Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

June 9, 2026

You're usually not opening the FFIEC APR calculator because everything is going smoothly. You open it when a disclosure looks close, but “close” isn't good enough. A fee was reclassified. The first payment date shifted. The payment stream has one irregular period. Someone wants to know whether the disclosed APR still holds.

That's the right time to use the FFIEC APR Calculator. Not to create the loan. Not to guess. To verify what's already on paper and decide whether the disclosure can stand.

A lot of confusion comes from treating the calculator like a lending platform feature. It isn't. Used correctly, it's a compliance control. Used carelessly, it gives a false sense of security because the math only reflects the data you feed it.

When a loan file is moving toward closing, APR verification is one of those tasks that can look routine until it suddenly isn't. An odd first period, a prepaid charge, or a real estate-secured structure can turn a simple check into a real compliance question. That's why the FFIEC tool matters. It gives institutions a standardized federal method to verify disclosed APRs and finance charges instead of relying only on internal spreadsheets or vendor outputs.

The federal release announcing the tool matters for another reason. The FFIEC APR Computational Tool was announced on April 16, 2020, and it was built by FFIEC member agencies to help verify finance charges and APRs under the Truth in Lending Act and Regulation Z. It supports unsecured and secured installment loans, construction loans, real estate-secured loans, and checks for MAPR limits under the Military Lending Act, as described in the FFIEC Federal Disclosure Computational Tools announcement.

That scope tells you something important. This isn't a niche calculator for one product type. It's a federal verification utility intended for the same general compliance environment examiners work in.

If you're new to APR testing, don't confuse conceptual learning with compliance verification. A consumer explainer such as this guide to APR vs APY calculators can help with terminology, but the FFIEC tool serves a different purpose. It checks whether your disclosed loan terms hold up under regulatory calculation logic.

Practical rule: If a loan disclosure is going out the door, a second calculation source is a control. If the file is complex, that control stops being optional.

A junior analyst often asks whether the calculator is “required.” The better question is whether your process is defensible without an independent verification step. In straightforward files, internal systems may be right. In messy files, confidence without verification is where avoidable errors start.

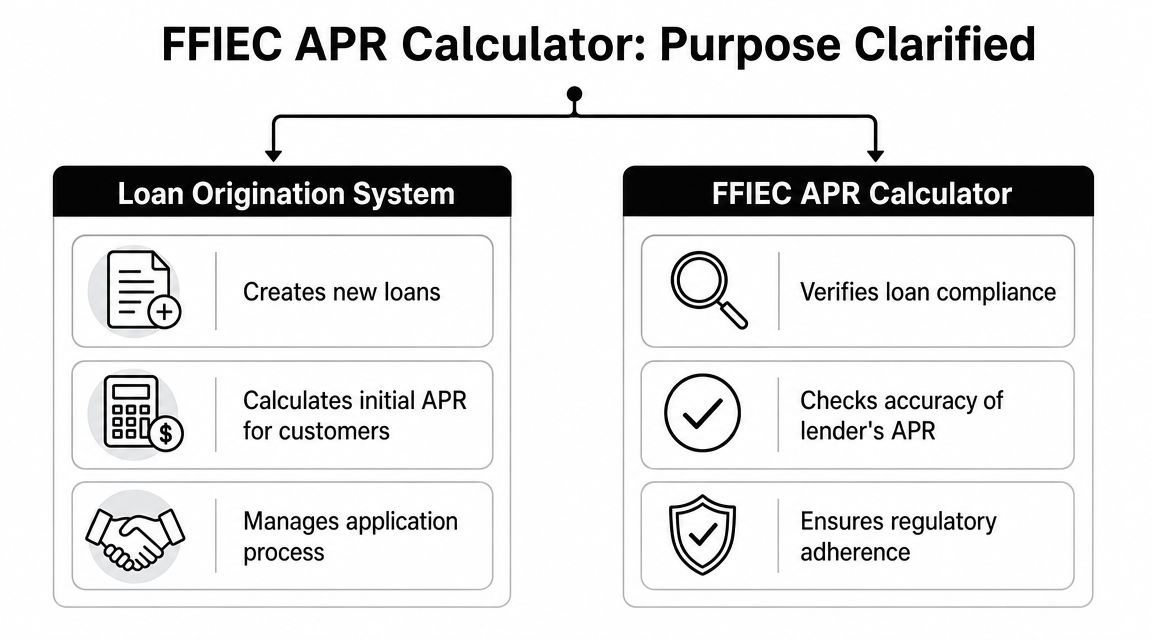

The most common mistake is using the FFIEC APR calculator as if it were a loan origination system. That's not what it does. It doesn't build a loan, manage an application, or generate production disclosures for borrowers. Its job is narrower and more useful: verify whether the disclosed APR and finance charge align with the actual contract terms you entered.

