Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

June 20, 2026

You open your terminal, Telegram, X feed, TradingView, and a DEX screener. Ten minutes later, you've seen twenty “can't miss” trades and learned nothing useful. That's where most traders are when they start looking at automated trading signals.

The appeal is obvious. Signals promise structure in a market that never stops moving. In crypto, especially DeFi, they also promise speed. But speed only helps if the signal is real, the execution is clean, and the edge survives contact with the market.

A lot of guides stop at signal generation. That's the easy part to talk about. The harder part is what happens after the alert fires: whether the trade fills near the intended price, whether too many others are chasing the same setup, and whether the model still works after conditions shift. That's the part that decides whether automated trading signals are useful or just another layer of noise.

Most traders confuse a signal with a bot. They're not the same thing.

The signal is the decision layer. It says buy, sell, reduce, or do nothing. The bot is the execution layer. It takes that instruction and routes the order. If the signal is weak, automating it just helps you lose money with more discipline.

That distinction matters because automated trading has become a serious market category, not a hobbyist side project. One industry projection puts the global automated algorithmic trading market at $53.8 billion by 2035 with a 10.6% CAGR according to EtnaSoft's market overview. That doesn't prove any specific signal is good. It does show that computer-generated entries and exits are now part of the mainstream trading stack.

A useful signal cuts the decision down to a rule you can test. That rule might come from price structure, statistical patterns, order flow, or blockchain activity. In DeFi, the source often matters more than the syntax.

Three examples:

Retail traders often buy signal feeds as if they're buying outcomes. They're not. They're buying a hypothesis about market behavior.

Practical rule: Treat every automated signal as a tradable claim that still needs validation under live conditions.

That means asking different questions than most marketing pages answer. Not “how many alerts do I get?” but “what kind of edge is this supposed to capture?” Not “can I connect it to a bot?” but “does the edge remain after fees, slippage, and latency?”

In volatile crypto markets, those questions aren't optional. They're the whole job.

Your article teaches readers how to evaluate signals. Most arrive looking for a specific answer first: which providers are worth investigating before they build an evaluation framework. This section provides that map — not as an endorsement list, but as the landscape orientation that makes the rest of the article more actionable.

The signal provider market in 2026 runs across four distinct categories. Free Telegram groups with public track records represent the lowest-barrier entry point. Evening Trader has established a reputation as the most consistently cited free signal source, with verified win rates referenced in multiple independent reviews at 92%+ for simpler setups. The free tier provides enough signal exposure for a new trader to build a feel for signal quality without financial commitment. The limitation is frequency — free groups typically provide fewer signals per week than paid options, which means fewer opportunities to evaluate whether the provider's edge is genuine or regime-specific.

Paid Telegram and Discord groups occupy the middle tier. Learn2Trade has been consistently cited across NFTPlazas and Ventureburn's 2026 reviews for verified accuracy in the 79% range with affordable monthly pricing (approximately £39/month for the standard tier). CryptoSignals.org specializes in Bitcoin and major altcoin signals with detailed trade rationale rather than just entry/exit levels — which matters for traders who want to understand why a signal was generated, not just what it says. Wolf of Trading and Fed Russian Insiders are consistently mentioned in the premium Telegram category but at higher price points.

AI-powered automation platforms represent the third category. 3Commas is the most frequently cited in this space, combining a signal marketplace with bot infrastructure that can execute trades automatically when signals arrive. Signals Blue and Sublime Traders are cited as reliable providers of AI-generated signals that feed into automation pipelines. Dash 2 Trade blends automated market scanning with analyst review in a hybrid model that retains human oversight on algorithmically identified setups.

At the premium end, providers like Fat Pig Signals operate on lifetime pricing above $1,800 — a price point that implies either very high signal confidence or an effective marketing model for retail traders willing to pay for perceived exclusivity. The honest framing for premium pricing is that the lifetime cost is only justified if the win rate and average return per signal exceed what a lower-cost or free provider delivers by enough margin to recover the price differential. NFTEvening's May 2026 guide noted that top-performing bots and algorithmic traders achieve 10-30% annual returns in favorable markets — and that 60-70% of automated traders still lose money due to poor setup or unrealistic expectations. Premium price does not automatically correlate with premium signal quality, and no provider should be subscribed to without first verifying their publicly disclosed track record against independent sources rather than their own marketing materials.

