Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

March 12, 2026

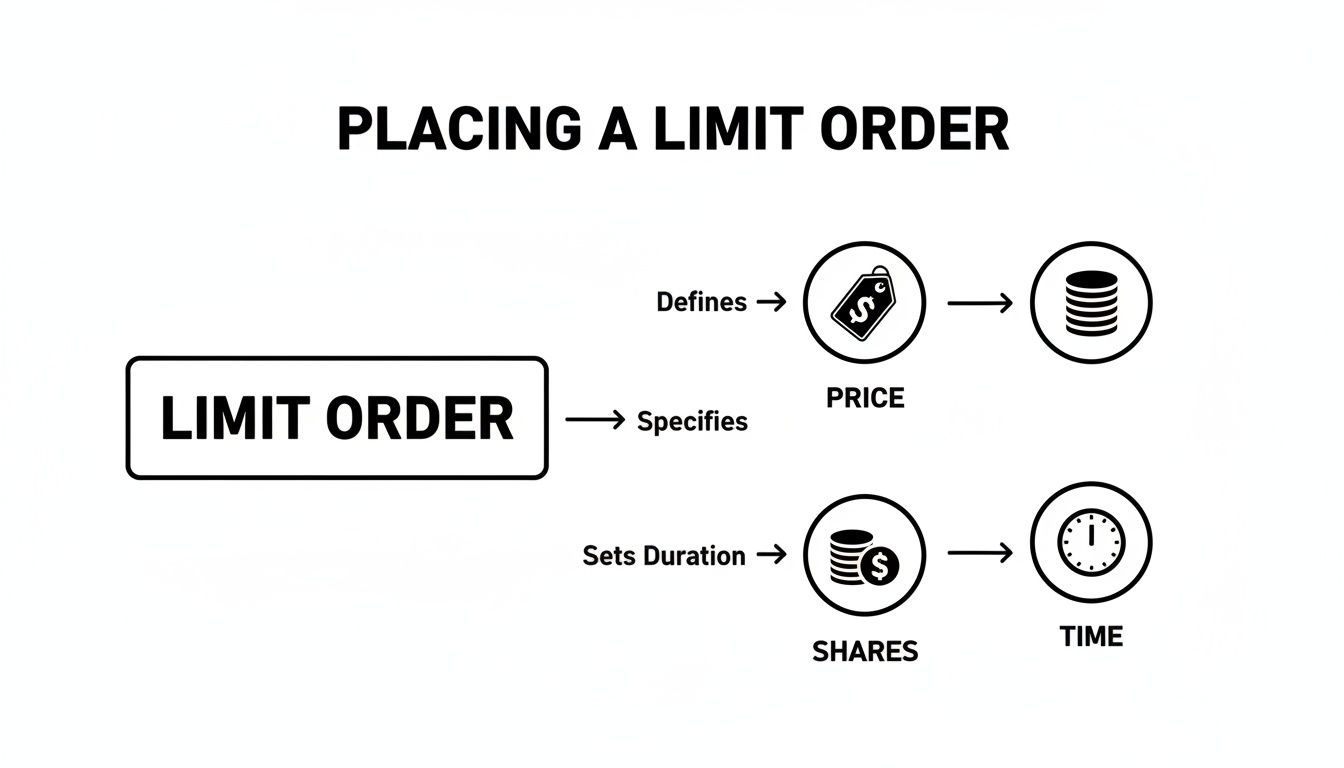

A Robinhood limit order is your secret weapon for trading with precision. It lets you name your price—the exact amount you’re willing to pay for a stock or the minimum you’ll accept to sell it. Think of it as youzzzr personal price negotiator, ensuring you never overpay or sell for less than you want.

Imagine the stock market as a massive, chaotic auction. A standard market order is like yelling, "I'll take it at whatever the current price is!" It’s fast, but you might pay more than intended, especially in a volatile market. That frustrating price difference is called slippage.

