Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

February 11, 2026

Dollar-Cost Averaging (DCA) is a straightforward investment strategy where you invest a fixed amount of money into a specific crypto at regular intervals, regardless of the price. Think of it as putting your crypto investing on autopilot, saving you from the nail-biting stress of trying to perfectly time the volatile market.

At its heart, DCA is all about consistency over timing. Instead of trying to pull off the near-impossible feat of buying at the absolute market bottom, you commit to a simple, repeatable plan. For instance, you could decide to buy $50 of Bitcoin every Friday, like clockwork. This disciplined approach helps smooth out your average purchase price over the long run.

Here's the simple mechanic that makes it work:

This process is a powerful shield against volatility, turning scary market downturns into genuine buying opportunities instead of moments of panic. If you're just getting started, you can see how this fits into the bigger picture by exploring other beginner-friendly crypto trading strategies in our guide.

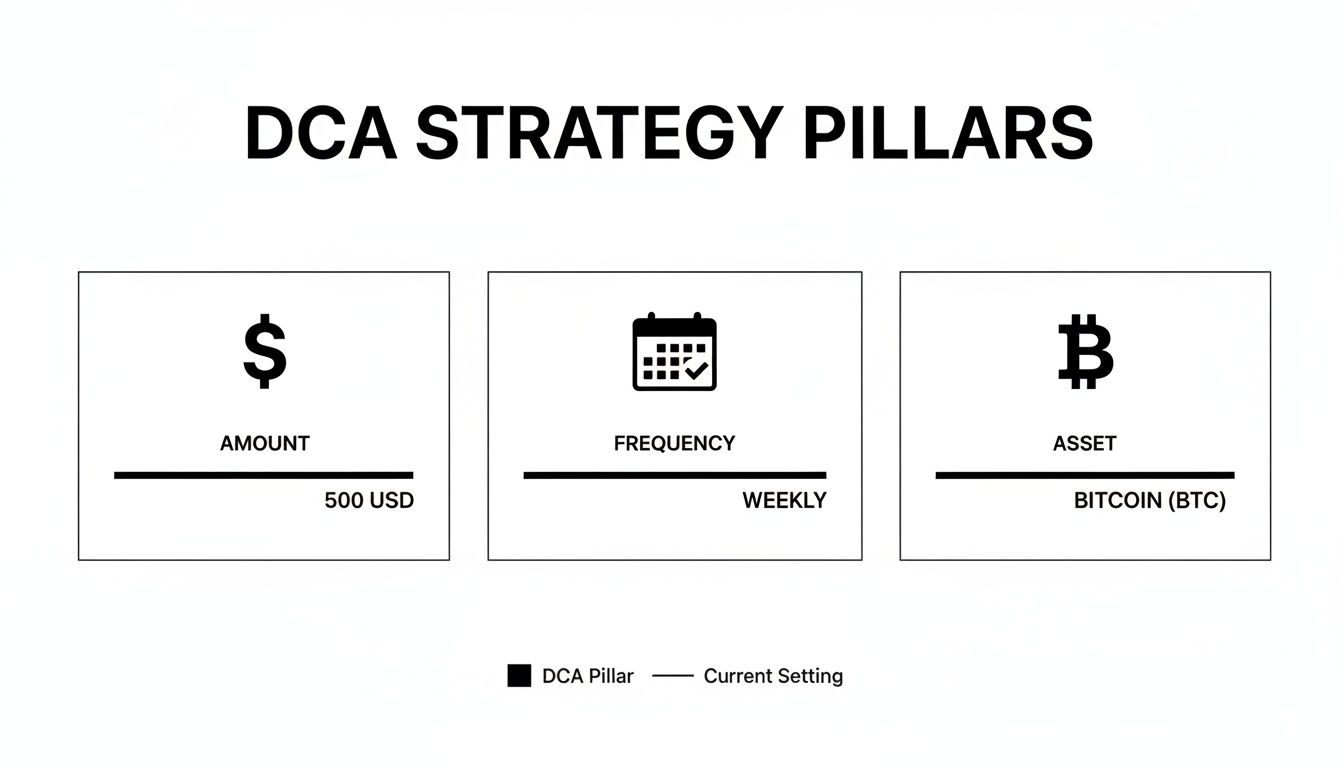

A solid DCA plan needs three simple but essential components. Nailing these down is the first step to making the strategy work for you.

