Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

June 16, 2026

Your wallet list keeps growing. One trader nails Solana meme rotations, another catches Base launches early, a third farms DeFi yields without blowing up, and your own capital ends up scattered across positions that don't add up to a coherent strategy.

That's where most on-chain portfolios go wrong. Traders think they're diversifying, but they're often just collecting exposures. They own the same risk through different tokens, different wallets, and different chains. When stress hits, everything starts moving together, costs spike, and what looked balanced on paper turns into a pile of correlated bets.

Portfolio optimization is the discipline that fixes that. Not by promising a perfect allocation, but by forcing you to ask better questions. Which positions improve the whole portfolio? Which wallets add unique edge versus duplicated risk? Which trades still make sense after gas, slippage, and turnover?

A sharp DeFi user usually doesn't have an asset selection problem. They have a portfolio construction problem.

You can be good at spotting promising wallets, early narratives, and fresh liquidity. You can still end up with a weak portfolio if your capital sizing is reactive. That happens when each new trade gets added because it looks good on its own, not because it improves the full book.

On-chain markets make this worse. A trader might hold a basket that looks varied on the surface. Some ETH beta, some Solana momentum, a few governance tokens, one yield strategy, maybe a handful of copied wallets. But when volatility expands, those positions can start behaving like one trade.

Practical rule: If you can't explain why each allocation belongs next to the others, you're not managing a portfolio. You're managing a watchlist with capital attached.

Good portfolio optimization starts with a simple shift in mindset. Stop asking, “What should I buy next?” Start asking, “What mix of exposures gives me the best chance of surviving bad conditions while still participating in upside?”

That's the key difference between guessing and building. Guessing focuses on individual winners. Smart portfolio building focuses on interaction effects. A mediocre position can improve a portfolio if it diversifies the rest. A great-looking position can weaken a portfolio if it adds crowded, expensive, unstable risk.

For DeFi traders, that logic matters even more than it does in traditional markets. You're dealing with fragmented liquidity, fast regime changes, wallet-level copy risk, and execution friction that doesn't show up in textbook models. The goal isn't elegant theory. The goal is a portfolio you can hold, rebalance, and defend when the chain gets noisy.

