Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

July 11, 2026

You close a trade green, check your wallet, and the result looks worse than the chart suggested. The swap worked. The thesis was right. But the net outcome got shaved by gas, approvals, a bridge hop, maybe a withdrawal, and sometimes a rushed fee preset that cost more than it needed to.

That gap is where a lot of copy traders leak PnL.

When people talk about alpha, they usually mean token selection, timing, or wallet discovery. In practice, wallet fees sit in the middle of all three. If you mirror an active wallet without understanding how it moves capital, what chain it prefers, and how often it pays to reposition, you can copy the idea and still miss the result.

You mirror a wallet that called the move right. The token runs, the exit looks clean, and the lead trader books a solid gain. Your copy, however, lands much lower after approvals, gas spikes, a bridge transfer, and a sell executed with default settings. The trade idea was profitable. Your fee stack changed the result.

That gap matters because copy-trading PnL is path-dependent. The same wallet can produce very different net returns depending on your chain, position size, execution timing, and how often you need to move capital. Fees are not background noise. They are a direct input into breakeven.

In mainstream payments, those costs are often buried inside pricing. In crypto, they are exposed transaction by transaction. Finder's digital wallet statistics reported that digital wallets reached 4.3 billion global users in 2024, equal to 53% of the world's population, and accounted for 53% of global e-commerce transactions that year. On-chain, that cost transparency cuts both ways. You can see the leak, but you still have to control it.

Wallet fees usually hit active traders before, during, and after the trade:

Small positions feel this first. A $40 fee bill on a large swing trade may be noise. On a smaller copy trade, it can erase the edge entirely.

This gets sharper when you follow high-turnover wallets. A trader rotating size on a cheap chain can survive a style that would be untradeable for a follower using smaller clips, bridging in from another network, and paying priority fees on every action. Same entries. Different net outcome.

Many popular copy-trading dashboards rank wallets by realized returns, win rate, or recent momentum. Useful metrics, but incomplete. They do not show whether those returns came from disciplined execution or from a market strong enough to cover waste.

Fee efficiency is a real signal. A wallet that avoids unnecessary approvals, bridges less often, trades where blockspace is cheaper, and sizes positions so fees stay small relative to expected upside will hold onto more gross alpha. That matters even more in flat or choppy conditions, where the spread between gross and net performance decides whether a strategy still works.

This is also where on-chain analysis becomes practical, not academic. You can inspect a wallet's transaction history and ask better questions: How often does it bridge? Does it cluster trades to reduce overhead? Does it chase congested periods or wait for better execution windows? Does it route through expensive contract paths for marginal gains? Traders who manage these details tend to keep more of what they make, and they are usually better copy-trading candidates than a flashy wallet with weak fee discipline.