To make it crystal clear, let's break them down.

The Three Pillars Of A Crypto DCA Strategy

ComponentDescriptionExampleFixed AmountThe specific dollar value you commit to investing each time. It should be an amount you can comfortably afford and stick with.Investing $100 into Ethereum.Regular FrequencyThe predetermined schedule for your buys. Common choices include daily, weekly, or monthly.Buying every Tuesday morning.Chosen AssetThe specific cryptocurrency you plan to accumulate for the long term, based on your own research and conviction.Focusing on accumulating Solana (SOL).

This strategy has become incredibly popular for good reason. A Kraken survey found that 59.13% of crypto users call DCA their go-to investment approach. This makes perfect sense in a market that saw Bitcoin plunge 75% from nearly $69,000 to under $17,000.

Imagine an investor who started a $100 weekly DCA in January 2022. They would have automatically scooped up more BTC during those lows, bringing their average cost down to around $25,000 by mid-2024. You can learn more about these kinds of investment trends over on BitPay.

Knowing the theory behind dollar-cost averaging is one thing, but seeing it work with real numbers is where the magic happens. Let's walk through a practical scenario to see how this strategy tames the market's wild swings.

Imagine you decide to invest $100 in Bitcoin every month for six months during a particularly volatile period—the perfect testing ground. This simple, consistent approach turns market chaos into a manageable process. You’re not trying to guess the tops and bottoms, which is a fool's errand for most. Instead, you're focused on disciplined accumulation, methodically building your position over time.

To really see the difference, we’ll compare your DCA journey against someone who invested their entire $600 as a lump sum right at the beginning—at the market's peak for this six-month window. This side-by-side comparison perfectly highlights the core strength of DCA in a rocky market.

Any DCA plan boils down to three simple pillars: how much you invest, how often you do it, and what you're buying.

This visual breaks the strategy down to its core components. It’s this structured, repeatable process that removes emotion and guesswork from the equation.

A powerful historical example unfolded after the 2017 bull run. Bitcoin crashed from $20,000 to below $3,200—a brutal 84% drop. Someone using DCA to buy $100 of BTC monthly for the 10 months starting in January 2018 would have ended up with an average cost of about $6,500 per coin, securing over 0.15 BTC.

Fast forward to a hypothetical December 2024, with BTC trading above $95,000. That position would be worth over $14,000, a 1,300% return that crushed what a lump-sum investor would have seen buying at the start of 2018. If you want to dive deeper, Fidelity has a great analysis of how DCA performs in volatile markets.

Okay, let's get into the numbers. The table below tracks our hypothetical six-month scenario. It shows the Bitcoin price each month, how much BTC each $100 purchase gets you, and how the average cost per coin changes for the DCA investor versus our lump-sum friend.

MonthBTC Price$100 DCA Buys (BTC)Cumulative BTC (DCA)Average Cost (DCA)Lump Sum (Bought Month 1)Month 1$50,0000.002000.00200$50,0000.01200 BTC at $50,000Month 2$45,0000.002220.00422$47,3930.01200 BTC at $50,000Month 3$35,0000.002860.00708$42,3730.01200 BTC at $50,000Month 4$40,0000.002500.00958$41,7540.01200 BTC at $50,000Month 5$55,0000.001820.01140$43,8600.01200 BTC at $50,000Month 6$60,0000.001670.01307$45,9070.01200 BTC at $50,000

See what happened there? By the end of six months, the DCA investor has a lower average cost per coin ($45,907 vs. $50,000) and has accumulated more Bitcoin overall (0.01307 vs. 0.01200 with the same capital).

Key Insight: Notice how the DCA investor automatically bought more Bitcoin during the price dips in months 3 and 4. This is the superpower of DCA—it forces you to buy more when prices are low, which systematically drags down your average entry price and provides a cushion against volatility that the lump-sum investor completely misses out on.

