Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

July 11, 2026

Price realization is the price you get for a trade after all costs, versus the price you expected. In practice, it can sit below 100% when value leaks through discounts, rebates, terms, or mix, and it can go above 100% when surcharges or mix shifts lift what you capture.

You know the setup. A swap looks clean in the DEX UI. The quoted output is attractive, the chart agrees with your thesis, and the trade seems profitable before you click confirm. Then you check the wallet after settlement and the result is worse than the screen implied.

That gap is where traders lose edge.

In DeFi, it's common to blame “slippage” and move on. That's too shallow. The key question is whether your execution converted the price you aimed for into the price your wallet realized after gas, pool fees, routing choices, price impact, and any other concession buried inside the trade path. That's the practical meaning behind the price realization definition.

If you trade size, rotate fast, or copy smart wallets, this metric matters more than many headline PnL screenshots. A trader can be directionally right and still realize mediocre outcomes. Another can trade in choppy conditions and still keep more of the intended price because they manage execution better.

A common DeFi mistake is treating the displayed quote as the trade result. It isn't. It's only the starting reference.

On-chain trading inserts friction at several points between intention and settlement. You see one number before submitting. The chain records another after the transaction lands. Your wallet balance reflects a third reality, because the wallet includes execution costs the quote didn't fully represent in the way you mentally modeled the trade.

Three leaks show up again and again:

Practical rule: If your P&L review starts from token price alone, you're already missing part of the trade.

This is why price realization is useful. It forces you to compare what you wanted from the trade with what you captured. That sounds simple, but it changes how you diagnose mistakes.

A trader who only tracks entry and exit price sees direction. A trader who tracks price realization sees execution quality.

That distinction matters when you're reviewing swaps on Uniswap, Jupiter, Raydium, 1inch, or CowSwap. Two traders can make the same directional call on the same token pair and end up with meaningfully different wallet outcomes because one traded at a better time, used a tighter method, split size more intelligently, or avoided hostile conditions.

Use price realization as an execution lens. It tells you whether the issue was your market view, your trade mechanics, or both.

You swap 50,000 USDC into ETH, the quote looks fine, and the trade confirms. Later, your wallet value says you captured less than the setup suggested. Price realization is the metric that explains that gap.