A limit order changes the game. It's a firm, non-negotiable bid. You're telling your broker, "I will only buy this stock if the price hits $50 or lower," or "I will only sell this stock if it climbs to $55 or higher." You set the terms.

Once you set a limit order on Robinhood, it doesn't execute instantly unless your price is already available. It gets added to the market's "order book"—a digital list of all buy and sell orders for that stock. Your order then waits for the market to meet your condition.

Here’s the mechanism in action:

This simple control over your entry and exit points is the foundation of strategic trading, protecting your capital from the market's whims.

When you place a limit order at a specific price, you're not just setting a condition — you're joining a queue of all other orders at that same price level. If fifty other traders have already placed limit buy orders at fifty dollars before you, and a seller arrives willing to sell at fifty dollars, those fifty orders get filled before yours even becomes eligible. Your position in this queue is determined by one simple rule: first-in, first-out.

This queue position explains why two traders can set identical limit orders at the exact same price and one gets filled while the other doesn't. The difference isn't luck or favoritism — it's timing. The trader who placed their order first gets priority. This becomes especially important at psychological price levels like whole numbers where many orders cluster.

The practical implication is that for competitive limit prices — prices very close to the current market price where many orders are likely already waiting — milliseconds matter. If you're trying to buy at fifty dollars and the stock is currently at $50.05, there are probably dozens or hundreds of buy orders already sitting at fifty dollars. Your order goes to the back of that line. If the price dips to exactly fifty dollars and only twenty shares are available at that moment, the first twenty orders in the queue get filled and everyone else, including you, continues waiting.

Your queue position isn't static throughout the day. It changes as orders ahead of you get filled or canceled. Every time someone ahead of you in the queue gets their order filled, you move up one spot. Every time someone ahead of you cancels their order, you move up. But every time someone places a new order at your price level, they go behind you in the queue, not ahead.

This creates a strategic consideration for limit orders that sit unfilled for extended periods. If you placed a buy limit order at fifty dollars first thing in the morning and it hasn't filled by mid-afternoon, you've likely moved up significantly in the queue as orders ahead of you filled or were canceled. Canceling your order and placing a new one at the same price puts you back at the end of the queue, which might actually hurt your chances of getting filled.

The exception is when you want to adjust your price. If you've been sitting at fifty dollars and you're willing to move to $50.01 to get filled faster, canceling and replacing makes sense because you're jumping to a more competitive price tier. But if you're staying at the same price, patience usually beats cancellation and replacement.

The way to optimize for queue position is understanding when speed of entry matters versus when price matters more. If you're entering a limit order for a trade you want to execute today and you're willing to be flexible on price, setting your limit at a slightly more aggressive level — a penny or two more favorable to the other side — can put you in a thinner queue or even at the front of the queue if nobody else is at that price yet.

If you're placing a longer-term GTC order where you're willing to wait days or weeks for the perfect price, queue position matters less because you have time for the market to cycle through all the orders ahead of you. In this case, setting your ideal price and letting time work for you is the better strategy.

The number one reason to use a limit order is price certainty. You eliminate the risk of overpaying or selling for a disappointing price. This is crucial when trading stocks with low trading volume or during volatile periods when prices fluctuate rapidly.

A limit order is your safety net. By setting a specific price, you guarantee that if your trade executes, it will be at your desired price—or better. Never worse.

This control separates strategic trading from reactive guessing. Let's compare it directly to a market order.

Use this table to decide which order type best fits your trading goals and the current market conditions.

FeatureLimit OrderMarket OrderPrice ControlTotal Control. You set the max buy or min sell price.No Control. Executes at the current best available price.Execution CertaintyNot Guaranteed. Fills only if your price is met.Guaranteed. Executes immediately if liquidity exists.Best ForVolatile markets, patient traders, precise entry/exit.High-volume stocks, urgent trades, when speed is paramount.Primary RiskThe order may never fill if the market moves away.Slippage; you may pay more or sell for less than expected.

