Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

February 15, 2026

Getting cash from your Robinhood account to your bank is simple. You have two main options: a standard ACH transfer, which is free but takes a few days, or an Instant Transfer, which costs a small fee but gets your money to you in about 30 minutes.

The most critical step is ensuring your cash is fully settled. This is the most common hurdle for users, so understanding it is key to a smooth process.

Everyone knows about the T+2 settlement rule. Sell a stock Monday, wait until Wednesday to withdraw. Simple, right? Except there's a hidden layer of complexity that catches traders off guard and locks up their capital when they need it most.

The issue isn't just when funds settle—it's which funds settle first and how that affects your withdrawal ability. Robinhood uses a FIFO (First In, First Out) system for determining what cash is available. This creates scenarios where you think you have withdrawable cash, but the platform tells you otherwise.

Here's a real scenario that happens daily: You have $10,000 in your account on Monday. You buy and sell different stocks throughout the week, keeping roughly the same cash balance. By Friday, you still show $10,000 in cash. You try to withdraw $8,000. Robinhood says you can only withdraw $2,000. What happened?

The answer is settlement stacking. Each trade you made has its own T+2 settlement timeline. Monday's trades settle Wednesday. Tuesday's settle Thursday. Wednesday's settle Friday. By Friday afternoon, only Monday and Tuesday's trades have fully settled. Everything else is still in the settlement pipeline.

Robinhood doesn't let you withdraw cash that's tied up in unsettled trades, even if your total cash balance looks fine. This is how you can have $10,000 showing but only $2,000 withdrawable.

The solution: track your settlement calendar manually if you're an active trader. Before initiating any withdrawal, calculate which trades have actually cleared T+2. Don't trust the total cash balance—only trust the "withdrawable cash" figure shown on the transfer screen.

If you're flagged as a pattern day trader (4+ day trades in 5 business days), you're required to maintain a $25,000 minimum account balance. What most traders don't realize is that this minimum applies to withdrawals too.

You can't withdraw funds that would drop your account below $25,000 while you have open positions. Even if all your cash is settled, even if you're trying to withdraw your own money you deposited years ago, Robinhood will block it if it violates the PDT minimum.

The workaround: close all positions first, then withdraw. Once you have zero open trades, the PDT minimum doesn't apply to withdrawals. You could drop to $5,000 and still pull the money out—as long as you're not holding any stocks at the time.

But here's the catch: if you close positions just to withdraw funds, you'll trigger wash sale rules if you rebuy those same stocks within 30 days. Any loss you took on the sale gets disallowed for tax purposes. You've just turned a tax deduction into taxable income.

This one destroys beginners. You deposit $1,000 on Monday via ACH. Robinhood gives you instant buying power, so you immediately buy stocks. Tuesday morning, you sell those stocks for $1,100. You made profit! Now you try to withdraw the $1,100. Denied.

Why? You bought stocks with unsettled deposit money (your Monday ACH hasn't cleared yet). Then you sold those stocks before the deposit settled. This is called a good faith violation. You're essentially trying to withdraw money you never actually deposited yet because ACH takes 5 business days to fully clear.

Three good faith violations in 12 months gets your account restricted to settled cash only for 90 days. No more instant buying power. No more day trading. You're basically trading with one hand tied behind your back.

The prevention is simple but annoying: never sell a position until your deposit that funded it has fully settled (5 business days). If you deposited $1,000 Monday, don't sell anything you bought with that money until the following Monday.

Before you can withdraw money, you need to know the difference between settled and unsettled funds. Just because you see cash in your account doesn't mean it's ready to move.

Understanding this rule prevents most transfer issues. Robinhood manages a massive volume of transactions—net deposits reached $7.1 billion in a single month at one point—so these settlement rules are crucial for operational integrity.

Robinhood says 1-3 business days for ACH transfers. In reality, many users report 4-6 days. The discrepancy isn't Robinhood lying—it's how the banking system actually works versus how it's marketed.

