Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

May 6, 2026

You’re probably here because you’ve already hit the same wall most first-time bot builders hit. You can code, you know the market basics, you’ve tested a few indicator ideas, and yet every path seems to collapse into the same commodity logic: RSI crosses, moving average crossovers, Bollinger reactions, and bots that look clean in a notebook but fall apart when money is on the line.

That’s usually not a coding problem. It’s an edge problem.

If you want to learn how to make a trading bot that has a real shot in crypto, especially in DeFi, start with a signal source that isn’t already baked into every public chart. Price indicators are useful as filters. They’re weak as your only source of intent. On-chain wallet behavior is different. It shows who acted, when they acted, and often how they sized the trade.

Open your wallet tracker after a sharp move and you will often see the actual sequence in plain view. A small group of wallets accumulated before the chart looked obvious, retail volume arrived later, and indicator-only bots entered after the easy part of the move was gone. That gap is where a DeFi bot can still have an edge, but only if the strategy is defined before the code.

Write the trade idea in one sentence that can be proven wrong. If you cannot do that, the bot will drift into feature creep and curve-fit itself around noise.

Good hypotheses for an on-chain bot usually look like this:

That last point breaks a lot of first builds. Wallet tracking gives you intent. It does not outsource risk management.

RSI, MACD, and moving averages are easy to code and easy to test. They are also visible to everyone. In DeFi, that usually makes them better as filters than as the primary reason to take a trade.

The stronger approach is to treat price as confirmation and wallet behavior as the signal source. If a tracked wallet starts building size in a token before attention reaches the chart, you are reacting to participant behavior rather than recycled price math. This is the primary advantage behind smart money wallet tracking in crypto.

I use indicators sparingly here. They help reject bad entries. They rarely create the edge by themselves.

Do not mix three bot styles into version one. Pick the job your bot will do, then accept the operational constraints that come with it.

| Strategy archetype | What drives the signal | Where it works | Common failure mode |

|---|---|---|---|

| Wallet mirroring | On-chain buys, sells, sizing, timing | Fast DeFi rotations, narrative tokens | Following weak wallets, reacting too late |

| Event reaction | Listings, contract changes, liquidity additions | Launch periods, catalyst-driven trades | Latency, spoofed momentum, poor fills |

| Mean reversion | Short-term price dislocation | Deep, liquid pairs | Standing in front of a real trend |

| Grid or DCA automation | Predefined order placement | Specific regimes with stable assumptions | Running the wrong structure in the wrong regime |

For a first serious DeFi bot, wallet mirroring is usually the best place to start because the signal source is tied to actual capital movement. The trade-off is execution pressure. If the source wallet trades illiquid names, your bot can still lose on a good read because your fill quality is worse.

The strategy should specify the conditions for entry, the conditions for rejection, and the conditions for exit. Keep those rules mechanical enough that two developers would implement them the same way.

A workable example:

Many first-time builders often overestimate copying and underestimate translation. A whale can ladder into weakness, hold through a 25 percent drawdown, and exit in fragments across venues. Your bot needs a version of that behavior that fits your capital, latency, and risk tolerance.

Decide what success means now. Otherwise you will keep tweaking parameters until the backtest looks clean and the live bot behaves like a different system.

Use practical measures: net profitability after fees and gas, drawdown, slippage, missed-trade rate, and how often a signal could be executed at the intended size. If those numbers are weak, the strategy is weak, even if the chart annotations look convincing.

A bot with a clear edge is easier to build than a bot searching for one after the infrastructure is already in place.

The edge in an on-chain bot comes from wallet selection, not from scraping random transactions and hoping volume equals skill.

A profitable-looking wallet can still be unusable as a bot signal source. You want wallets whose behavior can be translated into rules.

Good candidates usually show:

A disciplined process is better than chasing the latest “smart money” thread on social media. I’d build a watchlist in layers:

Separate by chain and market style

Don’t mix Solana memecoin snipers with slower Ethereum DeFi rotation wallets. Their time horizons and execution assumptions are different.

Review trade history manually

Look at entry clustering, average hold time, and whether the wallet buys breakouts, dips, or fresh listings.

Reject wallets with uncopyable behavior

Some wallets succeed because they have access, speed, or size advantages you can’t replicate. A good signal source for a bot has to be operationally usable.

Classify exits

Many builders get lazy here. If the wallet exits in fragments while your bot only supports full exits, your backtest will lie to you.

A simple review framework helps:

| Review lens | What you want to learn | Why it matters for automation |

|---|---|---|

| Entry timing | Early, reactive, or late | Determines latency tolerance |

| Position sizing | Fixed, convex, or discretionary | Tells you whether to mirror size or normalize it |

| Hold duration | Minutes, hours, days | Shapes your polling and execution design |

| Sell behavior | Full exit or scaling | Drives exit logic architecture |

The strongest wallets aren’t just profitable. They’re legible.