Ultimately, choosing between them comes down to a trade-off: price vs. speed. For disciplined traders, the price control of a limit order is almost always the smarter choice.

Placing a Robinhood limit order is a straightforward process you can master in minutes. Whether on mobile or desktop, you can set up your trades with pinpoint accuracy.

Let's walk through the exact steps.

The Robinhood app is designed for on-the-go trading. Here’s a step-by-step guide:

Placing an order on the Robinhood website offers a larger interface to view market data.

Pro Tip: To increase the chance of a buy order filling, check the bid-ask spread. Setting your limit price slightly above the current bid can make your order more attractive to sellers, potentially speeding up execution without significantly altering your entry point.

Robinhood allows you to place and execute limit orders during extended hours — both pre-market (4:00 AM to 9:30 AM EST) and after-hours (4:00 PM to 8:00 PM EST). This feature sounds like it gives you more trading time and earlier access to news-driven moves, but the reality of how limit orders work during extended hours is dramatically different from regular trading hours in ways that create serious traps for uninformed traders.

The first major difference is that NBBO protections don't apply during extended hours. During regular trading hours, your broker is required to route your order to get you the best price available across all exchanges. During extended hours, this requirement doesn't exist. Your order gets routed to whichever venue Robinhood's order flow agreements direct it to, and that venue's price might not be the best price available in the extended hours market. You have no guarantee of optimal execution.

The second difference is liquidity. Extended hours trading volume is typically ten to twenty percent of regular hours volume or less. This thin liquidity creates much wider bid-ask spreads. A stock that trades with a one-cent spread during regular hours might have a fifty-cent spread in pre-market. If you place a limit buy order at what seems like a reasonable price based on the previous close, you might be sitting far below the actual extended hours ask price, making your order effectively invisible to sellers even though it's technically active.

The third difference is how limit orders interact with extended hours liquidity. During regular hours, market makers and algorithmic traders are actively providing liquidity, which means there's usually someone willing to trade at or near the current price. During extended hours, much of this automated liquidity disappears. Your limit order might be the best bid or offer in the entire extended hours market for that stock, but if there's no counterparty willing to trade with you, the order just sits there regardless of how competitively it's priced.

This creates a particularly frustrating scenario where you see a stock trading at fifty dollars in extended hours, you place a limit buy order at fifty dollars, and the stock continues trading at or near fifty dollars for the next thirty minutes but your order never fills. What's happening is that the trades you're seeing are happening between parties who are both active in extended hours, while your limit order is sitting in a queue that nobody is actively checking because extended hours trading is primarily done through direct routes rather than the centralized order book that operates during regular hours.

The defensive approach to extended hours limit orders is understanding that they function more like "requests for quote" than guaranteed execution mechanisms. If you're trying to trade during extended hours, the limit order strategy that works during regular hours — setting a price and waiting — often fails. Instead, you need to set your limit price within the current extended hours bid-ask spread if you want any chance of filling, which means accepting the worse pricing that extended hours naturally creates.

The better strategy for most traders is avoiding extended hours trading entirely unless you have a specific reason to accept the worse execution and higher risk. If news breaks after hours and you want to trade on it, consider setting a limit order for regular hours the next morning instead. You'll get better execution, tighter spreads, and NBBO protection. The gap between setting an extended hours order that mostly doesn't fill and waiting for regular hours is usually less than you think, and the execution quality difference is substantial.

So, you’ve submitted your Robinhood limit order. What happens next? Your order enters a high-speed, regulated system designed to find you the best possible price.

First, your order is routed to market makers—large trading firms that provide liquidity to the market. They compete to fill your trade while honoring the National Best Bid and Offer (NBBO). This SEC rule ensures your trade executes at the best available price across all U.S. exchanges. It's why you sometimes get "price improvement"—if a better price appears while your order is processing, you get that better deal.