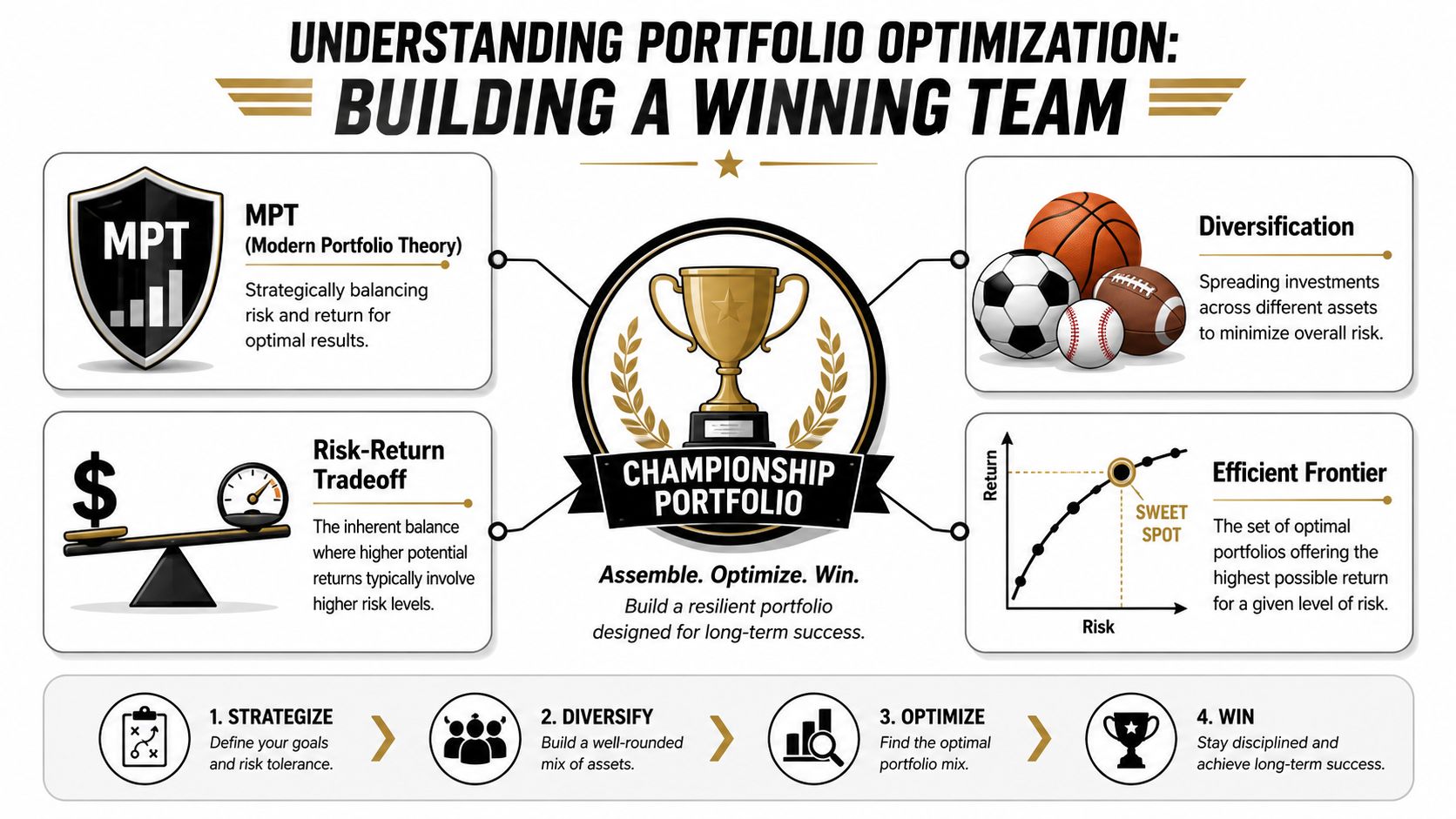

Portfolio optimization didn't start in crypto. It traces back to Harry Markowitz's 1952 paper, which introduced mean-variance analysis and argued that investors should choose portfolios based on the trade-off between expected return and variance, rather than selecting assets one by one, as summarized in this historical review of Markowitz and Modern Portfolio Theory.

That idea still matters because it changed the unit of analysis. The important question stopped being “Is this asset good?” and became “How does this asset behave inside a portfolio?”

A sports team is the easiest way to think about this. If you only recruit strikers, you'll have talent, but not balance. You still need defenders, midfield control, and a goalkeeper. A portfolio works the same way.

Owning several high-upside tokens isn't enough. If they all respond to the same macro move, the same liquidity cycle, or the same risk-on burst, you haven't diversified much. You've just repeated the same role.

That's why diversification isn't “own more things.” It's “combine things that behave differently.”

A practical portfolio usually combines exposures that don't all win and lose at the same time. In traditional markets that could mean equities, bonds, and commodities. In DeFi, it might mean a mix of trend-following wallets, mean-reversion traders, lower-turnover accumulators, and selective protocol exposure with distinct risk drivers.

Most traders naturally focus on upside. Optimization forces you to pair upside with the path taken to get there.

Three ideas sit at the center:

Those inputs combine into a portfolio-level view. A volatile asset isn't automatically bad. A lower-return asset isn't automatically useless. What matters is how each piece changes the total risk and return profile.

The whole point of portfolio optimization is that the portfolio can be better than any single component, if the pieces fit.

That's why institutional investors still organize decisions around volatility, correlation, and diversification. The framework survived because it gives people a common language for comparing very different assets and combining them deliberately.

The efficient frontier is the set of portfolios that offer the highest expected return for a given level of risk. Any portfolio below that frontier is sub-optimal because it gives up return without reducing risk enough, based on the framework described in this efficient frontier implementation walkthrough.

You don't need the math to use the concept. The practical lesson is simple: many portfolios are inefficient because they contain positions that don't improve the trade-off.

A useful way to apply that in crypto is to rank ideas by contribution, not by excitement:

| Question | Weak portfolio habit | Strong portfolio habit |

|---|---|---|

| How is capital allocated? | Added whenever a trade feels attractive | Sized based on role in the total book |

| How are positions judged? | Individually | In combination with all other positions |

| What counts as diversification? | More names | Different behavior under stress |

| What gets removed first? | Losers only | Positions that reduce portfolio efficiency |

For a deeper walkthrough of the classic framework, see Wallet Finder.ai's guide to Modern Portfolio Theory.

A wallet can post strong PnL for a month and still be a bad portfolio. Airdrop exposure, one concentrated beta trade, or a lucky illiquid entry can make weak construction look smart for longer than it should.

What deserves more capital is a return stream you can size, monitor, and stick with through ugly periods.