One practical option for this workflow is Wallet Finder.ai, which surfaces wallet trade history, timing, position sizing, and watchlist-based alerts. If you’re still defining what “smart money” looks like operationally, this explainer on smart money in crypto is a useful starting point.

Once you’ve found a handful of credible wallets, reduce their behavior into machine-readable conditions.

For example:

That’s the key transition from on-chain research to bot design. You’re not copying personalities. You’re extracting patterns.

Most first bots fail because everything is jammed into one file. Signal discovery, state tracking, exchange logic, and risk checks all live in one loop. That’s easy to start and miserable to debug.

If you’re serious about learning how to make a trading bot, keep the system boring and modular.

A clean structure looks like this:

That separation saves you later when something goes wrong and it will.

Python is the default choice for this kind of build because it’s readable, fast enough for many signal-driven systems, and has strong libraries for APIs, data handling, and backtesting.

Here’s a simple architecture sketch:

from dataclasses import dataclassfrom typing import Dict, Any@dataclassclass Signal:token: strchain: straction: strsource_wallet: strtimestamp: strmetadata: Dict[str, Any]class RiskManager:def __init__(self, max_position_notional, max_daily_loss):self.max_position_notional = max_position_notionalself.max_daily_loss = max_daily_lossdef approve(self, signal: Signal, portfolio_state: Dict[str, Any]) -> bool:if portfolio_state.get("daily_loss_limit_hit"):return Falseif portfolio_state.get("planned_notional", 0) > self.max_position_notional:return Falsereturn Trueclass ExecutionClient:def place_buy(self, token: str, amount: float):print(f"BUY {amount} of {token}")def place_sell(self, token: str, amount: float):print(f"SELL {amount} of {token}")class Bot:def __init__(self, risk_manager, execution_client):self.risk = risk_managerself.execution = execution_clientdef on_signal(self, signal: Signal, portfolio_state: Dict[str, Any]):if not self.risk.approve(signal, portfolio_state):return "rejected"if signal.action == "buy":self.execution.place_buy(signal.token, portfolio_state["planned_amount"])return "buy_sent"if signal.action == "sell":self.execution.place_sell(signal.token, portfolio_state["position_amount"])return "sell_sent"return "ignored"This isn’t a full bot. It’s the right shape for one.

Your signal path and your execution path should be loosely coupled. If your wallet tracker sends an alert, don’t let that alert directly fire a trade with no validation.

Use an intake layer that checks:

If you’re wiring execution into exchange infrastructure, this overview of crypto exchange APIs is useful for thinking through authentication, order routing, and the differences between data APIs and trading APIs.

After the architecture is in place, it helps to watch another developer walk through a live bot build process.

Your order code should do one thing at a time. Don’t combine signal parsing, sizing, and order submission in a single function.

Example patterns:

def get_account_balance():# fetch from exchange or walletreturn {"USDC": 1000}def calculate_order_size(balance_usdc, risk_fraction, entry_price):notional = balance_usdc * risk_fractionreturn notional / entry_pricedef place_limit_buy(symbol, quantity, limit_price):print(f"Placing limit buy for {quantity} {symbol} at {limit_price}")def place_market_sell(symbol, quantity):print(f"Placing market sell for {quantity} {symbol}")Small functions expose bad assumptions fast. Big functions hide them until live trading.