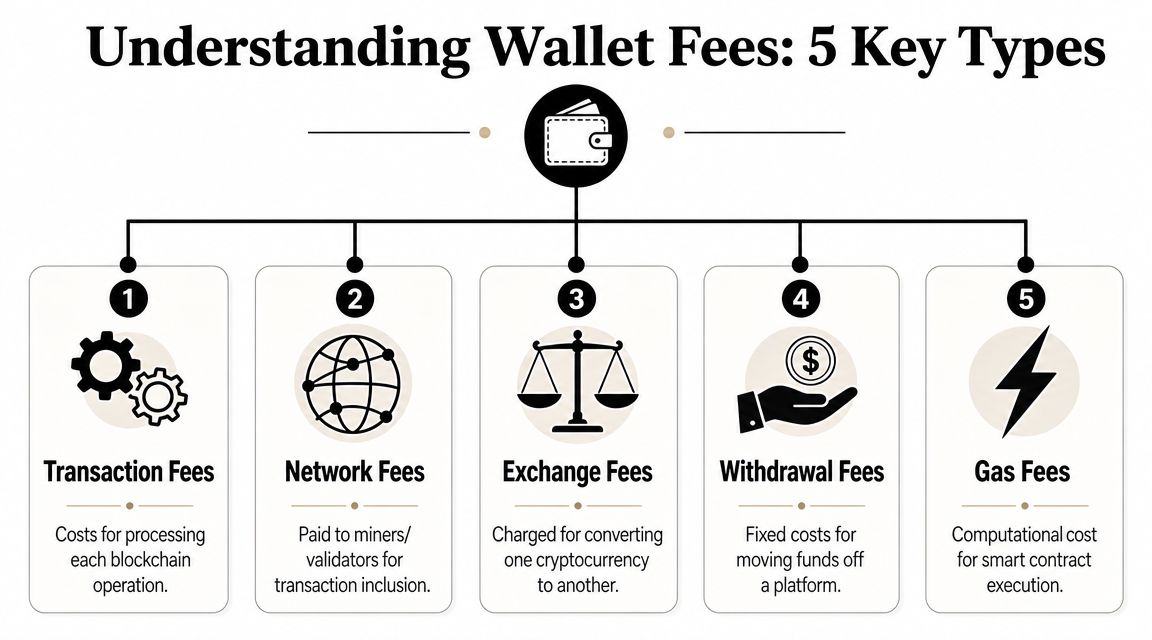

If you can't label the fee, you can't control it. Most trading costs fall into five buckets.

Think of this as the highway toll. You pay the chain to include your transaction.

On Bitcoin, the fee is tied to blockspace demand. On smart contract chains, gas also reflects how much computation your action needs. A simple transfer costs less than a contract interaction, and a contract interaction usually costs less than a multi-step route through an aggregator.

These fees don't go to your wallet provider. They go to the network participants who include or validate the transaction.

This is the service charge layer. Some platforms add fees for buying, selling, converting, or withdrawing assets. Custodial apps often package convenience into the spread or into explicit transaction charges.

A self-custody wallet may not charge for holding assets, but the moment you use built-in swap rails, fiat onramps, or staking modules, a provider fee may appear in the route. Traders miss this because they assume “wallet fee” only means gas.

This is the valet service version of execution. You sign an intent, and another party submits the transaction on your behalf.

Sometimes the user sees no direct gas payment because a sponsor or relayer covers it. That doesn't mean the transaction is free. The cost may be embedded in the swap rate, deducted elsewhere, or paid by a protocol for strategic reasons. The user experience is smoother, but the economics still exist.

This is the currency exchange counter of on-chain trading. When you move funds across networks or route through liquidity pools, you may pay bridge fees, liquidity provider fees, or both.

These are easy to ignore because they often appear as route outputs rather than line-item charges. But for copy traders, they matter a lot. A wallet that hops chains often may still be profitable, yet the follower who bridges separately and later can end up with a worse basis.

This is the permit to spend. Many tokens require an approval transaction before a dApp can access them.

That approval is often a standalone on-chain action. It can be cheap or annoying depending on the chain, but it still counts. New traders often evaluate only the swap cost and forget the approval cost, especially when they rotate into a token for the first time.

A “cheap swap” can still be an expensive trade if it requires a fresh approval, a bridge, and a rushed confirmation.

Everything covered above is on-chain cost. If any part of your workflow touches a centralized exchange wallet before or after a trade, that adds a completely separate fee layer worth understanding on its own terms.

Most exchanges charge maker and taker fees, lower for limit orders that add liquidity to the order book, higher for market orders that fill immediately against it. Base rates vary widely across platforms, often somewhere between 0.02% and 0.6% depending on the exchange and your account tier, with high-volume traders unlocking meaningfully lower rates through tiered discount schedules. That's before withdrawal fees, which apply when you move funds off the exchange into a self-custody wallet, and which are usually a flat, asset-specific charge rather than a percentage.

The most commonly missed cost sits inside the spread, the gap between an asset's buy price and its sell price on a given venue. A platform can market itself as fee-free while embedding a wide spread into every trade, which means you're paying a real cost that simply never shows up as a labeled line item. This matters most on thinner altcoin pairs, where spreads can run meaningfully wider than on a liquid pair like BTC to a major stablecoin, sometimes overshadowing the quoted trading fee entirely.