When you initiate a withdrawal Tuesday at 2pm, here's what actually happens behind the scenes:

Day 1 (Tuesday 2pm): You click "transfer." Robinhood queues your request.

Day 1 (Tuesday 8pm ET): Robinhood batches your transfer with thousands of others and submits to the Federal Reserve's ACH network.

Day 2 (Wednesday): Federal Reserve processes the batch and forwards to your bank. Your bank receives notification but doesn't credit your account yet.

Day 3 (Thursday): Your bank verifies the transfer, checks for fraud flags, and processes it internally. Still no money in your account.

Day 4 (Friday morning): Your bank finally posts the deposit to your account. The cash appears in your available balance.

That's 3 full business days after initiation, landing Friday morning. But if you initiated Tuesday evening instead of afternoon, Robinhood's 8pm batch already passed. Your transfer doesn't enter the queue until Wednesday 8pm, pushing everything back 24 hours. Now you're looking at Monday arrival.

Weekend in the middle? Add two more days. Initiated Friday at 3pm? You're not seeing that money until Thursday at the earliest.

Not all banks process ACH deposits at the same speed. Some credit your account as soon as they receive the notification (Day 2). Others hold it for "verification" until Day 4 or even Day 5.

Banks known for fast ACH: Ally Bank, Chime, SoFi, Marcus by Goldman Sachs. These usually credit within 2 business days.

Banks notorious for slow ACH: Wells Fargo, Bank of America, Chase (sometimes). These can take the full 5 business days.

Credit unions are wildly inconsistent. Some are faster than big banks. Others take a week. The only way to know is testing it yourself with a small transfer first.

Here's a scenario that ruins people: You deposit $5,000 into Robinhood via ACH. Robinhood gives you instant buying power. You buy stocks. You sell them two days later for $5,500. Your ACH deposit still hasn't fully cleared (remember, ACH takes 5 business days). Your original bank reverses the ACH deposit for insufficient funds or fraud suspicion.

Now Robinhood is out $5,000 they advanced you. Your account goes negative. Robinhood sells whatever positions you still have to cover the deficit. If you've already withdrawn some of that $5,500 profit, they'll freeze your account until you repay the negative balance.

This happens more than you'd think. Your bank might reverse an ACH for:

The protection: never trade with money from a pending ACH deposit until it fully settles. I know Robinhood gives you instant buying power. Don't use it for anything you plan to sell quickly. Only use it for long-term holds where you're confident your deposit will clear.