The real power of DCA isn't in some complex algorithm; it’s in its simplicity and its ability to build sustainable, long-term investing habits. It shifts your focus from chasing short-term pumps to patiently building a solid position over time.

Let's break down the core advantages that make this approach so effective.

Our psychology is often our worst enemy as an investor. The fear of missing out (FOMO) makes you want to buy at market peaks, and panic causes you to sell at the bottom. A DCA strategy acts as a circuit breaker for these gut reactions. By automating your buys, you stick to a logical plan, no matter how chaotic the market feels. Your decisions are driven by discipline, not drama.

Trying to perfectly time the crypto market is a losing game. It's stressful, and more often than not, it's a complete waste of time. DCA takes this impossible burden right off your shoulders.

You don't need a crystal ball to win with DCA. The strategy is built to embrace volatility and use it to your advantage, ensuring you are always accumulating without the pressure of guessing the market's next move.

This approach is pragmatic. It accepts that you'll probably never buy the absolute bottom, but it also protects you from going all-in right at the top.

One of the biggest myths in investing is that you need a huge pile of cash to get started. DCA completely shatters that idea. You can begin with an amount that fits your budget, whether that's $20 a week or $200 a month. This accessibility throws the doors wide open for anyone to start building a portfolio without taking on scary financial risk.

Success in crypto, like any market, is a marathon, not a sprint. When you commit to a regular buying schedule, you build the powerful habit of consistency, which is the secret sauce for long-term wealth creation. This steady, "set-it-and-forget-it" method keeps you in the game and focused on your big-picture goals, stopping you from making impulsive, short-sighted moves.

While dollar-cost averaging is a fantastic strategy for building discipline and taking emotion out of investing, it's not a magic wand. It won't guarantee the highest possible profits in every market scenario. To use DCA effectively, you have to understand its trade-offs.

The biggest drawback of DCA becomes clear during a strong, sustained bull market. If a coin is on a steady upward trajectory, a single lump-sum investment at the start will almost always outperform a DCA strategy. With DCA, each purchase is made at a slightly higher price, raising your average cost. The lump-sum investor, meanwhile, locked in their entire position at the lowest price before the rally.

Key Takeaway: DCA is built to protect you from gut-wrenching drops. In a market that only seems to go up, this protective feature becomes a drag on your potential returns compared to going all-in from day one.

Transaction fees can be a silent portfolio killer. When you're making frequent small buys, those fees can add up and eat into your capital. To mitigate this:

Opportunity cost is the potential gain you miss out on by not putting all your capital to work at once. If the market blasts off, the cash you were holding for future DCA purchases effectively missed the boat. This is the fundamental trade-off:

Knowing this helps you pick the right strategy for your market outlook.DCA Performance Across Market Regimes: When It Wins and When It Loses

Understanding when dollar-cost averaging truly shines versus when it underperforms is critical for setting appropriate expectations and deciding whether DCA is right for your situation. The strategy's effectiveness varies dramatically depending on which type of market you're experiencing, and blindly DCAing through every condition without understanding these dynamics leads to suboptimal results.

The fundamental insight is that DCA is a defensive strategy, not an offensive one. It's built to protect you from catastrophic timing mistakes and smooth out volatility, not to maximize returns in trending markets. This distinction matters because it shapes when you should commit to strict DCA discipline versus when you might want to modify your approach or consider alternatives.

Bear markets represent DCA's absolute sweet spot—the condition where the strategy delivers its maximum value and outperforms almost every alternative approach. When prices are in sustained decline with violent downward volatility, DCA systematically accumulates more units at progressively lower prices, setting you up for explosive gains when the market eventually recovers.

The mechanics work beautifully during crashes. Each purchase buys more cryptocurrency than the previous one as prices fall, dramatically lowering your average cost basis. A concrete example: Bitcoin fell from sixty-nine thousand dollars in November 2021 to fifteen thousand dollars by November 2022—a seventy-eight percent collapse that destroyed traders who bought the top. Someone DCAing one hundred dollars weekly throughout this entire period would have accumulated Bitcoin at an average price around thirty-five thousand dollars, positioning them for substantial profits when price recovered above that level.

