

If you can't explain how you'll exit a position, you haven't finished evaluating the entry.

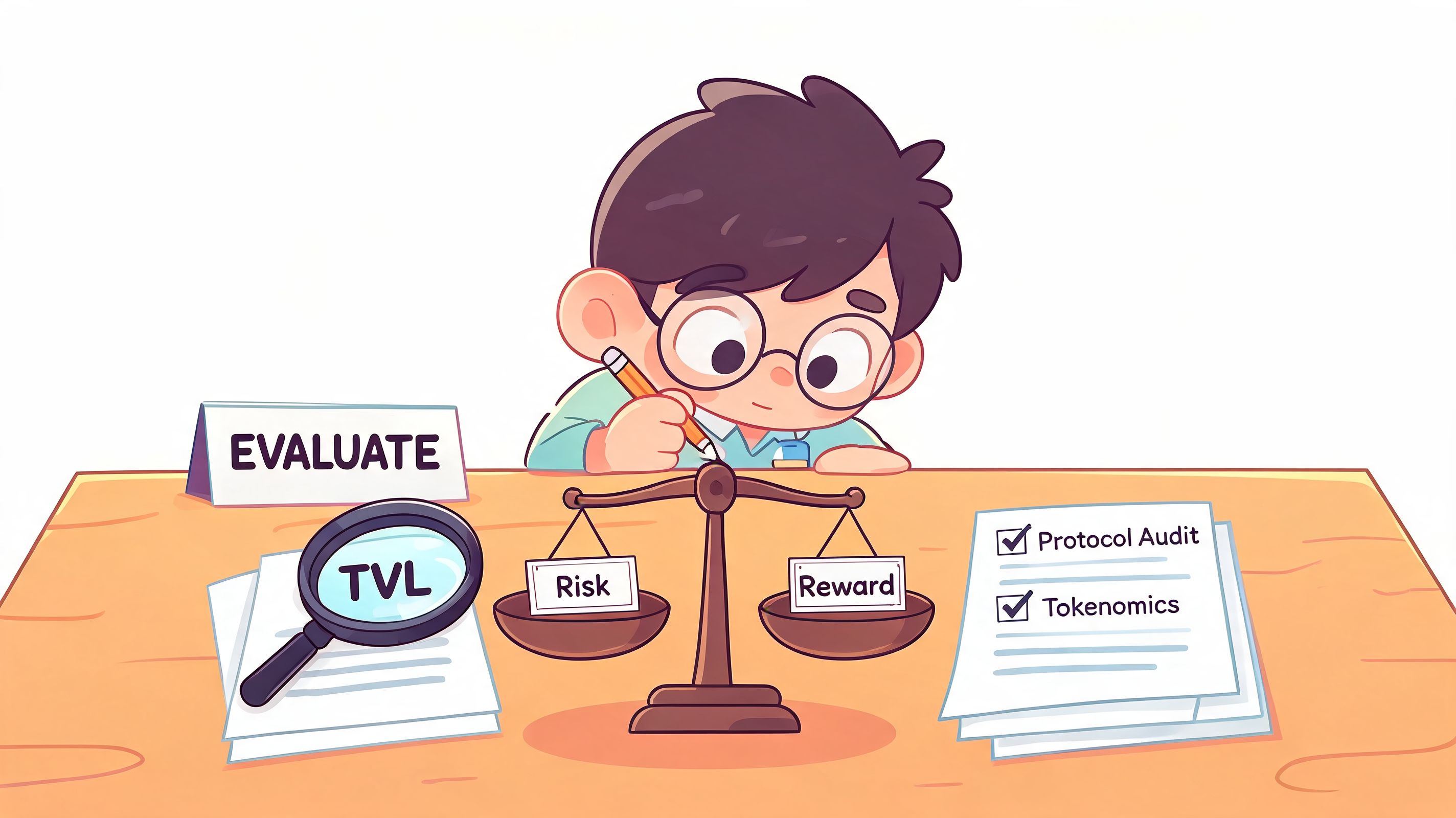

Most bad LP decisions come from looking at one number. Usually it's APR. Good evaluation starts when you separate advertised yield from investable yield.

Top-performing wallets often rotate liquidity rather than hold it passively because returns are often overstated when impermanent loss and pool quality are ignored. Net performance depends on whether fee income exceeds the mark-to-market loss from price divergence, which is why it helps to compare pool APR to historical volatility and track TVL trends before deploying capital, as described in this Binance Square post on liquidity mining analysis.

I use five filters.

Ask one question first: Would this pool still be interesting if emissions were cut?