How does Robinhood offer commission-free trading? Through a common practice called Payment for Order Flow (PFOF).

Here's the breakdown: Robinhood sends your order to market makers, who pay Robinhood a fraction of a cent for the right to execute it. The market maker profits from the tiny "bid-ask spread." It all happens in milliseconds.

This diagram shows the key information you provide that instructs the market makers.

When you set your price, shares, and duration, you're giving the system crystal-clear instructions.

Limit orders are highly valuable in this model because they provide specific, actionable data for firms like Citadel Securities, which handles a significant portion of Robinhood's order flow.

PFOF from retail orders accounted for over 70% of Robinhood's total revenue in 2021, highlighting its importance. For you, the trader, this system means your well-placed limit order has a very high chance—often over 95%—of being filled at or better than the best market price. To learn more, you can explore the mechanics of Robinhood's order flow.

The key takeaway is simple: a limit order doesn't just protect you. It instructs the entire market system on your exact terms, ensuring that if your trade executes, it will be at your specified price or an even better one, thanks to the NBBO.

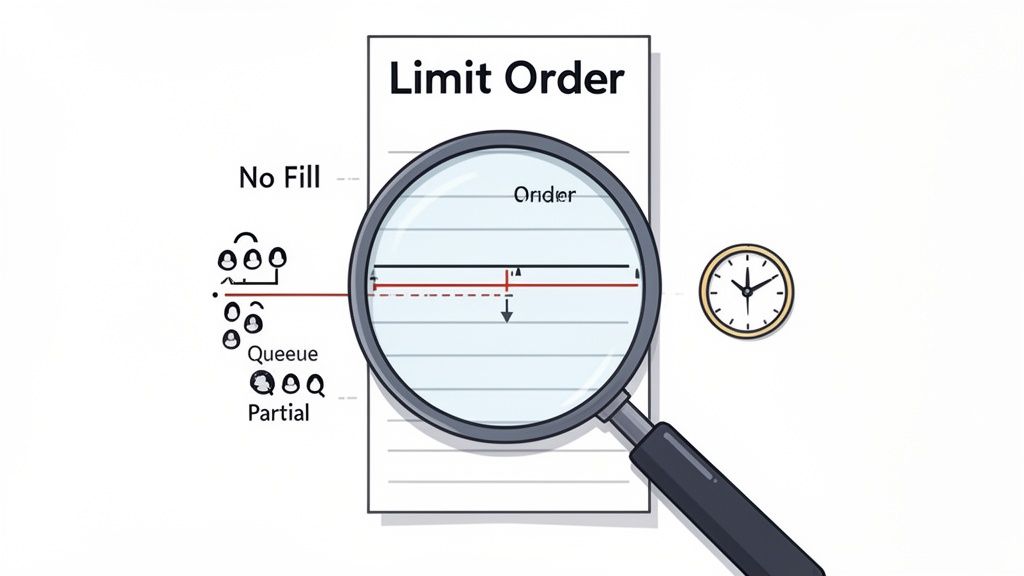

It’s frustrating: you set a perfect Robinhood limit order, but it just sits there, unfilled, as the opportunity vanishes. This isn't a glitch; it's the market signaling that your conditions haven't been met.

Let's break down the common reasons why and what you can do.

ReasonWhy It HappensActionable SolutionPrice Never Reached Your LimitThe most common cause. The market price must touch or pass your limit price for the order to become eligible to fill.Re-evaluate your price. If your analysis has changed, consider adjusting your limit price closer to the current market.Low Liquidity (Trading Volume)Even if the price is met, there may not be enough buyers or sellers available to complete your trade, common in thinly traded stocks.Check the stock's average daily volume. If it's low, be prepared for slower fills or consider trading more liquid assets.You Are Behind in the QueueOrders at the same price are filled on a "first-in, first-out" basis. If many orders were placed before yours, they get priority.To get ahead, you can cancel and replace your order with a slightly more competitive price (e.g., a penny higher for a buy).Partial Fills OccurredYour order was partially filled, but not enough shares were available at your price to complete it. The remainder of your order stays active.Decide if you want to wait for the rest to fill, cancel the remaining portion, or adjust the price to secure the shares.