In practice, the workflow is simple. You take the loan terms from the contract or closing statement, enter them into the calculator, and compare the tool's output to the disclosed figures. That makes it a control layer.

That distinction affects who should use it and when:

A loan origination system has a very different role. It captures borrower data, applies product logic, calculates proposed terms, produces workflow outputs, and pushes a file through operations. The FFIEC tool doesn't replace any of that.

If you enter estimated data, outdated fees, or a payment schedule that doesn't match the note, the calculator will still give you an answer. It just won't be the answer you need.

That's why people get into trouble when they call it a “calculator” and stop there. The name sounds general. The compliance use is specific.

A lot of institutions still have process habits from older desktop tools. The OCC confirmed that APRWIN and APYWIN were discontinued in favor of the FFIEC Federal Disclosure Computational Tools, and the old Windows programs are no longer available, according to OCC Bulletin 2020-40.

That change wasn't just cosmetic. It moved many teams from a legacy desktop workflow to a web-based federal utility. If your department once relied on APRWIN screenshots, saved local files, or analyst-specific habits, your procedures had to change.

A workable modern approach usually includes:

| Workflow Area | What Works | What Doesn't |

|---|---|---|

| Input preparation | Pull terms from final executed documents | Keying from memory or preliminary drafts |

| Verification timing | Run after all fees and payment terms are settled | Running too early and assuming nothing changed |

| Documentation | Save the result with notes on assumptions used | Keeping only a verbal sign-off |

| Escalation | Flag variances for compliance review | Letting operations “fix later” without analysis |

The institutions that use the FFIEC APR calculator well treat it as a formal checkpoint. The ones that struggle tend to treat it like a convenience feature.

The calculator is only as good as the data you enter. Most bad APR verification work comes from one of two problems: someone used incomplete documents, or someone entered the right figures in the wrong form. Before opening the tool, gather the loan terms from the final documentation set and reconcile anything that changed during closing.

Use the note, final disclosure, closing statement, and any fee detail your institution relies on to determine the finance charge. Don't mix early disclosures with final terms. Don't assume the payment stream in the system is identical to the executed documents.

If your team works across multiple calculators, keep them separate in your mind. A market-oriented tool such as this review of the best crypto calculator app serves a completely different use case from federal APR verification. For compliance, source documents matter more than interface convenience.

| Data Point | Description | Where to Find |

|---|---|---|

| Loan amount | The principal amount being financed under the loan terms | Note, loan agreement, closing package |

| Finance charge | Charges treated as finance charge for APR purposes | Disclosure, fee worksheet, closing statement |

| Amount financed | The amount after accounting for applicable prepaid finance charges | Final disclosure or internal calculation support |

| Payment amount | Each scheduled payment amount | Note or payment schedule |

| Number of payments | Total scheduled payments in the stream | Note, amortization schedule |

| Payment frequency | Monthly, biweekly, or other periodic structure used in the contract | Note and payment schedule |

| First payment timing | The date or period until the first scheduled payment | Note, closing disclosure, contract terms |

| Irregular periods | Odd first period, skipped period, or nonstandard interval if applicable | Note riders, payment schedule, closing documents |

| Final payment details | Balloon or irregular final payment if applicable | Note, amortization schedule |

| Loan type basis | Whether the transaction should be tested as interest-bearing or precomputed | Product terms, note structure |

| MAPR-related inputs if applicable | Terms needed to assess Military Lending Act limits for applicable installment loans | MLA review file, contract, fee support |

Clean input beats fast input. Slow down long enough to reconcile the documents before you start typing.

A disciplined analyst builds a short intake sheet before using the calculator. That step feels manual, but it prevents reruns and avoids the worst habit in APR testing, changing fields until the output “looks right.”