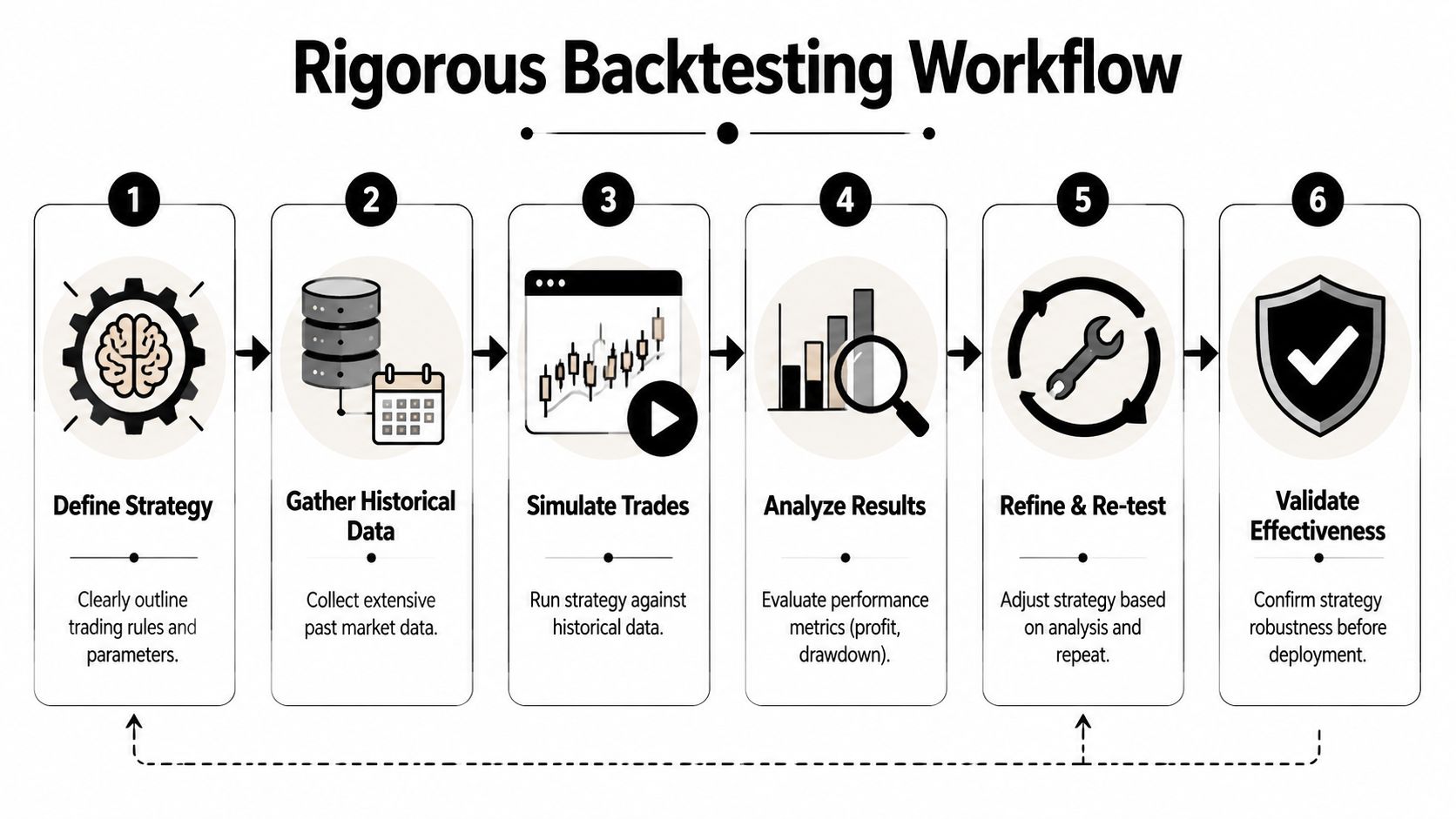

Backtesting isn’t there to make you feel good. It’s there to disqualify fragile ideas before they touch capital.

A professional bot development process uses a three-phase methodology of supervised learning, reinforcement learning, and rigorous backtesting with walk-forward analysis. The walk-forward part matters most for most builders. You optimize on one historical window, test on the next, and repeat that sequence to reduce overfitting, as described in Amplework’s trading bot development breakdown.

Even if you’re not building a full ML stack, the principle still applies. Train or tune on one slice. Validate on the next. Never let the bot “see” the full answer sheet.

A basic backtest often fails in three predictable ways:

That’s why backtesting should include multiple scenarios, realistic datasets, and metrics beyond profit. The development guidance from KJ Trading Systems on creating an automated trading bot stresses parameter optimization around entry, exit, stop-loss, and take-profit, while also requiring out-of-sample data and review of cumulative profit, drawdown, and trade frequency.

Don’t obsess over win rate in isolation. A backtest with a 70% win rate and 30% drawdown is unhealthy unless you understand the logic behind it, a point noted in the AI trading workflow discussed earlier.

Use a minimum review set like this:

| Metric | Why it matters | What it tells you |

|---|---|---|

| PnL | Raw profitability | Whether the strategy makes money at all |

| Maximum drawdown | Worst peak-to-trough decline | Whether the strategy is survivable |

| Sharpe ratio | Return relative to total volatility | Whether returns came with chaotic risk |

| Sortino ratio | Return relative to downside volatility | Whether losses are concentrated and ugly |

| Trade frequency | Number of trades over time | Whether the strategy is too sparse or too noisy |

| Latency sensitivity | Execution delay impact | Whether your edge disappears in the real world |

A practical workflow for this is a detailed guide to backtesting trading strategies, especially if you’re converting event-style wallet signals into simulated entries and exits.

Wallet-based systems need an extra layer of skepticism. A wallet that looked elite in one period may degrade, rotate styles, or stop trading entirely.

Use walk-forward tests like this in concept:

That process is annoying. It’s also the difference between research and self-deception.

A wallet bot should be tested as if you were living inside the timeline, not browsing it after the fact.

A bot that follows the right wallet can still lose money for boring reasons. The signal is good. The deployment is sloppy. A node lags, a signer retries twice, gas spikes, the bot enters late, and a controlled setup turns into a bad fill.