The psychological benefit during bear markets is even more valuable than the mathematical advantage. When prices are crashing and fear dominates sentiment, most investors freeze or panic sell. DCA forces you to keep buying through the terror, accumulating when assets are cheapest and everyone else has capitulated. This disciplined buying during maximum pessimism is how generational wealth gets built, but it's psychologically brutal without a systematic plan forcing your hand.

The strategic approach for bear markets is maintaining strict DCA discipline and potentially even increasing allocation if you have conviction in the asset's long-term survival. Some sophisticated investors run a base DCA amount continuously, then add supplemental buys during particularly steep capitulations—maybe doubling their weekly buy when price drops thirty percent from recent highs. This "DCA with dip buying" hybrid captures the strategy's defensive benefits while opportunistically adding exposure during panic.

Bull markets expose DCA's fundamental weakness—in consistently rising markets, the strategy systematically underperforms simple lump-sum investing by design. Each DCA purchase happens at a higher price than the previous one, raising your average cost and reducing your total position size compared to if you'd deployed all capital at the beginning.

The math is unforgiving. If Bitcoin rises from forty thousand dollars to one hundred thousand dollars over two years and you DCA one hundred dollars weekly, your average purchase price might be seventy thousand dollars. The lump-sum investor who bought everything at forty thousand enjoys a one hundred fifty percent gain on their entire capital, while your DCA approach only captures full gains on the portion purchased early—later purchases have progressively smaller gains.

This doesn't make DCA wrong during bull markets, but it does make it suboptimal for pure return maximization. The trade-off is risk versus reward: lump sum captures maximum upside but exposes you to catastrophic loss if you buy the peak before a crash; DCA sacrifices some upside potential for protection against buying the top. Your choice depends on your risk tolerance and market timing confidence.

The strategic modification for confirmed bull markets is shortening your DCA timeline or increasing purchase amounts to deploy capital faster. Instead of spreading purchases over two years, compress them into six months to capture more of the trending move while still maintaining some average-cost-basis benefit. Alternatively, front-load your plan by making your early DCA purchases larger than later ones, capturing more exposure at lower prices while maintaining the discipline of regular buying.

Sideways or range-bound markets create the worst conditions for DCA because the strategy's benefits disappear while its costs remain. When price oscillates in a predictable range for extended periods, your average cost simply ends up near the middle of the range—offering no meaningful advantage versus just buying once at mid-range prices, but charging you transaction fees for dozens of purchases that accomplished nothing.

The problem is wasted capital efficiency. If Bitcoin trades between fifty thousand and sixty thousand dollars for twelve months while you DCA weekly, you'll end up with an average cost around fifty-five thousand dollars—exactly what you'd get from a single purchase at mid-range. But you paid transaction fees fifty-two times instead of once, and kept capital sitting in cash waiting for DCA purchases instead of having it fully deployed earning yield elsewhere.

The strategic response to detected sideways markets is pausing DCA temporarily and either deploying a lump sum at the bottom of the established range or redirecting DCA capital toward assets showing clearer trends. Some investors keep DCA running at reduced amounts during sideways chop just to maintain the discipline and habit, accepting the inefficiency as the price of staying in the game, but it's not the mathematically optimal approach.

The challenge is recognizing which market regime you're actually in—this requires honest assessment rather than wishful thinking. A twelve-month range from fifty to sixty thousand dollars is clearly sideways. But is a three-month consolidation after a rally sideways accumulation before the next leg up, or the beginning of a bear market? Getting this assessment right determines whether pausing DCA is smart risk management or the first step toward missing the recovery entirely.

Alright, enough theory. Let's put a real, automated crypto DCA plan into action. Here’s a blueprint to get your own "set-it-and-forget-it" strategy running today.

This automation is the secret sauce. It takes emotion out of the equation and forces discipline by doing it for you.

One of the most difficult decisions DCA practitioners face is whether to pause their strategy during certain market conditions or life circumstances. The standard advice is "never stop DCA, just keep buying through everything," but this absolutist approach ignores legitimate scenarios where pausing makes strategic or practical sense. Understanding when to pause and when to power through is essential for long-term success.