Think of your limit price as a hard line in the sand. The market doesn’t care if it gets close; if your price isn't met or beaten, the order stays pending.

Understanding concepts like cumulative volume delta can also provide insight into whether buyers or sellers are in control, which directly impacts order flow and the likelihood of your order filling.

When your limit order is large relative to the available liquidity at your price level, it often gets filled in pieces rather than all at once. You might place an order for five hundred shares and get filled in chunks: two hundred shares in one execution, one hundred in another, fifty in a third, and so on until the full order is complete. Each of these is a separate "fill" even though they're all part of the same order, and this fragmentation creates hidden costs that accumulate across multiple small fills.

The first cost is regulatory fees, which are calculated on a per-transaction basis. The SEC fee and FINRA Trading Activity Fee apply to each separate execution. When your five hundred share order fills as one complete transaction, you pay these fees once. When it fills as five separate executions, you pay them five times. The individual fees are tiny — fractions of a cent per share — but they add up over hundreds of trades, and they're higher for fragmented fills than complete fills of the same total size.

The second cost is less visible but potentially larger: price drift during partial fills. When your order starts filling, the market is at one price level. If your order takes thirty seconds to completely fill through multiple executions, the price might drift against you during that time. Your first two hundred shares might fill at exactly your limit price, but by the time the final fifty shares fill, the price might have moved a cent or two, and you'll get that last portion at a slightly worse price even though the whole order was technically "at limit."

Partial fills occur because of how the order matching system works. If you place a limit buy order for five hundred shares at fifty dollars and only two hundred shares are available at that price from sellers, you get filled for two hundred and the remaining three hundred shares of your order continue waiting. If another one hundred shares become available at fifty dollars a minute later, you get filled for that hundred. The process repeats until your entire order is complete or you cancel it.

The likelihood of fragmentation is directly related to your order size relative to typical lot sizes at your price level. If you're ordering five hundred shares of a highly liquid stock where the typical order size is thousands of shares, you'll likely get filled all at once. If you're ordering five hundred shares of a thinly traded stock where typical orders are fifty to one hundred shares, you'll almost certainly experience multiple partial fills.

The strategy for minimizing fragmentation costs depends on the stock's liquidity and your urgency. For highly liquid stocks, this isn't a concern — your order will fill in one or two executions regardless of size. For less liquid stocks, you have two options.

The first is breaking your order into smaller intentional pieces and placing them as separate orders over time rather than one large order that fragments uncontrollably. If you want five hundred shares total, place five orders of one hundred shares each at slightly different limit prices or at different times. This gives you control over the spacing and timing rather than leaving it to the random availability of counterparties at your price.

The second option is accepting that your large order will fragment and building the regulatory fees into your cost basis calculation. If you know a five hundred share order in a thinly traded stock will generate five to ten separate fills, factor an extra cent or two per share into your expected cost to account for fees and price drift. This doesn't prevent fragmentation but it keeps your expectations realistic.

Once you master the basics, a Robinhood limit order becomes a powerful strategic tool. These advanced techniques help you automate decisions and improve your average entry and exit prices.

Level II market data provides a look into the "order book"—a live list of all buy (bid) and sell (ask) limit orders at various price levels. This is a game-changer for setting effective limits.

Thanks to Nasdaq TotalView, Robinhood provides this powerful data to its users. By analyzing this data, you can spot:

Actionable Tip: Place your buy limit order just above a strong support level or your sell limit order just below a heavy resistance level to dramatically increase the probability of your order getting filled.