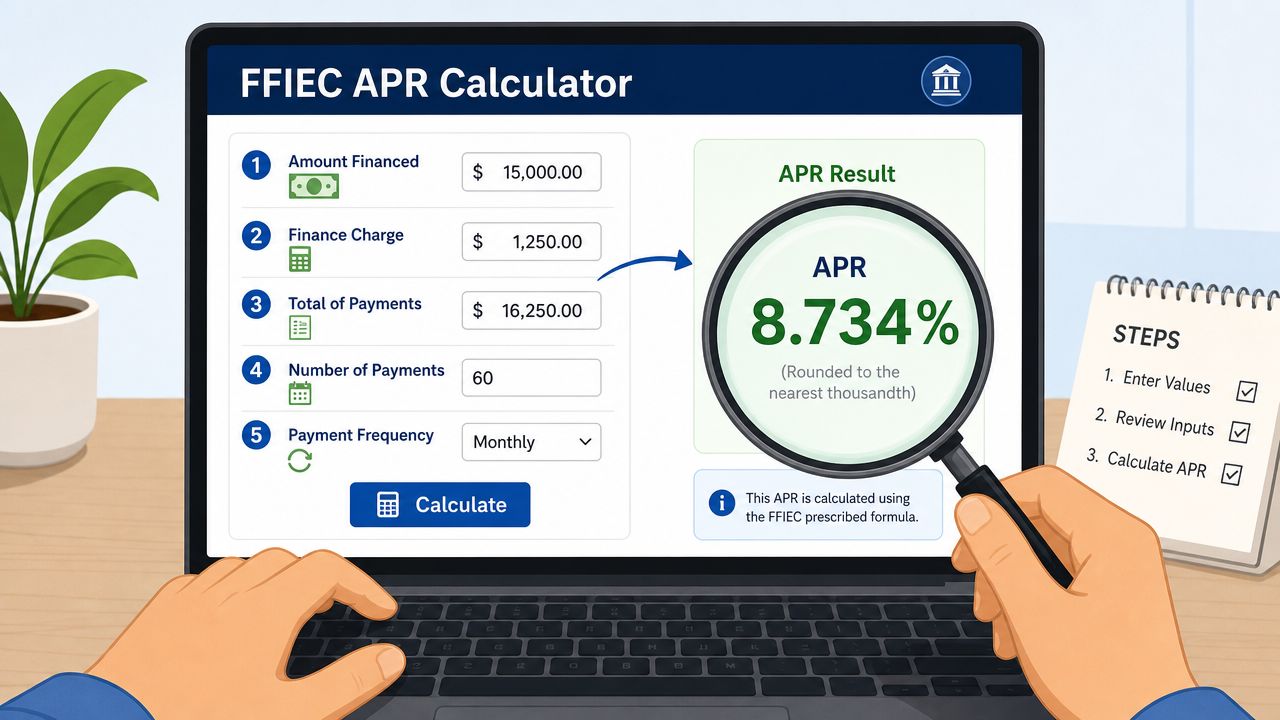

The best way to learn the FFIEC APR calculator is to treat it like a file review, not a math exercise. You start with a closed set of terms, choose the right loan structure, enter the payment pattern exactly as documented, and compare the output to the disclosed APR.

Use the interface as a verification screen. Don't use it as a place to invent assumptions.

I'm not going to fabricate a sample loan with made-up figures. Instead, use your own institution's nonpublic training file or a sanitized prior file and walk through it exactly this way:

The interface tends to make more sense once you stop thinking about labels in the abstract.

After you've entered the file, stop and compare the inputs back to the documents before hitting calculate. Performing this comparison helps many analysts avoid false discrepancies.

Review habit: Read the payment pattern out loud from the note and compare each field on screen. It sounds basic, but it catches more errors than advanced troubleshooting does.

A short walkthrough can help if your team is training new staff on the interface:

Treat the output as a compliance checkpoint.

If it aligns with the disclosed APR, document the verification and save enough support so another reviewer can understand what you tested. If it doesn't align, pause the file review and isolate the issue. In my experience, the cause is usually one of these:

The strongest analysts don't celebrate when the number matches. They confirm why it matches. That's what makes the file defensible later.