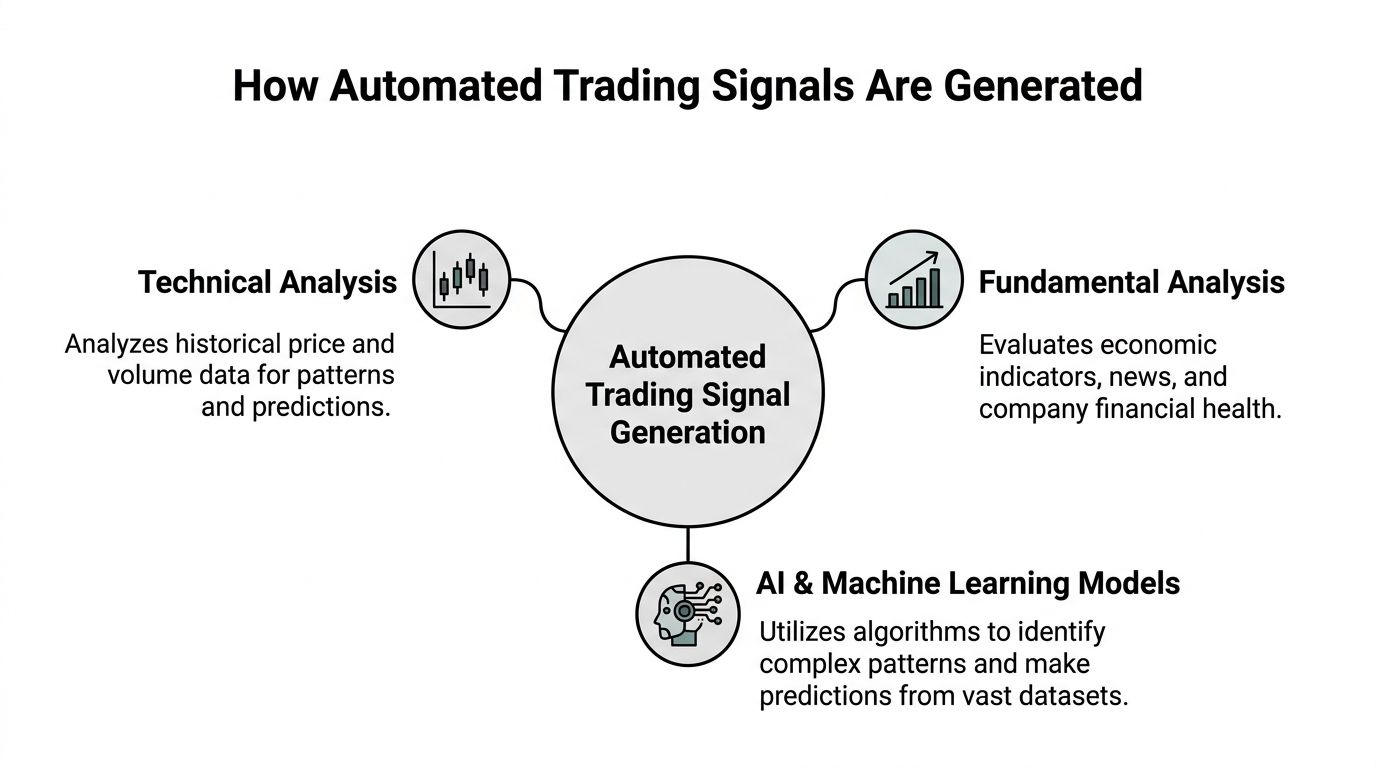

Most signal engines fall into a few broad families. You don't need to be a quant developer to understand them. You do need to know what each one is good at, and where each one tends to break.

Technical signals are the closest thing to market traffic lights. They use historical price and volume to define conditions like trend continuation, reversal, breakout, or exhaustion.

Typical building blocks include moving averages, RSI, volatility bands, support and resistance, and candle structure. The strength of this approach is clarity. Rules are visible, testable, and easy to automate. The weakness is crowding. If too many traders watch the same setup, the edge gets thinner.

Technical signals work well when you need:

In traditional markets, fundamentals include earnings, balance sheets, and macro releases. In crypto, the closest equivalents are token releases, governance decisions, liquidity changes, protocol incentives, listings, and major ecosystem news.

This approach usually has stronger narrative context than pure chart signals. It often has weaker timing. You may know a catalyst matters before the market decides exactly when to price it in.

Think of these as pattern filters with larger memory. Instead of relying on a handful of hand-built rules, a model tries to detect interactions across many variables.