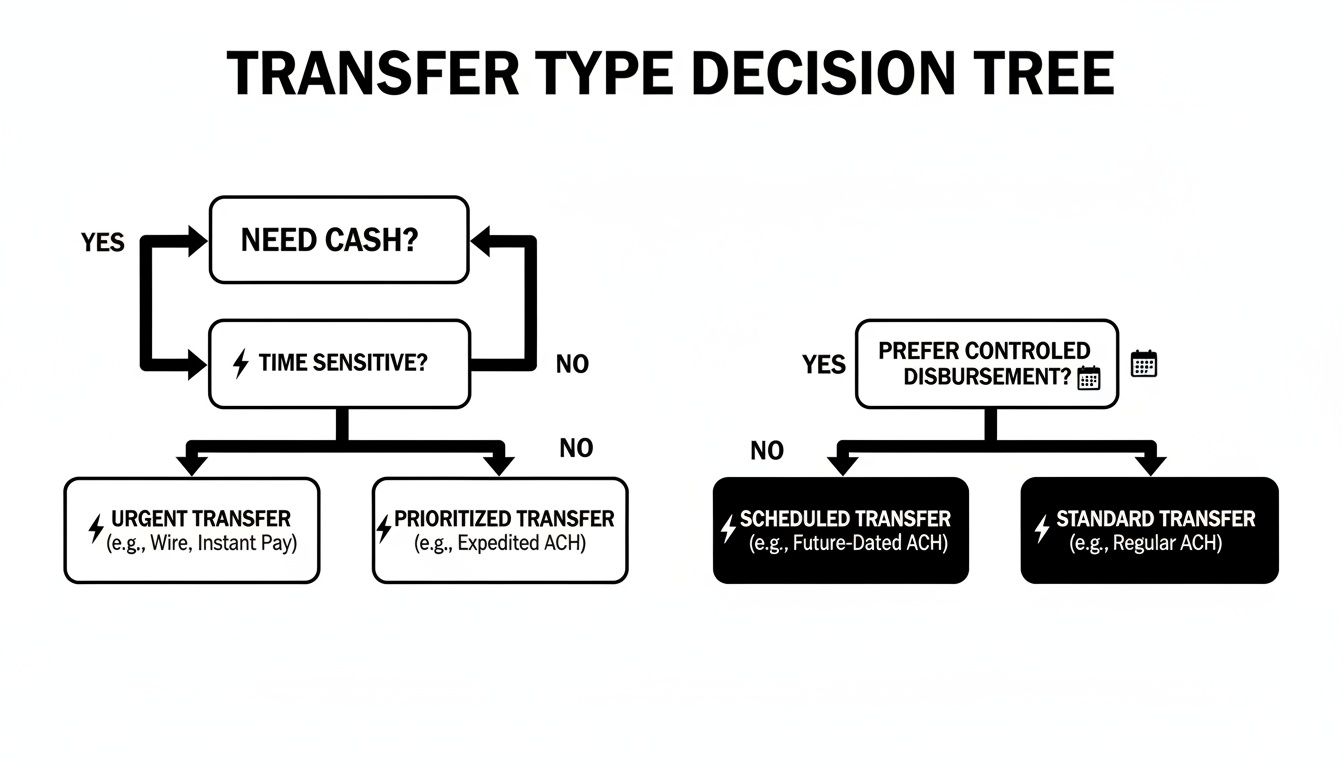

Once your funds are settled, choose the transfer method that fits your needs. Do you need the money immediately, or can you wait to avoid fees?

FeatureStandard ACH TransferInstant TransferSpeed1-3 business daysWithin 30 minutesCostFree1.75% fee (min $0.25)Best ForNon-urgent needs, fee-conscious usersUrgent cash needs, convenience

This decision tree gives you a simple visual for picking the right method based on your situation.

If you need funds immediately, the Instant Transfer fee is likely worth it. Otherwise, the free standard ACH transfer is the practical choice. The core concepts are similar across platforms, though specifics can differ—for comparison, see our guide on how to cash out of Coinbase.

The best strategy is to plan ahead. If you anticipate needing cash, sell your assets a few days early so the funds are settled when you're ready to initiate the transfer.