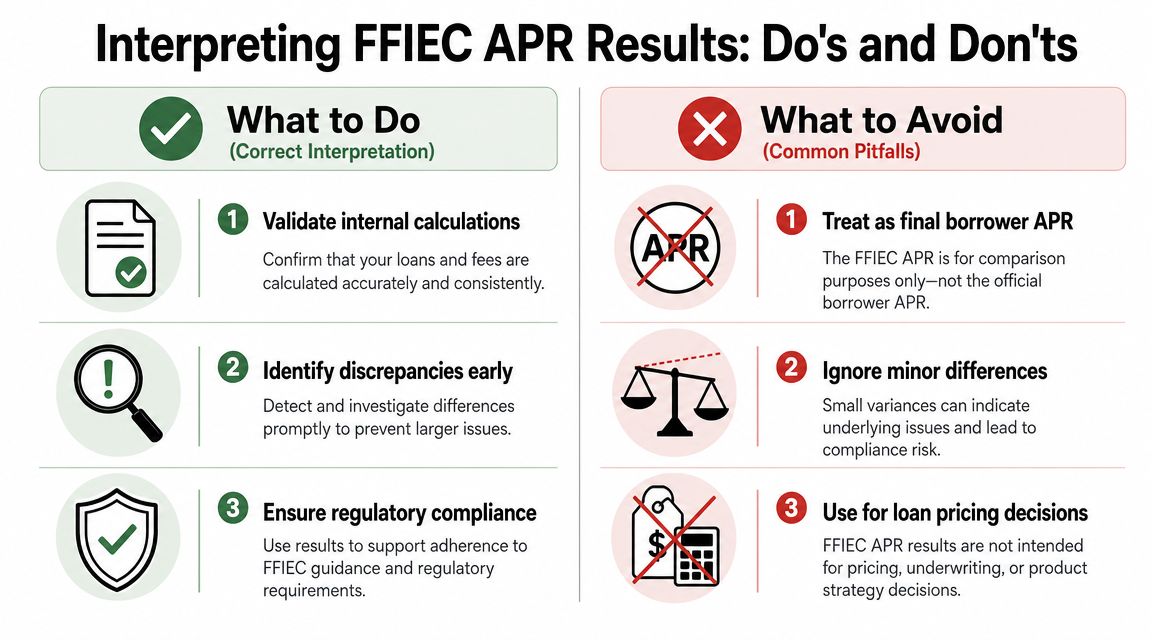

When the FFIEC APR calculator gives you a result, the job isn't finished. The output is useful only if you know what it confirms and what it doesn't. It confirms whether the terms you entered produce the APR you're testing. It doesn't prove your fee analysis was correct, your source documents were complete, or your internal disclosure process was sound.

The tool is best used as a final mathematical check against the actual contract. That aligns with how the web-based FFIEC utility is described in practice, where institutions enter final contract inputs to check disclosed APRs and, for applicable installment loans, MAPR limits under the Military Lending Act, as summarized in this discussion of the FFIEC APR and APY calculation tools.

A good verification record answers three questions:

| Question | What you should confirm |

|---|---|

| What was tested | The specific final loan terms and documents used |

| What did the tool return | The APR result produced from those inputs |

| What was done with the result | Matched, escalated, or corrected |

That last part matters. If the output differs from the disclosure, don't treat it like a minor nuisance. Open an issue and determine whether the problem sits in finance charge treatment, payment structure, or data entry.

Don't describe a variance as “small” until you know why it exists. Small differences can still point to a process problem.

A mature team doesn't stop at the number. It uses the result to improve controls. That can include a post-close exception log, a second-person review on complex structures, and targeted retraining when the same error pattern appears more than once.

That's also where broader performance thinking helps. A compliance team can borrow the discipline of a measurement mindset without confusing it with lending rules. Tools that frame decision quality, such as an ROI calculator, remind analysts to connect outputs to process consequences. In APR work, the consequence isn't campaign efficiency. It's whether your disclosure process is reliable and defensible.

A matched result means the entered terms worked mathematically. It does not excuse weak documentation.

A solid APR verification process doesn't live in one analyst's browser history. It belongs in policy, procedure, training, and quality control. If your institution uses the FFIEC APR calculator regularly, that use should be written down the same way any other compliance control is written down.

Examiners usually care less about whether a team says it “checks APR” and more about whether the institution can show a repeatable control. Good evidence includes saved results, notes on unusual structures, and proof that variances were reviewed rather than ignored.

A strong compliance program also accepts the limit of the tool. The calculator helps verify. It doesn't replace policy judgment, finance charge analysis, or oversight. Teams that understand that boundary tend to produce cleaner files and better remediation records.

If you spend your day validating numbers, spotting patterns, and making decisions from messy data, Wallet Finder.ai gives you a similar kind of edge in crypto markets. It helps traders track wallets, trades, and token activity across major chains so they can study what high-performing participants are doing and act faster on real on-chain signals.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.