For a copy trader, this changes how you evaluate a lead wallet's fee efficiency. A wallet that trades on a liquid, low-spread venue can look cheaper to copy than an identical strategy executed on a thin pair with a wide spread, even if both show the same headline percentage fee. Always judge the all-in cost, spread included, not just the advertised commission.

Holding an exchange's native token is one of the more overlooked discounts available here. Several major exchanges reduce both maker and taker fees for users holding a threshold amount of their platform token, sometimes by 20 to 25 percent. For a trader running meaningful monthly volume, that discount can be worth comparing against the token's own price risk before deciding whether it's worth holding purely for the fee reduction.

You copy a profitable wallet, match the entry, and still trail the leader on PnL. One reason is fee math. The trader you followed may be executing on a chain, wallet, and timing setup that is cheaper than yours, even when the trade looks identical on a dashboard.

Each chain prices blockspace differently. If you trade across Ethereum, Bitcoin, Solana, Polygon, or L2s, you need to know what drives the fee and which parts you can control.

On Ethereum, total cost comes from three variables: network demand, transaction complexity, and the priority you attach to speed. A plain ETH transfer is cheap relative to a swap, and a swap is cheap relative to a contract-heavy action that touches multiple pools or routers.

That matters in copy-trading. Following a wallet that uses simple, direct routes will usually leave less fee drag than following one that constantly uses aggregators, fresh token approvals, and multi-step contract calls. If you want the full mechanics behind base fee, priority fee, and gas units, this breakdown of Ethereum gas fees is the right reference.

Bitcoin fees are set by competition for blockspace. Wallets bid for inclusion, usually based on transaction size and current mempool pressure. During quiet periods, fees can stay manageable. During congestion, they can rise fast. Lightspark notes in its overview of Bitcoin fees that historical Bitcoin fees have spiked as high as $55 during high-demand periods: Lightspark's overview of Bitcoin fees.

Solana and Polygon work differently. Fees are usually low for routine activity, so the bigger trading question often shifts from gas to slippage, route quality, and whether the wallet is using priority settings or complex contracts. The fee is smaller, but it still affects repeat trading, especially for smaller accounts running many entries and exits.

L2s often reduce visible execution cost, but traders still pay for the full route. The full cost includes getting funds onto the network, executing there, and sometimes bridging back out.

That gap shows up clearly in copy-trading results. A trader operating natively on Arbitrum or Base may look highly efficient on-chain. A follower starting from mainnet, paying bridge costs, then mirroring smaller trades is running a worse fee profile from the first click.

Chain choice is a direct PnL input. For copy traders, on-chain analysis should include fee behavior, not just win rate. The wallets worth following are often the ones that generate returns without bleeding edge through avoidable execution costs.

Good traders don't treat the confirm screen as a surprise. They estimate first, decide second.

Most wallets already give you a speed choice. Slow, average, and fast are really trade-offs between cost and inclusion probability.

Use the wallet estimate as the first pass, then sanity-check it against an external tracker if the trade is sensitive. For EVM activity, a separate gas fee estimator helps when you want to compare the wallet's recommendation against current chain conditions before committing.

What works in practice:

Don't just read the total. Check what produced it.

A short visual walkthrough helps if you're calibrating these choices inside a wallet interface:

If the fee meaningfully changes your breakeven, pause. Either resize the trade, delay it, or execute on a more efficient chain. Traders get into trouble when they judge a setup by token upside but ignore whether the path to express that view is economically sensible.

Fee control is a trading skill, not a wallet setting.

For active traders and copy traders, wallet fees are often the hidden variable that turns a decent setup into a weak net return. The follower feels this even more than the original trader. If the lead wallet enters early and cheaply but you copy late on a more expensive route, your gross PnL and realized PnL diverge fast. Guidance from Coin.space's guide to reducing crypto transaction fees points to the same practical habits traders use in the field: transact during quieter periods when possible, batch actions, use lower-cost networks for routine activity, and choose wallets that let you adjust fee settings.