The fundamental tension is between discipline and adaptability. DCA's power comes from removing discretion—the plan forces you to buy regardless of conditions, preventing emotional mistakes. But complete inflexibility can also be a weakness when circumstances genuinely change in ways that invalidate your original thesis or create better opportunities elsewhere.

Not all pauses are created equal. Some represent rational strategy adjustments, while others are emotional capitulation in disguise. Here are the legitimate scenarios where pausing your DCA plan makes strategic sense rather than being a discipline failure.

Fundamental Thesis Breakdown

The most valid reason to pause is when the fundamental investment thesis for your chosen asset breaks down. If you're DCAing into a specific cryptocurrency because you believe in its technology and team, but the lead developer quits, the protocol suffers a major exploit, or regulators issue an existential threat, continuing to blindly buy is throwing good money after bad. Your DCA plan should have clearly defined "circuit breakers"—conditions that would cause you to pause and reevaluate.

The key is distinguishing between thesis breakdown and temporary setbacks. Price volatility, market fear, and negative headlines are temporary setbacks that you should DCA through. Regulatory bans, permanent loss of user funds, or project abandonment by the development team are thesis breakdowns justifying a pause. Write down your circuit breaker conditions in advance so you can assess them objectively rather than making emotion-driven decisions when fear is highest.

Severe Personal Financial Emergency

Life happens, and sometimes you need that capital for genuine emergencies—medical bills, job loss, unexpected family obligations. Continuing DCA during a personal financial crisis by racking up credit card debt or depleting emergency savings is poor financial management that puts your entire financial wellbeing at risk for the sake of maintaining a crypto investment schedule.

The strategic approach is pausing DCA but not panic-selling accumulated positions unless absolutely necessary. Your existing crypto holdings can continue appreciating while you redirect income toward immediate needs. Resume DCA only after your emergency fund is rebuilt and your financial situation has stabilized. This pause is about proper financial priorities, not market timing.

Detected Bubble Conditions

The most controversial legitimate pause reason is detecting clear bubble conditions where valuations have detached from any rational fundamental justification. When Bitcoin hit sixty-nine thousand dollars in 2021, various on-chain metrics and valuation models suggested extreme overheating. Pausing DCA during these periods to avoid buying the absolute peak, then resuming after a correction, can meaningfully improve your long-term returns.

The difficulty is having the discipline to actually resume after the pause. Many investors pause during bubbles correctly, but then fail to restart DCA during the subsequent crash when fear is highest—exactly when buying would be most profitable. If you're going to pause for valuation reasons, you must have pre-defined restart conditions, like price falling thirty percent from recent highs or on-chain metrics returning to neutral ranges.

These are the pause justifications that feel reasonable in the moment but actually represent discipline failures that will harm your long-term results. Recognizing and resisting these emotional traps is critical for DCA success.

Price Has Fallen Too Much

The absolute worst reason to pause DCA is because the price has crashed and you're scared. This is exactly backwards—crashes are when DCA delivers maximum value by accumulating at bargain prices. Pausing because you're afraid the price will go lower is market timing in disguise, the very behavior DCA is designed to prevent.

If you find yourself wanting to pause because "I'll wait for it to drop more," you're abandoning the strategy at precisely the wrong moment. The correct mental frame is viewing price crashes as sales—would you stop shopping just because your favorite store started offering huge discounts? The fear is understandable, but acting on it destroys DCA's effectiveness.

Waiting for Confirmation of Trend Reversal

Another tempting but destructive pause justification is "I'll resume DCA once I see clear signs the bottom is in and the trend is reversing." This is just market timing with extra steps. By the time the trend reversal is "clear" and you feel safe resuming, price has already recovered significantly from the lows—you'll have missed the best buying opportunity while sitting in cash waiting for safety.

DCA specifically exists because we can't reliably identify bottoms until well after they've passed. Pausing to wait for confirmation defeats the entire purpose of the strategy. You're supposed to be buying through the uncertainty, not waiting for certainty that never comes at attractive prices.

