Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

June 15, 2026

Your wallet probably didn't become a portfolio on purpose.

It became a pile. A little BTC because it felt responsible. Some ETH because everything routes through it. A few Solana names because momentum looked real. Airdrops you forgot to sell. LP positions you can't explain without opening three tabs. Then one meme coin that somehow became a meaningful percentage of your net worth.

That kind of sprawl is normal in crypto. It's also why many DeFi traders feel busy but not structured. They track entries, narratives, token release schedules, and influencer flows, yet they still can't answer a basic question: how much risk is the whole wallet taking?

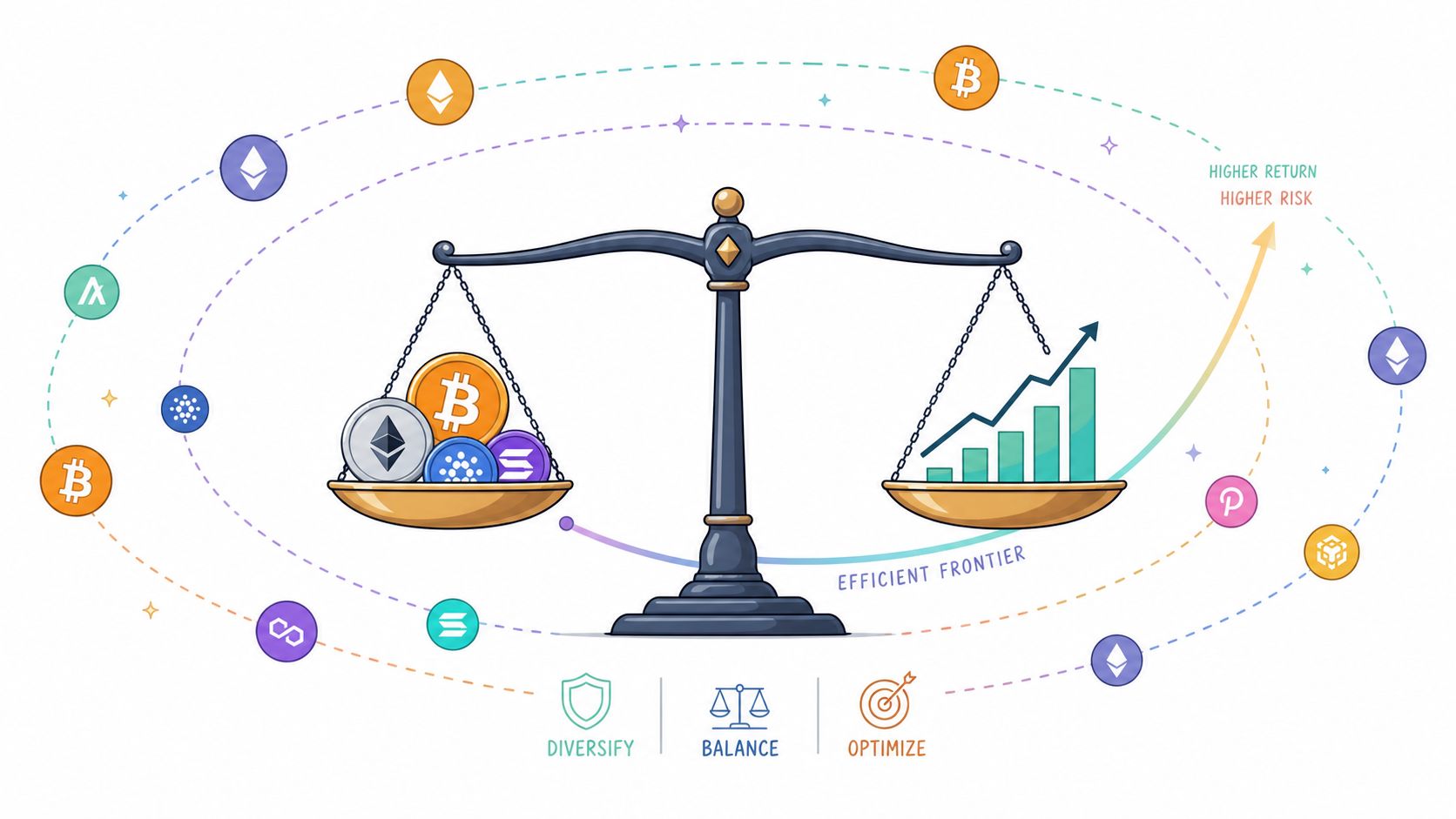

Modern Portfolio Theory gives you a clean way to think about that. It came from traditional finance, but the core idea travels well to crypto. Don't judge each token in isolation. Judge each position by what it does to the whole portfolio.