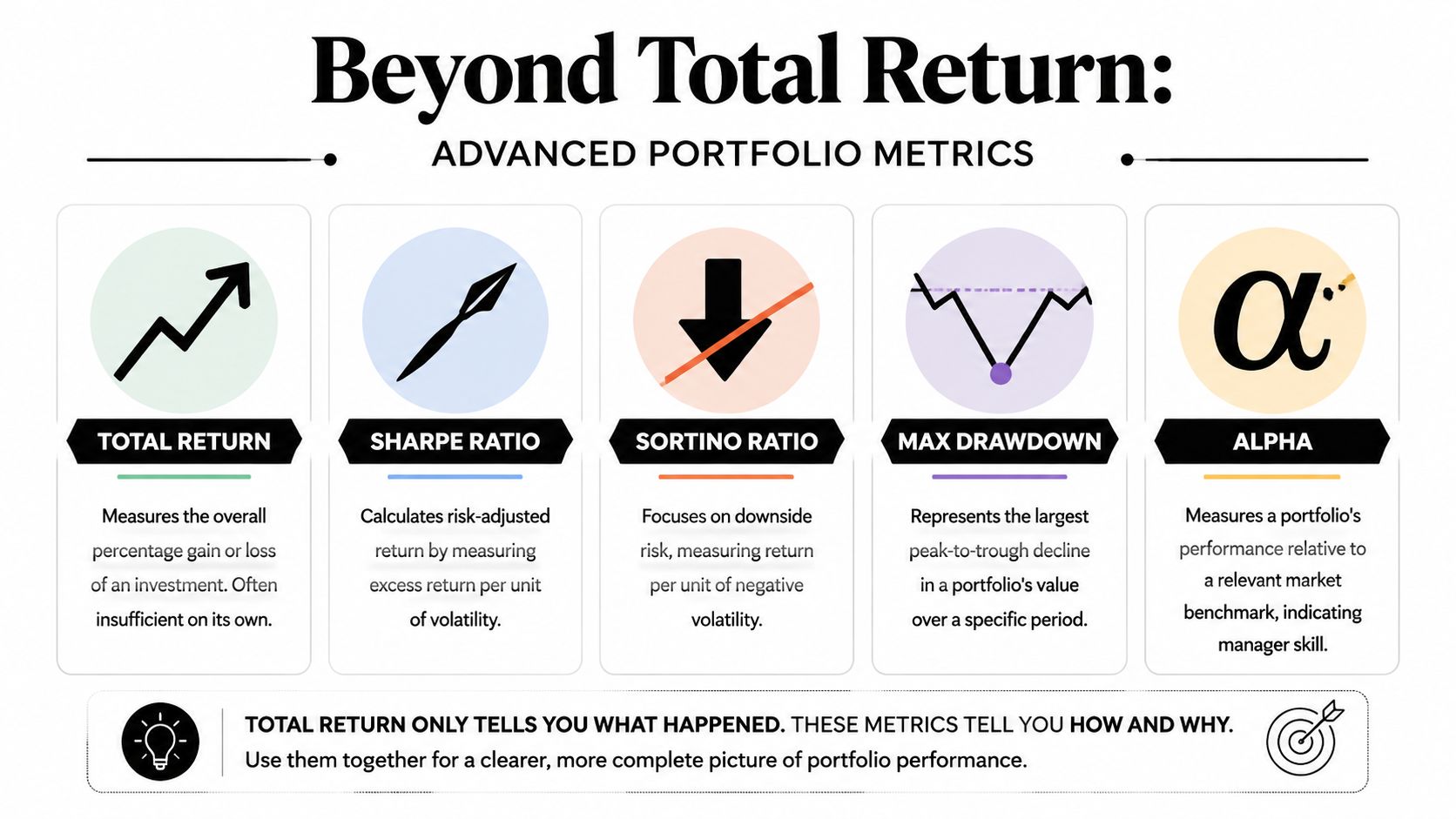

A practical optimization process usually generates many candidate allocations, often through repeated portfolio simulations or constrained weight searches, then ranks them by risk-adjusted performance. The Sharpe ratio remains a useful first filter because it measures return relative to total volatility, a standard approach described in CFI's overview of the Sharpe Ratio.

That matters when comparing portfolios that produce similar returns through very different paths.

Sharpe is not a verdict. It is a screening tool. In practice, I use it to eliminate noisy candidates before spending time on the harder questions.