Temporary Market Euphoria or Depression

Short-term sentiment swings should never trigger DCA pauses. If you pause every time the market feels overly euphoric and restart when it feels excessively fearful, you're just introducing timing discretion that research shows consistently underperforms systematic buying. Sentiment is usually wrong at extremes—maximum euphoria often comes mid-rally, and maximum fear often comes before recovery.

The discipline requirement is continuing to execute your DCA plan with complete disregard for how you or the market feels at any given moment. Your plan is your plan. Emotions are noise. Pausing because you have a feeling about where the market is heading is abandoning the systematic approach for gut-level gambling.

If you do pause your DCA for a legitimate reason, having a clear resume protocol prevents the pause from becoming permanent abandonment. Many investors pause temporarily but never restart, turning a strategic decision into an accidental exit from the market.

Your resume conditions should be specific and ideally mechanical. "Resume DCA when I rebuild my emergency fund to six months of expenses" is concrete and measurable. "Resume when the market feels safer" is vague and subjective. Write down your resume conditions at the same time you pause, establishing clear goalposts rather than leaving the decision for future-you to make emotionally.

For fundamental thesis breakdowns, the resume condition might be "project launches delayed feature and passes new security audit" or "regulatory uncertainty resolves." For valuation pauses, it might be "price retraces thirty percent from peak and RSI drops below forty." Whatever the condition, it should be observable and objective, preventing indefinite procrastination from fear or doubt.

While standard DCA follows a fixed-amount, fixed-schedule approach, several advanced variations can potentially improve results by introducing strategic flexibility while maintaining systematic discipline. These modifications aren't necessarily better than pure DCA, but they offer options for sophisticated investors willing to add complexity in exchange for potentially enhanced returns.

Understanding these alternatives helps you decide whether vanilla DCA is sufficient for your goals or whether you should implement one of these more nuanced approaches. Each variation makes different trade-offs between simplicity and optimization.

Conviction-weighted DCA modifies the fixed-amount principle by varying your purchase size based on current valuations relative to your assessed fair value. Instead of buying one hundred dollars every week regardless of price, you might buy fifty dollars when price seems high, one hundred dollars at fair value, and two hundred dollars when it seems cheap.

This approach attempts to combine DCA's discipline with value investing principles—buying more when valuations are attractive and less when they're stretched. The benefit is better capital efficiency than strict DCA by concentrating purchases during bargains while maintaining regular buying that prevents completely missing the market.

The implementation requires establishing valuation bands in advance. Maybe you define fifty thousand dollars as fair value for Bitcoin, making forty thousand dollars "cheap" (double DCA), thirty thousand dollars "very cheap" (triple DCA), sixty thousand dollars "expensive" (half DCA), and seventy thousand dollars "very expensive" (quarter DCA). These bands should be based on rational models—on-chain metrics, realized price multiples, production cost estimates—not gut feelings.

The risk is that this introduces subjectivity and timing decisions that can go wrong. You might define sixty thousand dollars as expensive and reduce DCA, then watch price run to one hundred thousand without giving you the "cheap" re-entry you were hoping for. You've underallocated to an asset that worked, essentially market-timing yourself into underperformance. Unless you have strong conviction in your valuation framework and the discipline to stick with it, vanilla DCA is probably safer.

Value averaging (VA) represents a more sophisticated alternative where instead of investing a fixed dollar amount, you target a fixed growth in portfolio value. If your target is portfolio increasing by one hundred dollars weekly but it already grew two hundred dollars from price appreciation this week, you invest nothing. If price fell and portfolio only grew fifty dollars, you invest one hundred fifty to hit the target.

This approach has an elegant logic—you automatically buy more when prices are falling (since you need more purchases to hit your value target) and less or nothing when prices are rising (since appreciation already hit your target). It's mechanically similar to DCA but even more aggressively accumulates during dips.

The practical challenge is capital management. Value averaging requires keeping substantial cash reserves because your weekly investment amounts can vary wildly—anywhere from zero to several multiples of your average investment depending on price movements. During crashes, you might need to invest five hundred dollars one week to hit your value target, but you don't know this in advance, so you need to maintain reserves.