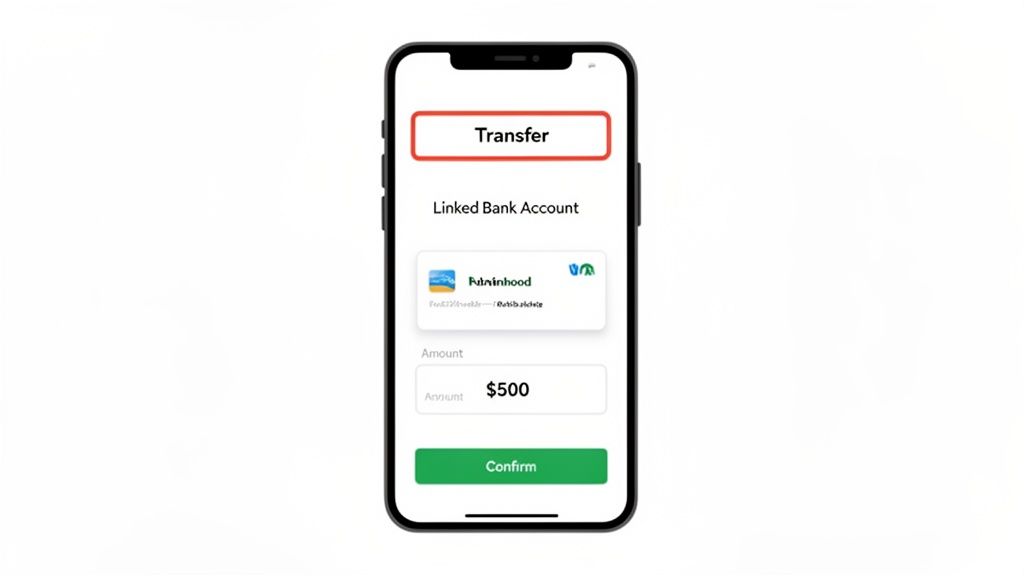

Alright, you've confirmed your funds are settled and chosen your transfer type. Now for the easy part: actually moving the money.

Getting your cash out of Robinhood is straightforward. Here is a screen-by-screen walkthrough to guide you.

The final step is the review page, your last chance to check everything before the transfer begins.

This screen is your final checkpoint. Is the amount correct? Is it going to the right bank account?

I can't stress this enough: always pause and double-check the review screen. Confirming the bank account and the dollar amount is a simple habit that can save you from a massive headache, especially with larger transfers. An extra five seconds of review beats days of trying to sort out a mistake.

Once you’ve verified the details, tap the final "Transfer" button. You will receive a confirmation from Robinhood, and your cash will be on its way.

When moving money, two questions are paramount: how long will it take, and what will it cost? The answers depend on the withdrawal method you select.

Most users opt for the standard ACH transfer. It’s completely free, but it requires patience. Expect your funds to arrive in your bank account within 1 to 3 business days.

Remember, this timeline excludes weekends and bank holidays. A withdrawal initiated on a Friday afternoon might not appear in your account until the following Tuesday or Wednesday.

What if you need the money now? That’s where Instant Transfers are useful.

For a small fee, you can get your funds sent to an eligible debit card or bank account, usually within 30 minutes. I've found this is a lifesaver for covering an unexpected bill or jumping on an opportunity outside of Robinhood.

The convenience comes at a cost: a 1.75% fee on the transfer amount (with a $0.25 minimum). This fee is deducted from the withdrawal. For example, if you withdraw $1,000 instantly, Robinhood deducts a $17.50 fee, and $982.50 arrives in your bank account.

You must also be aware of Robinhood's withdrawal limits, which are in place for security and regulatory reasons.

This table provides a clear breakdown of the limits and costs for each withdrawal method.

Transfer TypePer-Transaction LimitDaily LimitAssociated FeeStandard ACH$50,000$50,000NoneInstant Transfer$5,000$5,0001.75% (Min $0.25)

Knowing these rules helps you manage your money effectively, allowing you to balance speed and cost according to your needs.

Even with a straightforward process, issues can arise. Seeing a transfer get stuck or fail is stressful, but the solutions are usually simple.

The most common reason for a delayed Robinhood transfer to bank is attempting to move unsettled funds. Remember the T+2 rule: cash from a stock sale needs two full business days after the trade to become withdrawable.

Most guides tell you how to withdraw from Robinhood. Almost none tell you when you should withdraw for maximum tax efficiency. This timing can save or cost you thousands of dollars.

Every dollar you withdraw from Robinhood in a given calendar year affects your taxes for that year. If you sell stocks at a profit and withdraw the proceeds, you owe capital gains tax on that profit when you file in April.

But here's what most traders miss: you have control over which tax year bears that burden.

Scenario 1: You sell $100,000 of profitable stock positions December 20th, 2026. You withdraw the money December 28th, 2026. You owe capital gains tax on that $100K when you file in April 2027.