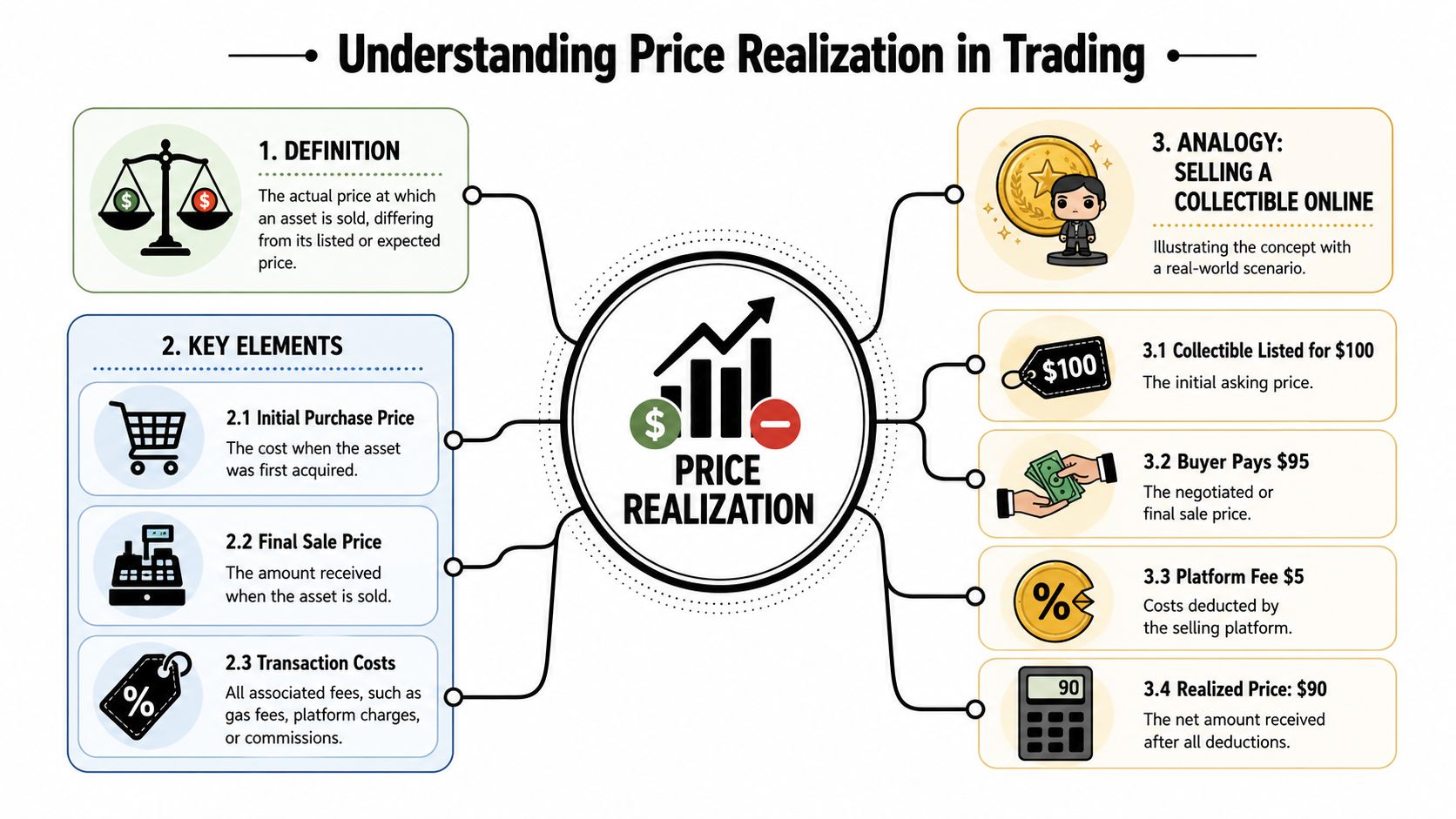

The cleanest definition is this: price realization measures the price you captured relative to the price you meant to capture.

That sounds simple until you try to measure it on-chain. In DeFi, the hard part is rarely the math. The hard part is choosing the right benchmark, then adjusting for what the trade really cost you. If the benchmark is weak, the metric is weak. If the benchmark matches the trade you were trying to execute, price realization becomes a useful P&L diagnostic instead of a vague ratio.

Traditional pricing explanations often frame price realization as the share of a list or target price collected after discounts, rebates, or credits, as noted in Lusha's overview of price realization. That framing is fine as a starting point. For traders, it misses the practical question that decides whether the number means anything. What price should count as the reference?

Say you planned to buy ETH with USDC on a DEX aggregator.

Your screen showed a pre-trade quote. Your order then routed across multiple pools, paid protocol fees, consumed gas, and moved enough size to shift execution. The price on the chart was one thing. The price your wallet captured was another.

That second number is what price realization is trying to isolate.

At a working level, price realization has three parts:

ComponentWhat it means on-chainReference priceThe price you expected, targeted, or used as your execution benchmark before the tradeRealized priceThe value you ended up with after the transaction settledAdjustmentsGas, swap fees, slippage, routing costs, MEV effects, and other execution leakage

Used properly, the process is simple:

Traders often misread their own performance. A swap can look bad against a visible market quote and still be acceptable against a realistic executable benchmark for that trade size and liquidity profile. The opposite happens too. A trader can feel good about a fill because it stayed near the screen price, while gas, fees, and routing drag turned a decent idea into a weak trade.

A related mistake is treating market price and executable price as interchangeable. They are not. This guide to true market price in crypto trading is useful if you want to tighten that distinction before reviewing execution quality.

Institutional transaction cost analysis uses a specific benchmark worth adding to the three already covered in this guide: arrival price, the market price at the exact moment you decided to trade, before your order started interacting with the market at all.

The distinction from a pre-trade quote matters more than it sounds. A quote captures the price right before you click confirm, which already reflects a market that may have moved since you first decided to act. Arrival price captures the earlier moment, giving you a cleaner read on how much value was lost to delay and hesitation versus how much was lost to execution mechanics once the order was actually placed. The gap between arrival price and your final realized price is sometimes called implementation shortfall, a term borrowed directly from institutional equity trading that maps cleanly onto on-chain execution.