Sharpe penalizes upside and downside volatility the same way. That makes sense in textbook models. It is less helpful in DeFi, where traders usually tolerate upside bursts and care far more about the losses that force them out of the position.

The Sortino ratio improves that view by focusing on downside volatility. Maximum drawdown adds another layer. It shows the deepest peak-to-trough loss a strategy suffered over the sample, which is often the metric that determines whether a copy-trader keeps following or rage-quits near the bottom.

Here is the practical read:

| Metric | What it helps you see | Where it's useful in DeFi |

|---|---|---|

| Total return | End result | Fast first pass |

| Sharpe ratio | Return relative to total volatility | Comparing portfolio efficiency |

| Sortino ratio | Return relative to downside volatility | Judging asymmetric risk |

| Max drawdown | Worst historical decline | Setting size and survival limits |

| Alpha | Performance relative to a benchmark | Separating beta from actual edge |

Traditional finance metrics need adjustment for crypto reality. Two portfolios can have similar Sharpe ratios, yet one is carrying far more hidden blow-up risk because its losses cluster in stressed conditions, its liquidity disappears during exits, or its turnover burns edge through fees and slippage.

That is why serious portfolio work goes past variance and includes tail-aware measures such as CVaR, along with turnover, execution quality, and capacity. On-chain, a strategy that rebalances well in a spreadsheet can fail after gas, spread, and pool depth are included.

The critical test is simple. Can the portfolio survive the bad regime and still be tradeable?

Three questions help separate clean backtests from usable portfolios:

For a more practical framework on comparing candidate allocations, Wallet Finder.ai breaks down the mechanics in its guide to efficient frontier analysis for portfolio selection.

Classic portfolio optimization assumes cleaner markets than the ones DeFi traders face. That doesn't make the framework useless. It means you have to treat it as a starting point, not an autopilot.

A major challenge for crypto optimization is that returns are fat-tailed and correlations can shift quickly. In stress, assets that looked independent can start moving together, liquidity can vanish, and drawdowns can matter more than average variance, which is exactly the practical gap highlighted in this asset allocation guidance covering optimization limits in crypto-like settings.

Traditional models often behave as if the future will resemble the past closely enough to optimize around historical averages. On-chain markets punish that assumption.

A wallet that trades small-cap launches may have low apparent correlation with an ETH swing trader during quiet periods. In a broad deleveraging move, both can suffer at once. A liquidity provider may look stable until price path and withdrawal timing turn the position into a very different risk profile than variance suggested.

Here's the contrast in plain terms:

| Factor | Traditional Finance Assumption | DeFi & Crypto Reality |

|---|---|---|

| Return distribution | Moves are often modeled with relatively stable distributions | Returns can be fat-tailed, with extreme moves arriving fast |

| Correlation | Relationships are somewhat stable over estimation windows | Correlations can flip quickly, especially in stress |

| Liquidity | Deep markets support cleaner execution | Liquidity can disappear, spreads widen, and slippage changes realized outcomes |

| Rebalancing | Trading costs are often easier to model | Gas, slippage, and bridge friction can make frequent rebalancing expensive |

| Asset identity | A stock is a stock | Token risk includes protocol design, custody path, and smart contract exposure |

| Market hours | Sessions create natural pauses | Crypto trades continuously across venues and chains |

| Risk measure | Variance can be a workable shorthand | Path dependency and tail loss often matter more than average variance |

Optimization outputs can look authoritative because they produce clean weights. That precision is often fake.

One practical rule of thumb in mean-variance optimization is that a universe of 500 securities requires at least 500 observations per security, which at monthly frequency implies roughly 42 years of data, according to this discussion of estimation limits in portfolio optimization. That's why many practitioners prefer more dependable approaches such as inverse-volatility or equal-risk-contribution when correlations are unstable or hard to estimate.

Crypto traders should take that seriously. You don't have decades of stable monthly data for many on-chain assets, and even when you have history, the market structure changes so fast that old relationships can become less useful.

The harder your inputs are to estimate, the less you should trust a highly optimized output.

That doesn't mean you abandon optimization. It means you use simpler constructions, wider ranges, and stronger constraints.

In practice, DeFi portfolio optimization works better when you treat it as risk management under uncertainty.

That usually means:

The common failure mode is easy to spot. A trader optimizes for expected return and historical covariance, then discovers that the live portfolio behaves differently because execution friction, crowding, and market stress were left out.

In DeFi, “optimal” is only meaningful if the portfolio survives contact with the chain.