That can be useful when relationships are messy. It can also create a black box. If you can't explain the conditions under which the model should fail, you probably don't understand the signal well enough to size it properly.

For DeFi traders, this is often the most interesting category. On-chain heuristics track wallet behavior, flows, token movements, and timing patterns directly on the blockchain. In plain English, you're watching what skilled participants do rather than guessing from price alone.

That doesn't mean copying every whale trade. It means identifying wallets with repeatable behavior and understanding context: entry timing, sizing, holding period, and whether the trade fits a pattern.

A practical setup often combines methods. A trader might source the idea from on-chain activity, use technicals for entry timing, and use automation for execution. That's usually stronger than relying on any single lens.

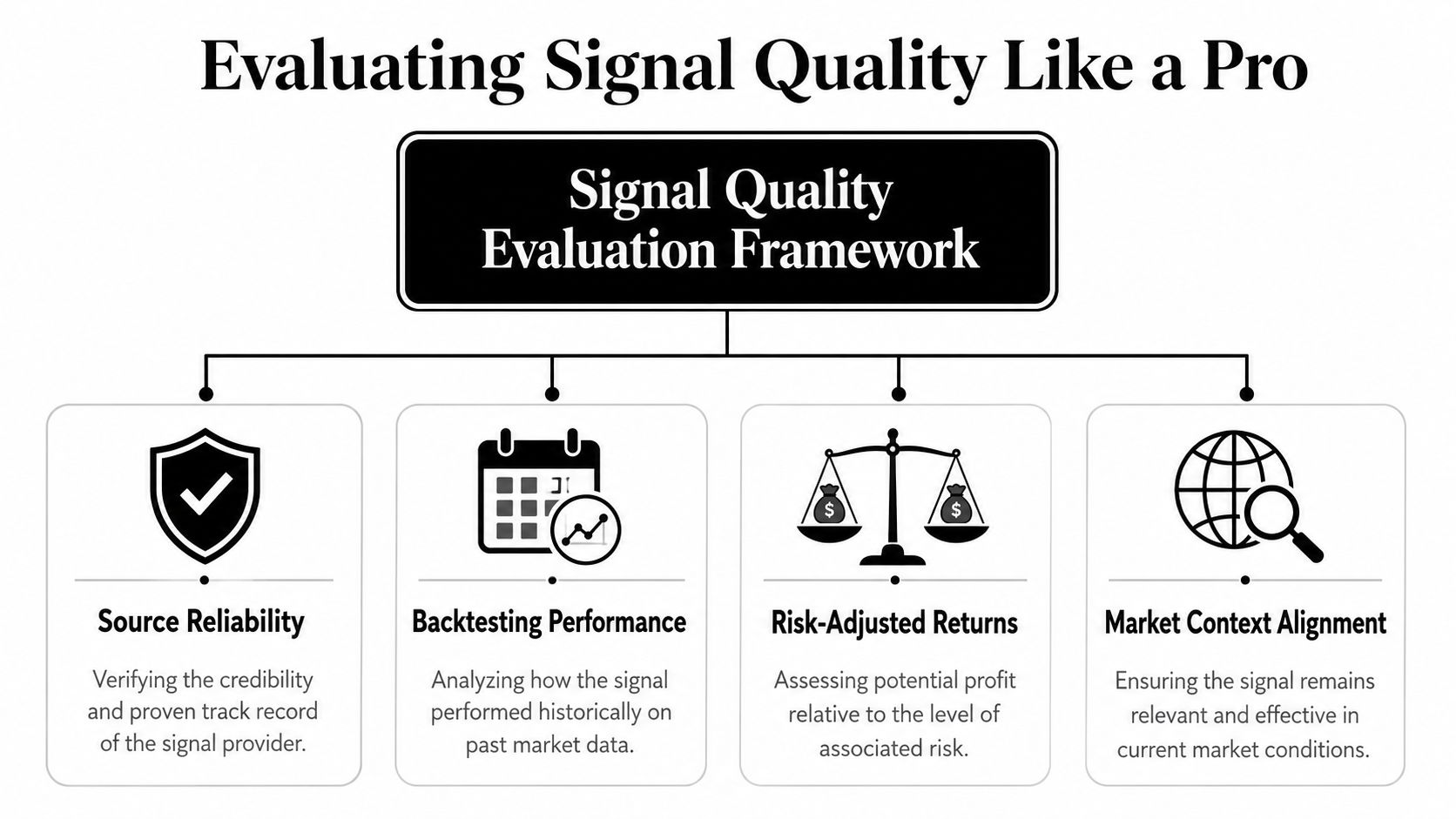

Most bad signal products hide behind one metric: win rate. It's easy to market and easy to misunderstand.