For a trader who researches a setup, waits for a specific level, then executes, arrival price is often the more honest benchmark than a pre-trade quote, since it captures the full cost of the entire decision-to-execution window rather than just the final routing step. Use it when you want to separate "I was slow to act" from "my execution was poor" as two distinct, measurable problems rather than one blended number.

For most on-chain trading reviews, one of these benchmarks works:

Use the wrong benchmark and the metric becomes cosmetic. Use the right one and price realization tells you whether the loss came from your thesis, your execution, or friction inside the route itself.

Traders often use nearby terms as if they mean the same thing. They don't. That confusion causes bad reviews and bad decisions.

Price discovery belongs to the market.

It describes how the market forms a price, especially in fresh or thinly traded assets. You care about it when a token is launching, repricing fast, or trading in uncertain liquidity.

Average execution price belongs to the order.

It tells you what your order got on average, especially when the trade was filled in pieces or across multiple pools.

Price realization belongs to your economic outcome.

It asks whether the trade delivered the value you intended once all the friction is counted.

This is why a trader can report a decent average execution price and still have weak price realization. Maybe the fills were acceptable, but gas was ugly, the route was inefficient, or the reference benchmark was too optimistic.

Some traders use slippage as a stand-in for the whole problem. Slippage is only one contributor.

A better mental model looks like this:

If you need a tighter definition of one major leak in that chain, this explainer on what slippage means in crypto is worth reviewing.

A vocabulary problem becomes a P&L problem fast. If you name the metric wrong, you usually fix the wrong thing.

When you audit trades, keep the terms separated. It's the only way to know whether the market moved against you, your order design was weak, or your realized outcome got shaved down by execution mechanics.

A rising token chart doesn't guarantee good execution. Traders learn that the hard way.

In volatile markets, headline price can rise while realized price falls. Net price realization guidance emphasizes that realized price should be decomposed into elements like discounts, rebates, promo spend, freight or terms, and mix. It also notes that the metric can fall below 100% from leakage or move above 100% from surcharges and mix shifts, which is why a static ratio often hides the actual cause of underperformance. That framework appears in Umbrex's net price realization guide.

The DeFi translation is straightforward. A token can rally while your actual trade economics worsen because the route, fees, slippage, timing, and position mix all moved against you.

Some habits consistently help:

Other patterns show up in losing reviews:

When a swap underperforms, don't ask one broad question. Split it up.

DriverWhat to inspect on-chainQuote gapDifference between pre-trade expectation and executed outputExplicit feesDEX fee, aggregator fee, bridge or route fee if anyNetwork costGas in native token and its economic value at execution timeMarket impactWhether your order size moved the pool materiallyMix effectWhether you're comparing different token sets, venues, or liquidity conditions

This decomposition matters because otherwise you'll “fix” the wrong thing. You might blame the DEX when the issue was your order size. You might blame slippage when the issue was a poor benchmark. You might blame volatility when the route itself was vulnerable.

For traders worried about hostile execution, review practical MEV protection methods in crypto trading. Better protection won't solve every pricing problem, but it can remove one avoidable source of leakage.

The term demonstrates its utility. You don't need a perfect institutional stack to measure it. You need a repeatable process.