You check your wallet after a rough week and the labels all look different. ETH staking. A Solana perp hedge. Two LP positions. A governance token you meant to sell. A meme coin that kept running, so you let it ride. Then the market drops and the whole thing starts moving like one oversized bet on crypto beta.

That is the problem Modern Portfolio Theory was built to address.

The model came out of traditional finance, but the habit it teaches fits DeFi surprisingly well. Stop asking whether a token looks good by itself. Ask whether adding it makes the whole wallet stronger, weaker, or just more crowded with the same risk. A position can have strong fundamentals, good momentum, and a clean catalyst calendar, yet still be a poor addition if it rises and falls with everything else you own.

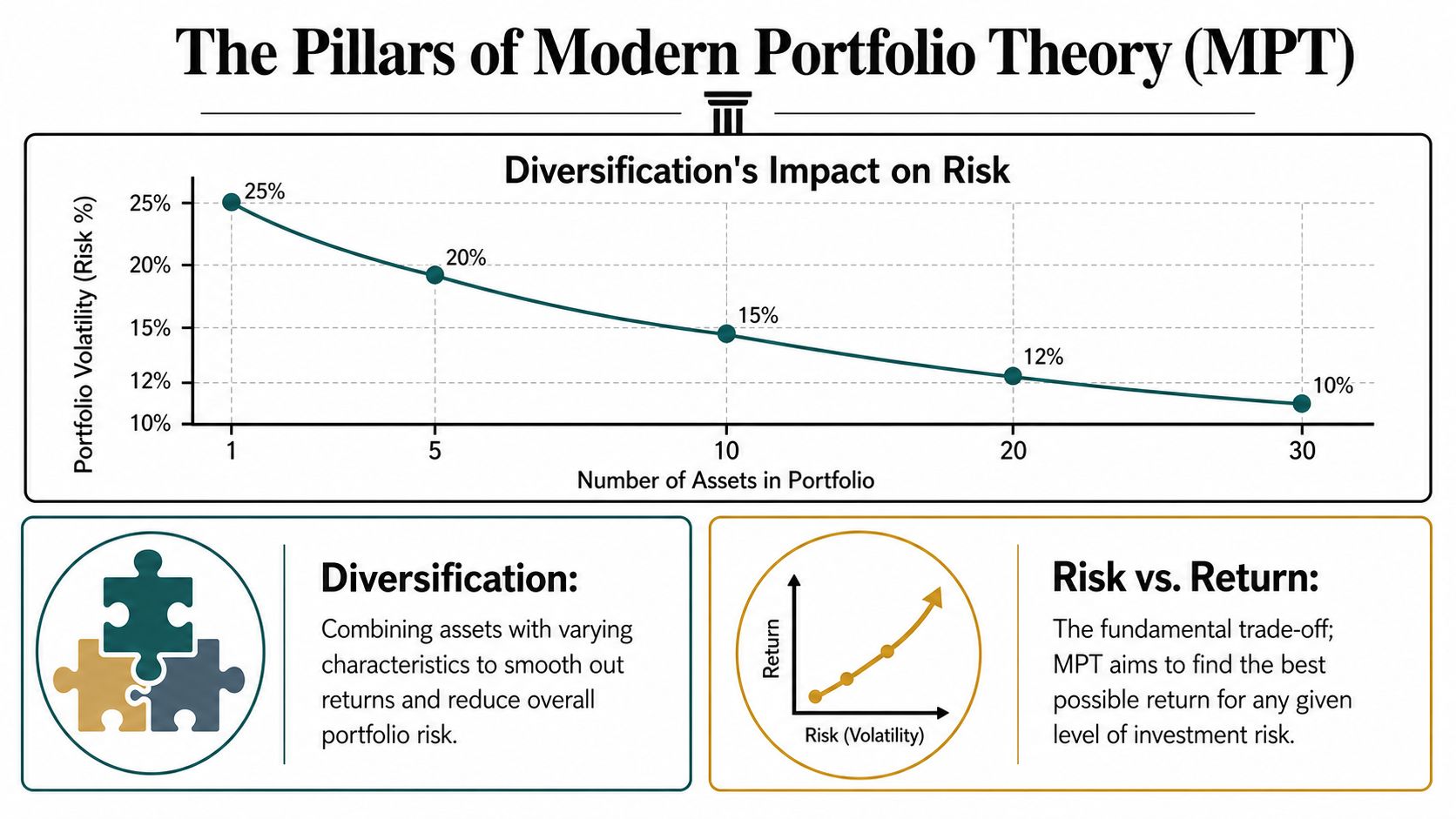

Harry Markowitz introduced this framework in 1952, and the work later earned a Nobel Prize. The idea was simple enough to survive seven decades of market change. Portfolio risk depends on how positions move together, not just on how risky each position looks on its own.

That point matters in crypto because wallets often look diversified on the surface while remaining concentrated underneath. Five tokens across three chains can still be one trade if they all depend on the same conditions: easy liquidity, rising sentiment, and traders reaching for risk.

A useful analogy is a validator set. Ten validators do not give you much protection if they all run the same client, in the same region, behind the same infrastructure provider. Ten tokens do not give you much protection if they all break for the same reason.

You do not need to become an academic optimizer. You need a better mental model.

Start with a practical shift:

That is the main lesson. Modern Portfolio Theory does not promise a portfolio that never hurts. It gives you a way to turn a pile of on-chain positions into a system with a reason behind it.