Scenario 2: Same sale December 20th, 2026. But you wait and withdraw January 5th, 2027. You still owe the same capital gains tax in April 2027 (because the sale happened in 2026).

Scenario 3: You wait to sell until January 5th, 2027. You owe capital gains tax when you file in April 2028—giving you an extra 12 months before the tax bill comes due.

The lesson: if you're near year-end and don't urgently need the cash, waiting until January to sell and withdraw can defer your tax bill by a full year. That's 12 extra months to keep that money invested or earning interest instead of paying it to the IRS.

December is tax-loss harvesting season. If you're sitting on losing positions, selling them before December 31st lets you deduct those losses against your gains.

Real example: You made $50,000 in realized gains this year from profitable trades. You're also holding a stock position that's down $15,000 from your purchase price. If you sell that loser before December 31st, you can offset the gains.

Tax owed on $50,000 gain at 15% long-term rate: $7,500Tax owed on $35,000 net gain (after $15,000 loss): $5,250

You just saved $2,250 by selling one losing position strategically before year-end. Then you can rebuy that same stock in January if you want—just wait 30 days to avoid the wash sale rule.

Most traders ignore this entirely and wonder why their tax bill is so high. The wealthy do this religiously every December.

If you're making serious money on Robinhood (over $10,000 in capital gains per year), you're technically supposed to pay quarterly estimated taxes. Most retail traders ignore this because they don't know about it.

The IRS penalty for underpayment of estimated taxes is roughly 0.5% per month on the underpaid amount. If you owe $10,000 in capital gains tax from Q1 trading but don't pay it until April next year, you'll owe about $600 in penalties.

The strategic withdrawal timing: if you have a massive gain in January, withdraw enough to cover the estimated tax payment by April 15th (Q1 deadline). Don't wait until December to withdraw everything and get hit with underpayment penalties for the whole year.

Or better yet, use the standard ACH transfer to move money to a high-yield savings account throughout the year. Keep that tax money liquid and earning 4-5% interest until you have to pay it.

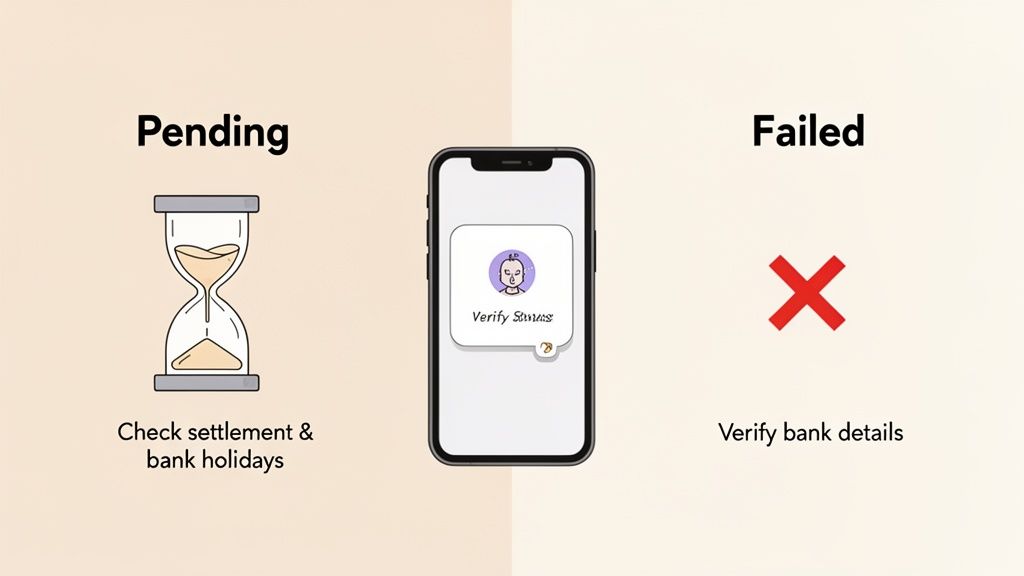

If your transfer is stuck on "Pending" for longer than the estimated 1-3 business days, don't panic. The delay is often due to weekends and bank holidays, which do not count as processing days.