The biggest savings usually come from fewer unnecessary transactions and better timing, not from switching wallets.

That matters more in copy trading than many traders realize. A wallet that trades ten times a day with thin edge can look profitable on a chart and still be hard to copy after fees.

Wallet defaults are fine for ordinary transfers. They get expensive when the wallet assumes every transaction needs priority inclusion, or when a complex route masks where the cost is coming from. Discussion in this academic talk on transaction fee mechanisms and user welfare examines how wallet fee recommendations and manual overrides can produce different outcomes for users, especially when people rely heavily on automated estimates.

Use a simple operating rule:

When you move an asset like a stablecoin off an exchange into self-custody, the network you choose often matters more than which exchange you're withdrawing from. The same token withdrawn over a cheaper network can cost a small fraction of what the same withdrawal costs over a more expensive one, since the fee reflects that network's own congestion and fee model, not the asset itself.

Before confirming a withdrawal, check which networks the exchange supports for that specific asset and whether your destination wallet actually supports the cheaper option. Sending to the wrong network, or to a wallet that doesn't support it, risks losing the funds entirely, so this is a case where saving on fees requires double-checking compatibility first, not just picking the lowest number on the list.

Beyond execution habits, one structural lever is worth evaluating alongside everything else in this guide: whether holding a small position in your exchange's native token meaningfully reduces your ongoing fee bill.

The math is straightforward to run. Estimate your typical monthly trading volume, calculate the dollar difference between the standard fee rate and the discounted rate, and compare that monthly saving against the cost and price risk of holding the token itself. For active traders running consistent volume, the discount often pays for itself quickly. For occasional traders, the token's own volatility can easily outweigh the fee savings, making it a net loss rather than a genuine cost reduction.

Some fee-saving ideas look smart and still damage PnL.

The practical goal is not to win every fee decision. It is to keep transaction costs low enough that your edge survives after execution.

A wallet can post strong returns and still be a bad wallet to copy.

That usually shows up in the fee trail. One trader gets in and out with a small number of well-timed transactions. Another reaches a similar result by churning through approvals, bridges, retries, and small rotations that only make sense at their size or speed. On a leaderboard, they can look similar. In your account, they produce very different net PnL.

Fee-efficient wallets usually share a few patterns:

The point is simple. Copy trading works better when the wallet's execution style can survive your fee structure.

Review wallet history with net performance in mind, not just gross outcomes.

Two wallets with similar returns are not equal. The easier one to copy is usually the one that needed fewer transactions to produce those returns.

Wallet Finder.ai is one way to inspect wallet histories, PnL, position timing, and behavior across chains. Used with a fee lens, that kind of analysis helps separate traders who are efficient from traders whose profits depend on execution conditions you may not be able to match.

Some wallets are profitable because they can act faster than you, trade larger than you, or operate in a stack you do not use. Their edge is real, but it may not transfer.

That is why fee analysis belongs inside wallet selection, not after it. If a trader relies on rapid rotations, frequent contract interactions, or chain-hopping to keep returns up, your copied version can lose most of the value to costs. The better trader to follow is often the one with slightly lower headline returns and much cleaner execution. Over time, that wallet is more likely to leave you with copyable PnL instead of theoretical PnL.

Wallet fees are not background noise. They're a line item in every trading decision, whether you notice them or not.

The traders who keep more PnL usually do mundane things well. They know what fee they're paying, why they're paying it, and whether the action justifies the cost. They don't confuse gross performance with net performance. They don't treat a wallet preset like gospel. And they don't copy a wallet without checking whether that wallet's execution style can be replicated.

That mindset matters even more in copy trading. Following profitable wallets is useful. Following fee-efficient wallets is better. Once you start reading transaction history through that lens, you stop asking only who made money and start asking who kept it.

If you want to evaluate wallets by more than headline returns, Wallet Finder.ai can help you inspect trading histories, position timing, and execution patterns so you can spot wallets that are not just profitable, but practical to copy after fees.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.