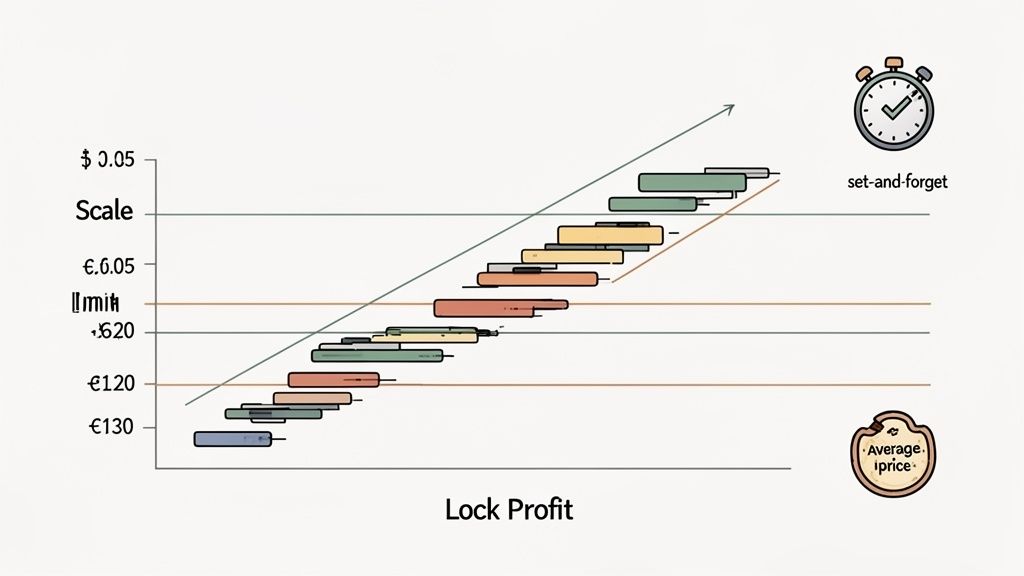

Instead of executing one large trade, "scaling" involves breaking your trade into smaller pieces using multiple limit orders at different price points.

Scaling is the art of averaging. By spreading out your orders, you can achieve a much better average price, reducing the risk of a single poorly timed entry or exit.

Example: Scaling into a Position

You want to buy 100 shares of a stock currently trading around $52. Instead of one large order, you could set:

If the stock dips, your orders begin to fill, giving you a better average cost. To refine your price levels, consider using technical buy and sell indicators.

Use "Good-til-Canceled" (GTC) limit orders to put your trading plan on autopilot. This removes emotion and enforces discipline.

A small mistake with a Robinhood limit order can lead to a missed opportunity or an unwanted trade. Here are the most common pitfalls to avoid.

When a stock undergoes a split, Robinhood automatically adjusts your pending limit orders to reflect the new share price and quantity. For example, if you have a limit order to buy 10 shares at $100 and the stock does a 2-for-1 split, your order is automatically adjusted to buy 20 shares at $50. The total dollar value of your order stays the same.

However, it's still smart to review your orders after any corporate action. In rare cases, especially with reverse splits or more complex scenarios, you may want to cancel and replace the order to ensure it still matches your trading strategy at the new price levels.

Yes, absolutely. You can have multiple active limit orders for the same stock at different price levels. This is actually the foundation of the "scaling" strategy discussed earlier in this guide.

For example, you might set three separate buy limit orders at $50, $48, and $45 to scale into a position as the price drops. Or you might set multiple sell limit orders at $55, $60, and $65 to scale out of a position as the price rises. Each order is independent and will execute if and when its specific price condition is met.

Just remember that each order ties up buying power (for buy orders) or shares (for sell orders), so make sure you have sufficient capital or shares available to cover all your pending orders if they were to fill simultaneously.

Ready to find trading opportunities before the crowd does? Wallet Finder.ai helps you track the moves of top-performing traders on the blockchain in real time. Discover winning wallets, copy their trades, and get instant alerts so you never miss a beat. Start your free trial at https://www.walletfinder.ai.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.