The second challenge is that value averaging sometimes requires selling during strong rallies if price appreciation exceeds your target growth by substantial amounts. The system might tell you to sell some holdings to bring portfolio growth back to target, which feels counterintuitive during bull markets and creates taxable events. Most investors modify VA to make selling optional rather than mandatory, only making buys or pausing, never sells.

Rather than DCAing into a single asset, this approach systematically builds a diversified crypto portfolio through regular rebalancing purchases. You might allocate seventy percent to Bitcoin, twenty percent to Ethereum, and ten percent to a basket of large-cap altcoins, making weekly purchases that restore these target allocations.

The implementation means each week you assess which assets have underperformed and direct your fresh capital entirely to whatever is furthest below its target allocation. If Bitcoin has outperformed and is now eighty percent of your portfolio versus the seventy percent target, while Ethereum has underperformed and dropped to fifteen percent versus the twenty percent target, your entire DCA purchase that week goes to Ethereum to restore balance.

This creates a systematic "buy low, sell high" rebalancing discipline. Assets that have fallen in price receive more investment to restore their target weight, while assets that have appreciated get no additional investment until they fall back into underweight status. Over long time horizons, rebalancing tends to improve returns by forcing you to accumulate laggards before they recover.

The trade-off is increased complexity and more taxable events if you implement true rebalancing including sales, not just rebalancing through new purchases. You also need clear conviction in your target allocation percentages—if you arbitrarily chose weights that don't reflect the assets' actual long-term potential, you'll be throwing good money after bad by constantly rebalancing into structural losers.

Let's tackle some of the most common questions people ask when they begin dollar-cost averaging in crypto.

Not always, but it's usually safer. In a market that only ever goes up, a lump-sum investment at the start would make more money. But crypto is volatile. DCA is a risk management strategy. Its real job is to protect you from the disaster scenario of investing all your cash right at a market peak.

Determining your optimal DCA amount requires balancing aggressive wealth building with financial sustainability and safety. The general guideline is allocating between five and twenty percent of your after-tax income to crypto DCA, with the specific percentage depending on your age, risk tolerance, existing financial foundation, and other investment allocations.

Conservative investors with substantial existing traditional investments, older investors closer to retirement, or those with dependents and significant financial obligations should lean toward the five to ten percent range. This allocation allows meaningful crypto exposure and wealth building potential while ensuring you're not over-concentrated in a highly volatile asset class that could damage your financial security if it crashes. If you're allocating fifty dollars weekly on five thousand dollars monthly income, you're at roughly ten percent, which is reasonable for cautious investors.

Aggressive younger investors with high risk tolerance, minimal financial obligations, strong emergency funds, and substantial faith in crypto's long-term prospects might push toward the fifteen to twenty percent range. At twenty percent, someone earning five thousand monthly would DCA one thousand dollars, rapidly building a significant crypto position. This higher allocation makes sense for investors in accumulation phase with long time horizons who can weather major drawdowns without selling, but it requires genuine risk tolerance and the discipline to maintain course through crashes.

The critical rule is never DCAing with money you can't afford to lose or might need within your investment timeframe. Your DCA capital should come only after you've covered essential expenses, maintained emergency savings, funded any debt obligations, and contributed to tax-advantaged retirement accounts that provide employer matching. Crypto DCA is speculative capital deployment—it should represent your "growth and risk" bucket, not your financial foundation. If you find yourself skipping bills or reducing emergency savings to maintain DCA, your allocation is too aggressive and needs reduction to sustainable levels.

Understanding the tax treatment of your DCA strategy is essential for avoiding surprises and optimizing your after-tax returns. Each DCA purchase creates a new tax lot with its own cost basis and holding period, creating significant complexity when you eventually sell portions of your accumulated position.

In most jurisdictions including the United States, each purchase is treated as a separate acquisition for tax purposes. If you DCA one hundred dollars weekly for a year, you've created fifty-two individual tax lots, each with different purchase prices and holding periods. When you later sell some of your accumulated position, tax rules require determining which specific lots you're selling, which determines your capital gain or loss and whether it's short-term or long-term.