A signal can win often and still be terrible if the losers are large, the downside is uncontrolled, or the gains come with ugly drawdowns. The professional view is simpler. You're not buying alerts. You're buying a statistical edge.

The most widely used evaluation framework centers on Sharpe ratio, maximum drawdown, win rate plus profit factor, Sortino ratio, and Calmar ratio, as outlined in NURP's guide to trading system metrics.

Here's how to read them in plain language:

If a signal provider shows a high win rate but avoids profit factor and drawdown, that's a warning sign. Plenty of weak systems produce frequent small wins and then give back a large chunk when the market changes.

A solid operating rule is to manually test a system for at least 30 trades before automation and then monitor it weekly for changes in win rate, average trade duration, maximum consecutive losses, and profit factor, based on the same NURP framework for system evaluation.

That rule does two things. First, it forces you to observe how the signal behaves instead of outsourcing judgment to a dashboard. Second, it gives you a baseline. Without a baseline, you can't tell whether live performance drift is normal or dangerous.

A signal that can't survive a basic trade log usually won't survive real capital.

Use this short checklist before you automate any signal source:

A signal becomes investable when the metrics, execution style, and market context all line up. Not before.

A signal can be valid, profitable, and still stop working.

That's one of the least appreciated realities in systematic trading. Traders often spend all their time asking whether a strategy works and almost none asking how they'll know when it doesn't.

Modern systems have to adapt to volatility changes and macro regime shifts, and the key question is often when automation stops working, not whether it works at all, as discussed in Edgeful's guide to automated trading strategies.

In practice, signal decay usually comes from three sources:

You don't need a complex research desk to spot trouble early. You need a process.

Watch for changes in behavior, not just losses. A good signal can lose money for a stretch and still be healthy. A decaying signal often changes character first. It enters later, takes longer, slips more, or produces weaker follow-through.

Useful warning signs include:

Your kill switch isn't proof the strategy failed. It's proof you're running it like an operator instead of a believer.

The traders who survive don't marry their signals. They monitor them, reduce size when behavior changes, and pause automation when the edge looks impaired.

A signal becomes a trade through a chain of small operational decisions. Most of the actual risk sits in that chain, not in the alert itself.

In most setups, the workflow looks like this:

That sounds clean on paper. Live trading isn't clean.

The practical questions are about slippage, fill quality, and alert latency, and a signal's theoretical edge often degrades during execution, which is a central point in Altrady's discussion of signal bot automation.

For DeFi traders, this degradation gets worse when liquidity is thin, gas is unstable, or multiple wallets and bots rush the same token at once. The signal may still be right directionally. You just may not capture enough of the move to make it worth trading.

Common leaks include:

Before automating anything, define your controls in advance:

A walkthrough helps if you're building this stack for the first time:

The cleanest workflow is usually semi-automated at first. Let the system generate and route alerts, but keep order approval or size approval manual until you trust the behavior. That gives you visibility into execution drift before you fully hand over control.

The mistake is thinking automation removes oversight. In reality, good automation increases the need for monitoring because the system can now make the same mistake faster and more consistently.

On-chain signals solve a problem that technical and model-driven systems often struggle with in crypto. They show you who acted, when they acted, what size they used, and whether that behavior has been repeatable across prior trades.

That's useful because not every trader wants to build signal logic from scratch. Many just need a cleaner way to observe wallets with strong behavior and turn those observations into alerts.

One option is Wallet Finder.ai, which tracks wallet activity across major chains and lets users filter wallets by trading history, review PnL and timing patterns, build watchlists, and receive alerts when tracked wallets buy, swap, or sell. If you want a broader look at this workflow, their piece on the wallet tracker app workflow for crypto traders shows how traders use watchlists and alerts in practice.

The useful part isn't the alert by itself. It's the ability to narrow the source set before the alert ever reaches you.

A disciplined workflow looks like this:

On-chain tracking is a strong fit for signal-driven trading because it naturally addresses source quality. You're not asking a black-box provider to tell you they have edge. You're inspecting visible blockchain behavior and deciding which actors deserve attention.