Most stock-and-bond explainers stop there. For DeFi, the more useful question is how to apply that logic when correlations jump, narratives rotate overnight, and your exposures are spread across wallets, protocols, and chains. That on-chain translation is where this framework becomes practical instead of academic.

Open a typical DeFi wallet after a strong month and the spread can look healthy. A little BTC. Some ETH. A few L1 bets. A lending token. A perp DEX name. Maybe a meme coin that got out of hand. On-chain, that feels diversified. Under stress, many of those positions can still move like one crowded trade.

That gap between how a portfolio looks and how it behaves is where Modern Portfolio Theory becomes useful for crypto.

MPT starts with a simple point. Portfolio risk depends on how holdings interact, not just on how many you own.

That matters a lot more in DeFi than in stock-and-bond examples. Two tokens can live on different chains, have different communities, and still react to the same drivers. Liquidity dries up. Beta gets sold. Funding conditions tighten. A regulatory headline hits anything that smells speculative. If the same shock moves both assets, holding both does less for you than the wallet view suggests.

A better analogy is a validator set, not a bag of coin logos. If every validator depends on the same cloud provider, the count looks distributed but the failure mode is concentrated. Portfolios work the same way.

So diversification means adding exposures with meaningfully different behavior. In practice, that can include assets or strategies that respond differently to macro moves, rate expectations, on-chain activity, or volatility spikes. Sometimes the best diversifier is not another high-upside token. It is dry powder, stable yield, or a lower-volatility position that keeps you from selling risk into a drawdown.