If the answer is no, you're probably looking at a short-duration trade rather than a durable one. That's fine, but you should treat it as tactical capital, not sticky capital.

Emissions don't just pay you. They also attract competitors. When mercenary capital arrives, your share gets diluted and the token itself may face more selling pressure.

Look for signs of sustainability:

Different pools deserve different standards. Stable or tightly correlated pairs can tolerate a different entry logic than volatile pairs. Concentrated liquidity positions need even more scrutiny because the position can stop earning when price leaves the band.

I also look at pool depth and time-to-exit. A pool may look attractive on paper but become untradeable once you include slippage and the cost of repositioning.

For a more systematic process, this guide on building a liquidity pool risk scoring framework is a good way to formalize decision criteria.

| Evaluation area | What to check | Good sign | Weak sign |

|---|---|---|---|

| Yield composition | Fees vs emissions | Real usage supports returns | Emissions dominate |

| Pool depth | Ease of entry and exit | Clean execution | Fragile liquidity |

| Volatility fit | Pair behavior vs your strategy | Range matches expected price action | Position likely to drift or break |

| Reward durability | How long incentives remain attractive | Slower decay, clearer logic | Fast normalization, crowding |

| Wallet behavior | What strong participants are doing | Disciplined rotations | Retail pile-in after hype |

A short explainer can help frame the workflow before you deploy capital.

Raw protocol pages rarely tell the full story. On-chain behavior fills the gap.

I watch for:

That's the difference between reading a farm page and evaluating a trade.

The most useful case studies in liquidity mining aren't vanity wins. They're examples of why one structure remained investable longer than another.

A stronger liquidity mining program usually has three traits. It sits on top of real user demand, it doesn't rely entirely on emissions, and participants have a reason to stay once the initial reward spike cools.

Early blue-chip DeFi programs that survived the first reward rush generally earned that survival. They paired incentives with products traders already needed, such as deep swap liquidity or borrowing demand. That meant LPs weren't depending solely on governance-token distribution to justify staying in the pool.

A good concentrated-liquidity example follows the same pattern. The trade works when the pair has consistent flow, the chosen range reflects actual market behavior, and the LP actively repositions around volatility instead of treating the band as permanent.

Good liquidity mining campaigns don't just attract capital. They keep capital after the novelty fades.

The bad version is easy to recognize after you've seen it a few times. A new protocol launches with flashy APR, thin real usage, and token rewards doing all the heavy lifting. Liquidity arrives fast, the token gets sold, effective yield degrades, and exits become uglier than the farm page implied.

The visible warning signs usually appear early:

You don't need a dramatic collapse to lose money in defi liquidity mining. A mediocre farm can grind you down through dilution, weak fees, poor exits, and asset divergence.

The useful lesson is comparative. Strong programs create returns from actual usage and use incentives as an accelerant. Weak programs use incentives as a substitute for product demand. Traders who can tell the difference early usually keep more of what they earn.