The default method is First-In-First-Out where the lots you purchased earliest are considered sold first. This is often favorable because your oldest lots have the longest holding periods (qualifying for lower long-term capital gains rates) and potentially the lowest cost basis if you DCA'd through an early accumulation phase, giving you larger gains that benefit from preferential tax treatment. However, FIFO can be disadvantageous if your earliest purchases were at high prices before a crash—selling those lots first means realizing large losses.

The alternative is Specific Identification where you explicitly designate which lots you're selling, allowing tax optimization strategies. If you want to realize losses to offset other gains (tax-loss harvesting), you can specifically sell your highest-cost-basis lots. If you want long-term capital gains treatment, you can specifically sell lots held over a year. This requires meticulous record-keeping but provides maximum flexibility for tax management.

The strategic consideration is planning ahead for eventual exit. If you're DCAing with intent to hold for years, the default FIFO probably works fine and minimizes complexity. If you plan to actively trade or take partial profits during your accumulation phase, implementing specific ID from the start with detailed lot tracking will save massive headaches and potentially significant tax dollars when you need to report capital gains and losses.

Deciding whether to continue DCA after reaching your initial target position represents a strategic inflection point that depends on your updated assessment of the asset's value, your portfolio allocation goals, and your ongoing conviction in the investment thesis.

If you began DCA with a goal of accumulating one full Bitcoin and you've achieved that target, the decision to continue depends on whether you still believe Bitcoin is appropriately valued or undervalued at current prices and whether you're comfortable with your portfolio's crypto allocation getting larger. If Bitcoin has appreciated substantially during your DCA journey and now represents a much larger percentage of your net worth than planned, continuing might create uncomfortable concentration risk that proper diversification would suggest reducing rather than expanding.

The systematic approach is establishing new targets tied to updated valuations rather than just continuing indefinitely on autopilot. Maybe you hit your one Bitcoin target when price is sixty thousand dollars. You could then set a new target of reaching one-point-five Bitcoin only if price falls below forty thousand dollars again, otherwise pausing DCA to that asset and redirecting capital toward other undervalued opportunities or to rebalancing your portfolio back to target allocations.

The alternative is transitioning from accumulation DCA to maintenance DCA where you continue making regular purchases but at a reduced amount or frequency that grows your position slowly without dramatically changing your allocation. Perhaps you reduce from weekly one hundred dollar purchases to monthly one hundred dollar purchases, maintaining exposure and continued accumulation while limiting how much additional concentration you're building. This keeps you psychologically engaged with the strategy and ensures you stay invested rather than exiting completely, while preventing your position from becoming uncomfortably large.

This usually boils down to balancing a better average price against transaction fees.

FrequencyProsConsWeeklySmooths out price volatility effectively by catching more minor dips and spikes.More transactions mean potentially higher cumulative fees over time.MonthlySimpler to manage and involves fewer transaction fees.Less effective at averaging; can miss significant price action within the month.

For most people, a weekly or bi-weekly schedule hits the sweet spot. It does a great job of reducing volatility's impact without racking up excessive fees. A crypto average calculator can be very insightful for running your own numbers.

Absolutely. The principle works just as well for volatile assets like altcoins—in fact, it's arguably even more powerful for them. DCA allows you to gain exposure to assets with massive growth potential while dramatically reducing the risk of buying into a temporary, hype-fueled price spike. Just ensure the altcoins you pick fit your portfolio goals.

Your exit plan should be tied to your personal goals, not daily market movements. Stopping your plan because prices feel too high or too low is an emotional decision that undermines the strategy.

Key Principle: A good DCA plan needs a clear finish line. Maybe you stop once your portfolio hits a certain value, or when you need the money for a major life event like a down payment. Tying your exit to a personal goal is how you keep emotion from wrecking your long-term plan.

Ready to stop guessing and start learning from the best? Wallet Finder.ai gives you the on-chain intelligence to discover top-performing wallets and mirror their strategies in real time. Start your 7-day trial and find your edge today!

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.