That is why risk and deployment belong in the same conversation. For signal-driven bots, especially ones reacting to on-chain wallet activity, your edge is often timing-sensitive. If the system cannot execute safely and predictably, wallet intelligence stops being an edge and becomes expensive noise.

Manual discipline does not scale. Code does.

Set hard limits on how much the bot can lose on one trade, how much it can lose in a session, and how large it can grow any single position. The exact thresholds depend on your market, liquidity, and holding period, but the principle does not change. Loss limits should be enforced before the order is submitted, not after you notice damage on a dashboard.

For wallet-following bots, I also add signal-specific guards. If a tracked wallet buys into a thin pool with ugly slippage, the bot should skip it. If the wallet signal arrives after a delay, the bot should reject the trade rather than chase.

| Parameter | Recommended Setting | Rationale |

|---|---|---|

| Risk per trade | Small fixed share of account equity | Limits account damage from one bad entry |

| Daily loss cap | Hard trading stop after a predefined loss | Prevents revenge-by-algorithm during bad conditions |

| Max position size | Fixed ceiling based on account size and market depth | Stops oversized orders in thin books or pools |

| Stop-loss logic | Attached to every trade or enforced by exit logic | Keeps downside bounded when the market moves fast |

| Strategy shutdown rule | Disable after repeated execution failure or signal degradation | Prevents a broken or stale strategy from continuing to fire |

A laptop is fine for development and paper trading. Live capital needs infrastructure that stays up when your local machine sleeps, your internet drops, or your terminal crashes.

Use separate environments for paper and live trading. Store credentials in a secret manager or encrypted environment variables, and give the bot only the permissions it needs. Log every signal, order request, response, fill, and rejection. If your RPC, wallet intelligence feed, pricing source, or router fails, stop trading by default.

Fail-open behavior kills accounts.

On-chain bots need one more safeguard. Track the age of the signal. If your bot is acting on a wallet event that is already stale, it should do nothing. Smart money tracking works because it captures real flows before the crowd reacts. Once the market has repriced, you are no longer following informed activity. You are buying after it.

def can_trade(account_equity, planned_risk, daily_loss_limit_hit):if daily_loss_limit_hit:return Falseif planned_risk > account_equity * 0.02:return Falsereturn Truedef emergency_stop(bot_state):bot_state["trading_enabled"] = Falsereturn bot_stateThis is a minimal example, but the behavior is right. Reject the trade if it breaks risk limits. Disable trading if predefined failure conditions hit.

In production, extend that gate with execution checks such as slippage tolerance, max gas, signal age, liquidity depth, and duplicate-order prevention. Those controls are less exciting than strategy research, but they are usually what separates a bot that survives from one that blows up on a perfectly good signal.

Your bot buys within seconds of a tracked wallet. The fill is clean. The trade still loses money.

That does not mean the signal source failed. It usually means one of three things changed in production: the wallet no longer leads the market, your execution is slipping relative to test assumptions, or the bot is firing in conditions where the original edge was weak. Live monitoring exists to separate those cases quickly.

A bot that trades on on-chain wallet activity should be reviewed like a production service and a research process at the same time. PnL matters, but it is a lagging output. The first job is to inspect whether the bot is still acting on timely, high-quality wallet behavior.

Start with a dashboard that explains bot behavior, not just account balance. Track:

I also track wallet-level attribution. If three wallets generate half the trades and all the recent losses, that is the first place to investigate. Generic indicator bots often struggle to explain why they entered. Wallet-driven bots can do better if the logs preserve the full chain of cause and effect.

Long-term performance comes from reviewing edge decay before it turns into account damage.

On-chain behavior changes fast. Wallet clusters split. Funds rotate to new venues. Previously useful addresses start farming attention, trading thinner names, or exiting into copytrader flow. A bot that keeps treating every historical winner as current smart money will degrade gradually, then all at once.

Use a live review loop:

Don’t defend the bot. Audit the edge.

That point matters more with wallet intelligence than with RSI or MACD. Technical indicators are easy to recalculate, but they rarely give you a unique information advantage. The edge here comes from following the right wallets, fast enough, with enough filtering to avoid copying late or low-conviction trades. If the wallet set degrades, the strategy degrades with it.

A working bot is a maintained bot. The durable advantage is not the script. It is the operating process: finding better wallets, validating which ones still matter, measuring live execution against research assumptions, and removing signal sources as soon as they stop paying for their slot.

If you want a cleaner way to turn on-chain wallet activity into structured inputs for research or automation, Wallet Finder.ai helps you inspect wallet histories, monitor trades, and build watchlists that can feed a signal-driven workflow. It is a practical starting point when your next bot needs better inputs than generic chart indicators.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.