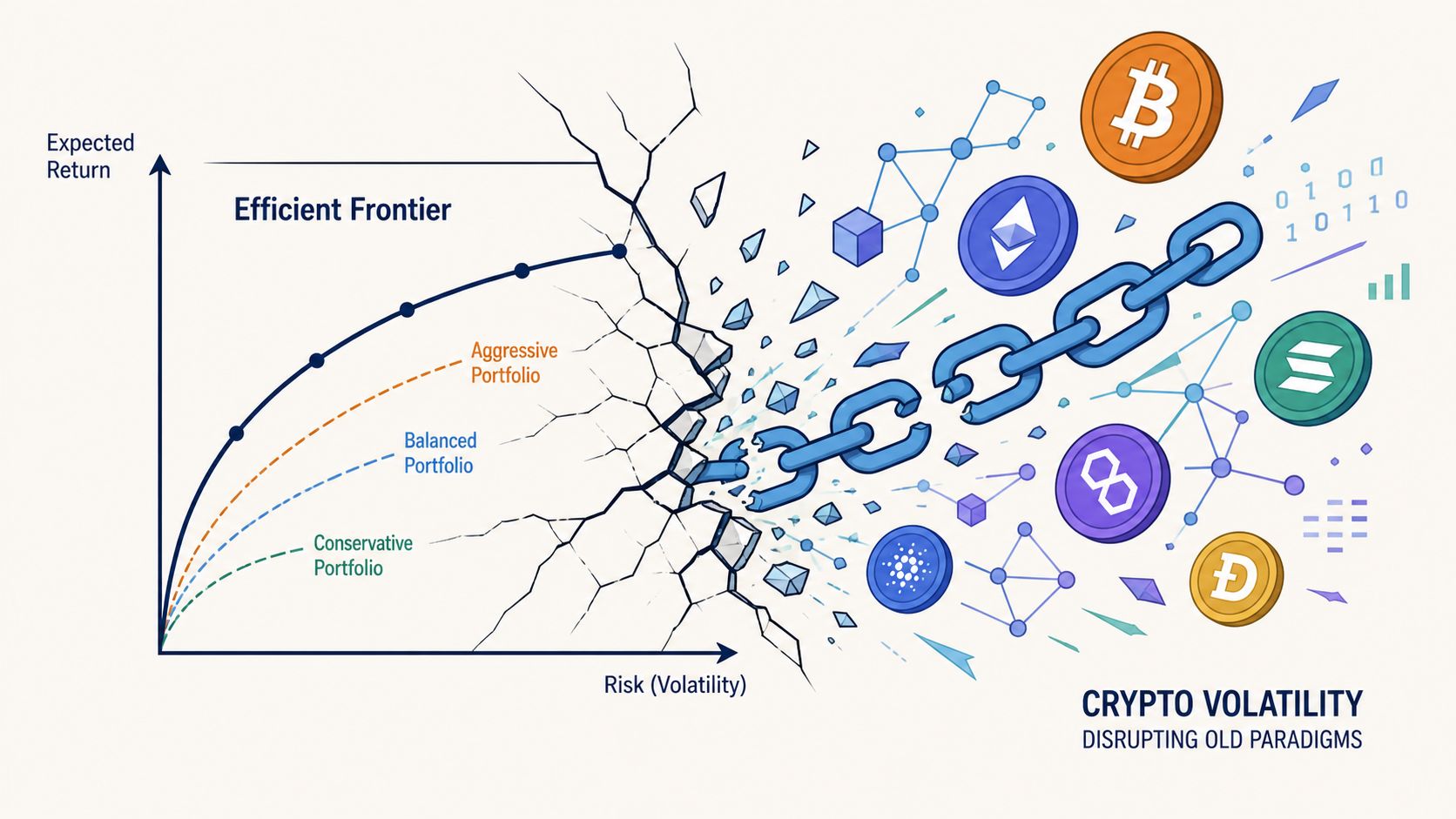

The second core idea is the efficient frontier. It is the set of portfolios that offer the highest expected return for a given level of risk, or the lowest risk for a given expected return.

That sounds technical, but the intuition is straightforward. If Portfolio A and Portfolio B target similar returns, and A gets there with smaller swings, B is hard to defend. If two portfolios take similar risk, but one has stronger expected return, the weaker one is just an inferior mix.

The efficient frontier is useful because it shifts the conversation away from hero assets and toward combinations. A token can be attractive on its own and still make your total portfolio worse if it adds a lot of overlap with positions you already hold.

A few implications follow:

If you want a simple way to pressure-test that tradeoff, a Sharpe ratio calculator for crypto portfolios helps compare return against volatility at the portfolio level.