That still doesn't remove the need for judgment. A good wallet can take a hedge, seed liquidity, rotate for reasons unrelated to your time frame, or front-run a thesis that no longer exists by the time you see it.

Follow wallets the same way you'd follow a discretionary trader. Learn their tendencies before you mirror their trades.

The traders who get value from on-chain signals don't copy every move. They build profiles. They learn which wallets enter early, which ones scale patiently, and which ones chase heat. That turns wallet activity from raw data into usable signal context.

A workable signal system has four moving parts. Source quality, execution quality, monitoring discipline, and risk limits. Miss one and the rest won't save you.

That's why “set and forget” rarely works in crypto. Even strong automated trading signals need review. The market changes, liquidity changes, and the way participants respond to the same setup changes with them.

A practical build sequence is simple:

If you're still designing the stack itself, this guide on how to make a trading bot is a practical next step for connecting alerts, execution, and control logic.

The traders who last in this space don't chase more alerts. They build a repeatable process around fewer, better ones.

Automated trading signals are trade recommendations generated by algorithms, AI models, or on-chain data systems that identify conditions suggesting a buy, sell, or hold action — without requiring a human analyst to generate each recommendation manually. They work by continuously scanning defined inputs (price patterns, indicator conditions, wallet behavior, volume anomalies) and firing an alert when a pre-set threshold is crossed. A complete automated signal typically includes an entry price, a take-profit level, a stop-loss level, and the timeframe the setup is designed for. The automation handles the monitoring and detection. The judgment about whether to act on any specific signal still belongs to the trader — which is the most important distinction between using automated signals and delegating all trading decisions to a system.

Published accuracy rates across reviewed signal providers in 2026 range from 70% to 92%+ for the most consistently cited providers. NFTEvening's independent review process found that 60-70% of automated traders still lose money despite using signal systems — usually because of poor setup, weak risk management, or unrealistic position sizing rather than because the signals themselves are wrong. A signal with a 75% win rate can still produce losses if the average winning trade returns less than the average losing trade costs, or if the trader sizes losing trades larger than winning ones. Signal accuracy is necessary but insufficient for profitability. The risk management layer — how much capital is committed per signal, where the stop-loss sits, and how the position is sized relative to portfolio — determines whether a 75% win rate produces positive or negative expectancy in practice.

Four checks separate legitimate providers from manipulative ones. First, their signal history should be verifiable in real time — every signal posted before the market moves, with timestamps, including losses, not just winners presented in screenshot form afterward. Second, their claimed win rate should be independently cross-referenced rather than accepted from their own reporting. Third, every signal they publish should include a stop-loss level — a signal without a stop-loss is an incomplete recommendation that leaves risk management undefined. Fourth, their pricing should be proportionate to the actual service — providers claiming 95%+ accuracy and charging a few dollars per month are almost certainly either overstating their accuracy or monetizing through a different mechanism than the subscription fee. A provider with a genuinely verifiable 80% win rate across hundreds of signals has a product worth real money, and their pricing should reflect that.

Yes — Cornix is specifically designed for this. It connects to your exchange account via API, monitors designated Telegram channels for signals in a recognized format, and automatically executes the trade when a signal arrives. The setup requires configuring risk parameters — position size as a percentage of account, maximum simultaneous positions, and stop-loss behavior — before enabling automation on any signal channel. The automation eliminates the execution latency between signal receipt and trade placement, which matters most for shorter-term setups where the entry window closes quickly. The limitation is that Cornix executes based on the signal format it receives — if the signal quality degrades or the provider starts manipulating output, the automation will execute those bad signals faithfully. Human oversight of which channels the automation is pointed at remains essential.

A signal is the decision layer — it identifies a condition and recommends an action. A bot is the execution layer — it takes that recommendation and places the order. The signal answers the question of whether to trade. The bot handles the mechanics of how to trade. They are frequently confused because many platforms combine both functions, but the distinction matters for evaluating what you are actually buying when you subscribe to a signal service. A signal service with no automation integration gives you the recommendation and leaves execution to you. A platform like 3Commas provides both the signal marketplace and the bot infrastructure that executes those signals automatically. On-chain tools like Wallet Finder.ai sit closer to the signal layer — surfacing behavioral signals from profitable wallets that then feed into whatever execution method the trader prefers, manual or automated.

If you want a cleaner way to turn on-chain activity into actionable signals, Wallet Finder.ai can help you track wallets, monitor trades in real time, and build a more disciplined signal workflow before you commit to full automation.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.