The cleanest way to apply portfolio optimization in DeFi is to stop thinking only in terms of tokens and start thinking in terms of sources of edge. On-chain, one of the most useful units is the wallet itself.

A copied wallet is a strategy stream. It has timing habits, turnover patterns, preferred ecosystems, holding periods, and reaction speed. When you allocate across wallets instead of blindly chasing the single hottest one, you can build a more resilient book.

A common rule in portfolio analysis is that about 80% of value can come from roughly 20% of items, and the same logic helps identify the core set of assets or wallets that deserve the closest risk management, as described in this discussion of concentration effects in portfolio analysis.

Applied to copy trading, that means your first job isn't to find every profitable wallet. It's to identify the smaller subset that drives differentiated performance.

Use a workflow like this:

Build a candidate list across styles

Don't fill your list with five wallets that all trade the same meme cycle. Include different behaviors. One momentum trader, one earlier accumulator, one lower-frequency swing wallet, one trader with stronger exit discipline, one strategy focused on a different chain.

Remove obvious duplicates

If several wallets enter the same names around the same time with similar sizing, they may be one exposure wearing different labels.

Screen for implementation fit

A wallet can be impressive and still be unusable for copying if it trades too fast, sizes too aggressively, or depends on conditions you can't replicate cleanly.

For ongoing tracking and exportable research around wallet activity, transaction history, and watchlists, a dedicated on-chain tracker such as Wallet Finder.ai's DeFi portfolio tracker can fit into this process.

Once you have a workable pool, allocate by role.

A practical structure often includes:

Core exposure

Lower-turnover wallets or strategies that you can reasonably mirror without constant adjustment.

Satellite exposure

Higher-upside, faster wallets that can add return but shouldn't dominate risk.

Cash or reserve capital

Dry powder matters on-chain because conditions change quickly and execution windows can be short.

Many traders achieve immediate improvement. They stop putting oversized capital behind the single top-ranked wallet and instead build a portfolio of traders.

That changes the questions you ask:

| Allocation question | Weak approach | Better approach |

|---|---|---|

| Which wallet gets capital? | The highest recent PnL wallet | The wallet that adds unique exposure |

| How much should it get? | Similar size to every copied wallet | Size based on volatility, turnover, and overlap |

| When do you remove it? | After a bad streak | After role failure, style drift, or correlation spike |

| What do you monitor? | Wins and losses | Behavior, overlap, and execution quality |

The hidden edge in optimization is often subtraction.

If your tool lets you export wallet histories, use that data offline to compare holding overlap, trade timing, and rough behavioral correlation. You don't need an institutional stack to learn something useful. Even simple comparisons can reveal whether two wallets are distinct or effectively one strategy.

The best addition to a portfolio is often the wallet that looks less exciting on its own but behaves differently from everything else you already hold.

After you identify overlap, tighten the list. Keep the wallets that broaden the book. Cut the ones that only increase noise or duplicate risk.

A useful walkthrough of portfolio thinking in live trading sits below.

Rebalancing in DeFi shouldn't be automatic just because weights moved. Every rebalance has a cost.

Use selective rules instead:

The right operating model is closer to a risk desk than a scorecard. You're not just following winners. You're maintaining a system of differentiated exposures that still make sense after slippage, fees, and real execution constraints.

Portfolio optimization is useful because it forces discipline. It becomes profitable only when that discipline survives live conditions.

That's the key mindset shift for DeFi traders. The job isn't to produce one perfect set of weights from historical data. The job is to build an allocation process that can handle unstable correlations, fat-tailed risk, and execution friction without constantly breaking.

A major practical question is whether portfolio optimization still improves outcomes after costs and estimation error. Practice-oriented guidance warns that investors should stress test portfolios rather than rely only on historical outputs, and that a simpler allocation can sometimes be more stable, as discussed in this practical critique of efficient frontier outputs.

That maps directly to crypto.

The strongest on-chain portfolios usually share a few traits:

A messy but resilient portfolio beats a mathematically elegant one that falls apart after fees, stress, or crowding.

If you're uncertain, simplify. Use fewer inputs. Trust historical optimization outputs less when the market regime is unstable. Give more weight to downside control, position limits, and execution quality.

That's still portfolio optimization. It's just portfolio optimization adapted for the chain instead of the classroom.

If you want to put this into practice, start by building a small basket of distinct on-chain strategies, track their overlap, and review how they behave together over time. Wallet Finder.ai can help you discover active wallets, inspect trading histories, set alerts, and turn scattered wallet watching into a more structured portfolio process.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.