Always check your timeline against business days, not calendar days. The banking system essentially pauses over the weekend, so a transfer that feels like it’s taking five days might only be on its second business day of processing.

If you've accounted for non-business days and the transfer is still pending, the next step is to verify that your linked bank account information is correct.

A "Failed Transfer" notification means the process was stopped and canceled. Before contacting support, run through this quick diagnostic checklist to identify the problem.

By reviewing these points, you can often solve the issue yourself. If the problem persists after checking everything, it’s time to contact Robinhood's support team with the specific details.

When moving money, your financial security is the top priority. Follow these best practices to ensure your funds are protected.

The single most effective action you can take is to enable Two-Factor Authentication (2FA). This is non-negotiable. 2FA adds a critical layer of security by requiring a unique, time-sensitive code from your phone at login. Even if a scammer steals your password, they cannot access your account without this code. For a complete walkthrough, see our guide on setting up a Robinhood authenticator app.

Beyond technical safeguards, smart habits are your best defense. Before confirming any withdrawal, run through this simple mental checklist:

A simple five-second review before confirming a transfer is one of the best habits you can build. It costs nothing and can prevent a costly mistake, saving you from the stress of trying to recover misplaced funds.

These practices are not complicated, but they are essential for protecting your hard-earned capital.

Yes, significantly. Robinhood Gold ($5/month) gives you instant settlement on stock sales. Normally when you sell a stock, the T+2 rule applies—your cash isn't available for withdrawal for two business days. With Gold, the moment you sell a stock, the cash is immediately available to withdraw (up to your Instant Deposit limit, usually $1,000-$50,000 depending on account history).

This is a massive advantage for active traders who need quick access to their capital. Without Gold, selling a stock Monday means waiting until Wednesday to withdraw. With Gold, you can sell Monday morning and initiate an instant transfer to your bank within minutes, getting cash in your account 30 minutes later.

However, instant settlement only applies to stocks and ETFs. Options still follow the T+1 rule (one business day), and crypto follows different settlement rules entirely. Gold also doesn't bypass the good faith violation rules—you still can't sell stocks bought with unsettled deposit funds without consequences.

Is it worth $5/month? If you actively trade and frequently move money in and out of Robinhood, absolutely. If you're buy-and-hold and rarely withdraw, probably not.

No. Robinhood requires that all withdrawals go to a bank account in your name. This is a security and regulatory requirement to prevent money laundering and fraud.

If you need to send money to someone else, you have to: withdraw to your own bank account first (1-3 business days), then use your bank's transfer service, Venmo, PayPal, or Zelle to send to the other person.

The only exception is joint accounts. If you have a joint checking account with someone, you might be able to link that joint account to your Robinhood and withdraw to it. But Robinhood will require both account holders' information and may restrict this depending on their current policies.

Some traders try to get around this by selling their stocks, withdrawing to crypto, then sending that crypto to someone else's wallet. While technically possible, this creates a taxable event (the stock sale), incurs crypto network fees, and is reportable to the IRS. It's not a workaround—it's a tax nightmare.

This depends entirely on whether your deposit has fully settled. If you deposit $1,000 via ACH Monday and try to withdraw that same $1,000 Tuesday, Robinhood will likely block it because the deposit hasn't cleared yet (ACH takes 5 business days).

However, if you deposit $1,000 Monday, wait 6 business days, then withdraw it without ever trading, that should work fine. The catch is if you used that $1,000 to buy stocks, sold them, and now want to withdraw the proceeds before the original deposit settled—that's a good faith violation.

Pattern matters too. If you consistently deposit and withdraw similar amounts (like depositing $5,000 every Monday and withdrawing $5,000 every Friday), Robinhood's fraud detection might flag this as suspicious "structuring" behavior. Banks hate this pattern because it looks like money laundering. You could get your account restricted and investigated.