Skepticism is healthy here because MPT gets oversold. It does not promise safety. It does not tell you drawdowns disappear. It gives you a cleaner way to ask whether your current mix is taking more risk than necessary for the return you expect.

That is a narrower claim. It is also the one that survives contact with crypto.

| Common belief | What MPT actually says |

|---|---|

| More tokens means more diversification | More distinct return drivers means more diversification |

| A low-volatility asset makes the whole portfolio safer | Portfolio risk depends on how each holding moves with the others |

| The highest-conviction asset should always get the most capital | Position size depends on how that asset changes total portfolio risk |

Practical rule: If two positions usually win and lose for the same reason, size them like one exposure until market behavior proves otherwise.

Most MPT explainers stop at stocks, bonds, and neat textbook correlations. For an on-chain portfolio, the better use of the framework is simpler. Treat every new token, pool, or strategy as a change to the behavior of the full wallet, not as an isolated bet.

Under the hood, Modern Portfolio Theory is a mean-variance optimization problem. The optimizer either minimizes portfolio variance for a target expected return or maximizes expected return for a fixed risk budget, as explained in this technical overview of mean-variance optimization.

That sounds academic, but the moving parts are familiar.

Expected return is your working estimate of what an asset might deliver. In crypto, that estimate is noisy, but you still need one. Otherwise every portfolio discussion becomes vibes and screenshots.

Variance measures how widely returns swing around that expectation. In practice, traders usually think in standard deviation because it's easier to interpret, but the point is the same. Wider swings mean more uncertainty.

A simple trader translation:

Most beginners focus on standalone volatility. MPT emphasizes covariance, which captures how assets move together. This is the part many crypto traders intuitively understand but rarely formalize.

If two assets both rip and dump at the same time, combining them doesn't help much. If they move differently, the portfolio can become less volatile than either position makes it look on its own.

That's why a portfolio can hold volatile assets and still behave better than expected. The interaction terms matter.

A portfolio's risk doesn't come from adding up scary-looking tokens. It comes from how their return streams combine.

For a two-asset portfolio, the risk isn't just weight times risk plus weight times risk. There's also the covariance term. That extra term is the reason diversification works mathematically.

You don't need to calculate covariance matrices by hand to benefit from the idea. You do need to stop thinking like this:

That conclusion can be wrong because co-movement matters.

Most DeFi traders won't run institutional optimizers daily, but they can still borrow the logic:

The math in modern portfolio theory isn't there to impress anyone. It's there to force a more honest question: what is this new position doing to the total risk of my wallet?

That's the question quants ask every day. DeFi traders should too.

Modern Portfolio Theory is useful. It's not innocent.

Crypto exposes the weak spots quickly because the model depends on inputs and assumptions that can get ugly in live markets.

MPT is a single-period, input-sensitive model. It leans on estimates for expected returns, volatilities, and correlations, usually taken from historical data. When those estimates shift, the “optimal” portfolio can shift with them. That issue is especially sharp in crypto, where historical samples are shorter and market structure changes fast, as described in this discussion of MPT's input sensitivity and crypto tail risk.

That means a clean optimizer can produce dirty outputs. Tiny changes in assumptions may lead to very different weights.

MPT often uses variance as the proxy for risk. That works well enough in some contexts, but DeFi traders know the missing categories immediately:

A token can look statistically manageable right up until the moment a bridge freezes, liquidity disappears, or the market reprices a governance exploit. Variance doesn't capture that well.

This is the classic failure mode in crypto. In normal conditions, segments can look distinct. In stress, everything starts trading as risk. The diversification you thought you had gets weaker precisely when protection matters most.

That doesn't make diversification useless. It means you should treat historical correlation as a moving estimate, not a law of nature.

| Assumption in classic MPT | What often happens on-chain |

|---|---|

| Inputs are reasonably stable | Inputs can shift fast with regime changes |

| Variance captures meaningful risk | Tail events and structural risks matter a lot |

| One-period optimization is enough | Traders manage flows, exits, and reinvestment over time |

Don't use Modern Portfolio Theory as an autopilot. Use it as a checklist, then stress it against how crypto actually breaks.