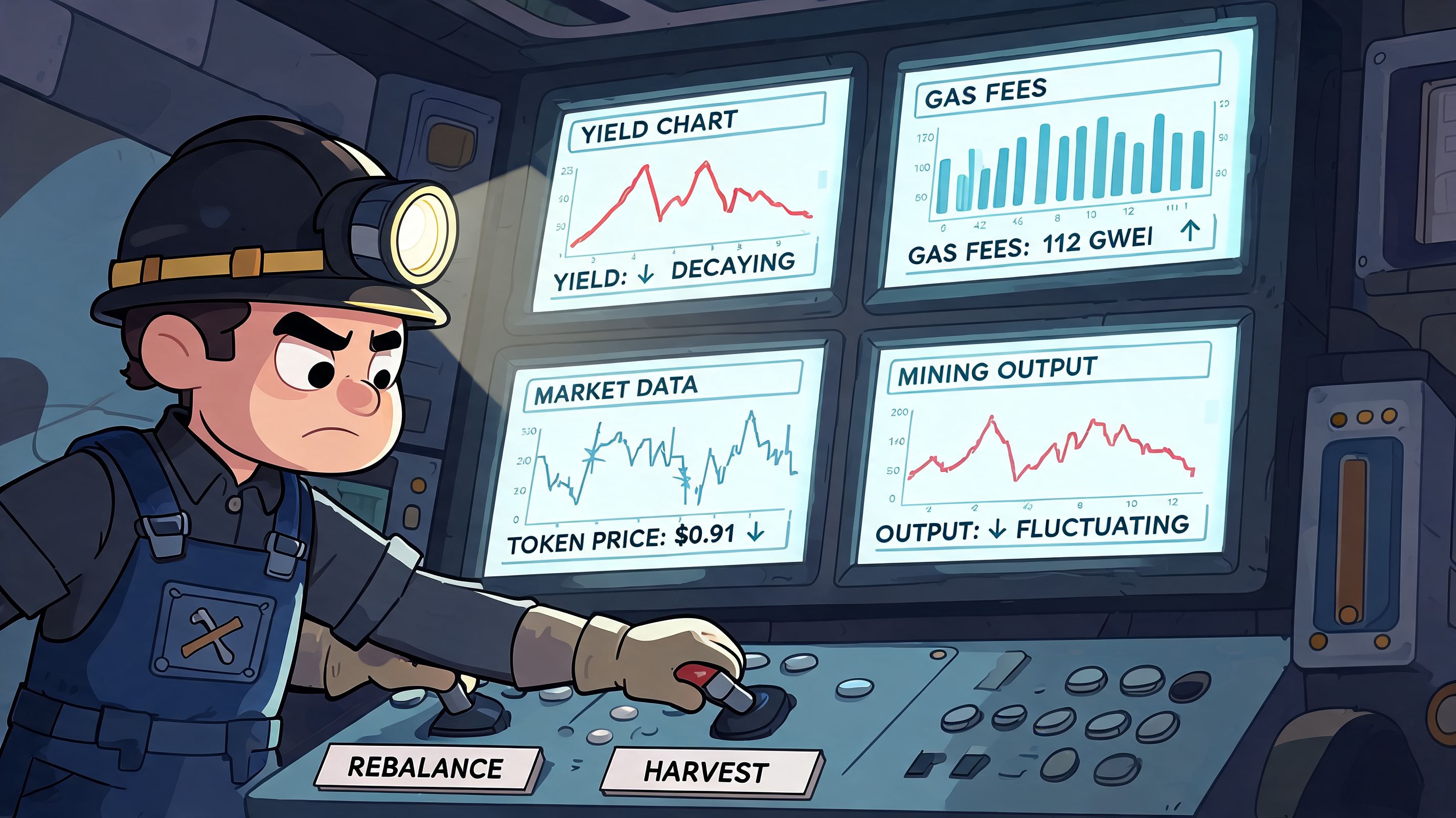

At the advanced level, liquidity mining looks less like “deposit and wait” and more like a surveillance workflow. You're tracking yield decay, wallet movement, volatility, and execution costs across chains and pools. That's where active miners separate from passive LPs.

One guide notes that DeFi is shifting from high-risk, high-reward models toward more sustainable systems, including revenue sharing and dynamic APYs. The practical question becomes not “where is the highest yield?” but how quickly rewards normalize once mercenary capital arrives, which is why it makes sense to focus on reward half-life, competitor saturation, and post-emission yield persistence, as discussed in this guide to DeFi mining sustainability.

Here's a professional loop that works better than browsing APR dashboards.

Start with on-chain discovery tools. Debank, Dune dashboards, protocol explorers, and wallet tracking platforms can help isolate addresses that repeatedly manage LP positions well. One option is Wallet Finder.ai, which tracks wallet histories, trade timing, and alerts across major ecosystems.

Don't chase a single big winner. Look for repeat behavior across multiple positions.

Once you have a candidate wallet set, study:

This step matters more than copying blindly. You want the decision rules, not just the destination.

Most profits in active mining come from reacting before the dashboard updates become obvious.

Useful alert conditions include:

| Alert type | Why it matters |

|---|---|

| Large LP entry by a proven wallet | Signals a fresh opportunity worth checking |

| Range adjustment in concentrated liquidity | Reveals how strong operators respond to volatility |

| Reward token selling after harvest | Shows whether emissions are being treated as cash flow or conviction |

| Rapid TVL crowding in a pool | Warns that return dilution may already be underway |

The wallet isn't valuable because it's smart. It's valuable because its behavior is observable before most traders interpret it.

Active miners need explicit rules for when to do nothing, when to harvest, and when to move. I use a simple operating framework:

This is the core bridge between DeFi analysis and copy trading. You aren't just finding yield. You're tracking how skilled wallets manage inventory under changing market structure.

If you want to turn defi liquidity mining into a repeatable workflow instead of a one-off farm bet, use Wallet Finder.ai to study how profitable wallets enter pools, rotate rewards, and react to changing on-chain conditions. The platform is most useful when you treat it as a research layer. Build watchlists, track timing, and use alerts to spot moves before crowded capital compresses the edge.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.