The safest approach: treat deposits and withdrawals as separate actions separated by at least a week. Deposit when you have new capital to invest. Withdraw when you're taking profits or need the money for life expenses. Don't create patterns that look like you're cycling money for no investment purpose.

This frustrates people daily. You see $5,000 in your cash balance but Robinhood says you only have $500 withdrawable. There are several possible reasons:

Unsettled trades: Your most recent stock sales haven't passed the T+2 settlement period yet. That cash exists but isn't available.

Pending deposits: You deposited money via ACH recently. Robinhood gave you instant buying power but the underlying deposit hasn't cleared. You can trade with it but not withdraw it.

Margin loan: If you have Robinhood Gold and used margin (borrowed money) to buy stocks, your cash balance might be negative underneath. What shows as "cash" is actually loan collateral.

Options spreads: If you sold options spreads, Robinhood holds cash as collateral until the options expire or you close the position. That cash is locked.

Dividend pending: A dividend was declared but hasn't paid out yet. Shows in your balance but isn't liquid.

The definitive answer is in Transfers → Transfer to Your Bank. The number shown there as "withdrawable cash" is the only number that matters. Everything else is accounting.

Robinhood's standard ACH limit is $50,000 per business day. For amounts over that, you have three options:

Option 1: Split across multiple daysWithdraw $50,000 today, $50,000 tomorrow, etc. This works but takes time. For a $200,000 withdrawal, you'd need 4 business days.

Option 2: Use a wire transferRobinhood supports outbound wire transfers for $25. Wires can handle unlimited amounts and typically complete within 1 business day. The downside is the fee and the fact that some banks charge receiving fees ($15-30) on incoming wires.

Option 3: ACATS transferInstead of withdrawing cash, transfer your entire Robinhood account to another brokerage via ACATS (Automated Customer Account Transfer Service). This moves your stocks directly without selling them. Robinhood charges $100 for outbound ACATS transfers, but many receiving brokerages (like Fidelity, Schwab) will reimburse this fee if you're bringing over significant assets. This avoids creating a taxable event from selling everything.

For amounts over $100,000, I'd recommend Option 3 or a combination of Options 1 and 2. Wire the maximum you need immediately, then do daily $50K ACH transfers for the rest. This minimizes fees while getting you access to capital quickly.

Yes, and it happens. Robinhood can place a hold on your account for several reasons, blocking all withdrawals until resolved:

Security review: Unusual account activity, like logging in from a new device or location, can trigger an automatic security hold.

Fraud investigation: If Robinhood suspects fraud (either against you or by you), they'll freeze the account pending investigation.

Regulatory compliance: If you're under investigation by FINRA or the SEC, Robinhood may be legally required to freeze your account.

Negative balance: If your account went negative due to an ACH reversal or margin call, withdrawals are blocked until you deposit funds to cover it.

Pattern day trading violation: If you violated PDT rules on a margin account, your account can get restricted to closing transactions only for 90 days, preventing new withdrawals.

The frustrating part is Robinhood often doesn't explain why in real-time. You'll see a generic message like "Your withdrawal can't be completed" with instructions to contact support. Support responses can take 1-5 business days, during which your money is trapped.

Prevention: enable two-factor authentication, don't use public WiFi for trading, maintain your account in good standing (no margin violations), and keep detailed records of all deposits/trades in case you need to prove legitimacy to support.

If you need your funds immediately, you can choose an Instant Transfer. This option sends money to your linked debit card, typically within 30 minutes, but it includes a 1.75% fee.

At Wallet Finder.ai, we turn complex on-chain data into clear, actionable signals. Discover profitable wallets, track smart money movements, and mirror winning DeFi strategies in real time with our powerful analytics platform. Start your 7-day trial and trade ahead of the market at https://www.walletfinder.ai.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.