There's another practical limitation. Many on-chain investors aren't making one clean allocation decision for one time period. They're adding funds, farming, rotating, harvesting, withdrawing, and reacting to incentives. That's not the world the basic model was built for.

For crypto, the right posture is skeptical respect. Use MPT to organize your thinking. Don't let it convince you that measured volatility equals understood risk.

Theory helps only if it changes what you do with your next allocation. In DeFi, that usually means taking a messy set of wallets, protocols, and tokens, then turning it into a risk map you can manage.

Start with behavior, not labels.

Most crypto portfolios improve as soon as you stop treating every token as unique. Group holdings into a few economic buckets based on how they tend to react.

A simple framework:

This isn't perfect classification. It's good enough to expose concentration.

You don't need false precision. Start with rough expectations about co-movement, then test them against your own history.

| Asset Class A | Asset Class B | Expected Correlation | Rationale |

|---|---|---|---|

| BTC | ETH | High | Both often respond to broad crypto risk sentiment, though ETH may carry additional ecosystem-specific drivers. |

| BTC | Stablecoins | Low | Stablecoins are typically used as reserve capital or settlement assets rather than directional market exposure. |

| ETH | DeFi governance tokens | High | Many DeFi tokens inherit Ethereum ecosystem risk and user activity cycles. |

| Solana ecosystem tokens | Ethereum DeFi tokens | Medium | They can share market beta while still reacting to different chain-specific catalysts. |

| Meme coins | Stablecoins | Low | Meme coins are speculative risk assets, while stablecoins are usually held for optionality and capital preservation. |

| Yield strategies | Meme coins | Low to medium | Carry-focused positions may behave differently from pure speculation, but stress periods can still pull everything toward the same direction. |

Those labels are heuristics, not laws. The point is to ask whether you're mixing behaviors or just collecting versions of the same trade.

Run your wallet through a repeatable process.

A useful helper for this step is a crypto diversification tool for portfolio review.

On-chain traders have an advantage traditional investors didn't have when MPT was born. You can observe real wallet behavior in near real time.

That makes wallet selection a practical proxy for strategy selection. Instead of asking only which tokens to own, you can ask which types of operators you want exposure to. One wallet may run concentrated momentum. Another may trade event-driven launches. Another may stay mostly in stables and rotate selectively.

Used carefully, a platform such as Wallet Finder.ai can help identify wallets with different trading styles across chains, recent activity, sizing patterns, and realized behavior. That gives you a way to blend strategy exposures rather than blindly mirror one aggressive operator.

If you mirror wallets, diversify the decision-makers too. One brilliant but hyper-concentrated wallet can still blow up your total portfolio behavior.

A simple application looks like this:

Later in your process, it helps to review a live example of how traders monitor and act on wallet behavior:

Modern portfolio theory doesn't tell you which token will outperform next month. It gives you a framework for combining exposures with intention.

For a DeFi-native portfolio, that usually means:

That's already a major upgrade from most crypto portfolio construction. You're no longer asking only, “Can this coin go up?” You're asking, “What job does this position perform inside the whole wallet?”

No version of Modern Portfolio Theory will make crypto neat. Markets gap. Correlations jump. Tail risks show up from places the spreadsheet never modeled.

That's fine. The point isn't perfection. The point is to stop running a wallet like a bag of unrelated impulses.

Modern portfolio theory is most useful as a mental model. It teaches you to think in terms of interaction, tradeoffs, and total portfolio behavior. That's valuable even if you never run a formal optimizer.

Keep the core lessons:

A smarter crypto portfolio is still volatile. The difference is that the volatility is chosen, sized, and monitored.

For DeFi traders, the modern version of this framework lives at the intersection of old theory and live on-chain data. Use the theory to structure your thinking. Use current wallet, trade, and protocol data to reality-check it. That combination won't remove uncertainty, but it will make your risk more intentional.

If you want to turn these ideas into a repeatable workflow, Wallet Finder.ai lets you inspect on-chain wallets, trading histories, position behavior, and strategy patterns so you can compare exposures and build a more deliberate crypto portfolio.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.