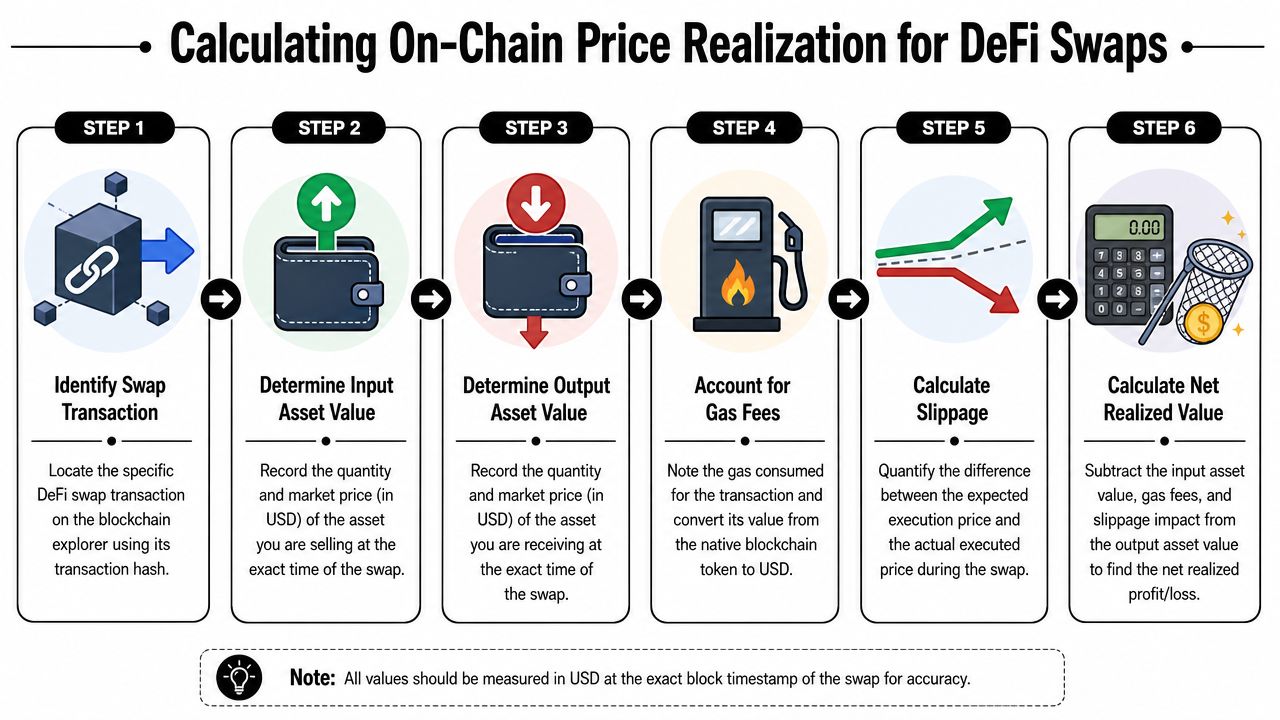

Start with one swap. Pick a transaction on Uniswap, Jupiter, Raydium, 1inch, or another venue you use regularly. Your job is to compare the value you expected from the trade with the value you realized after execution.

To make the process easier to follow, use this visual flow first.

Suppose you swap one major asset for a stablecoin pair on a DEX. The interface shows an expected output. After the trade confirms, the explorer shows slightly less stablecoin received than quoted. You also paid gas. The swap fee is embedded in the route economics.

Your review looks like this:

If that net realized value is meaningfully below the benchmark you chose, the trade had poor price realization. If it's close, your execution was efficient. If it beats the benchmark, you captured unusually favorable execution.

Don't obsess over whether one tiny component belongs in a separate bucket. What matters is using the same method every time.

A simple journal can tell you a lot:

That last field matters more than people think. Many bad trades are not “bad luck.” They're oversized relative to available liquidity.

For a quick walkthrough of the broader mechanics behind DeFi swap execution, this video is useful before you build your own review template.

What works:

What doesn't:

If you trade frequently, consistency beats sophistication. A basic but disciplined review process will improve your decisions faster than a complicated spreadsheet you stop updating after a week.

Most traders don't need another abstract metric. They need examples of what better execution looks like in the wild.

That's where wallet-level analysis becomes useful. If you can inspect profitable on-chain traders with full trade history, you can reverse-engineer the habits behind cleaner realization. You won't get a single magical score, but you will get the raw material that matters more: entries, exits, timing, position sizing, venues used, and the order patterns that preserved value.

When you study strong wallets, focus on behavior instead of headline gains.

That kind of review often explains why two traders with the same market idea realize very different outcomes.

A useful workflow looks like this:

Research angleWhat you can inferExact entry and exit pointsWhether the trader avoids bad liquidity windowsTrade sequenceWhether they scale in and out instead of crossing the spread all at onceChain and token preferencesWhether they selectively avoid poor execution environmentsHistorical consistencyWhether the good outcomes come from process or isolated luck

Price realization improves through habit. Traders usually don't fix it by memorizing a definition. They fix it by changing where, when, and how they execute.

Good execution leaves footprints on-chain. If you know how to read them, you can copy the process, not just the trade.

For copy traders, this is especially important. Mirroring a wallet after the fact without understanding its execution style can turn a good original trade into a worse copy. Studying the wallet's behavior first gives you a better chance of preserving the economics that made the original trade worthwhile.

Yes. It can happen when your execution beats the benchmark you chose. On-chain, that usually means the swap cleared at a better effective price than your reference, or your benchmark was too conservative for the route and size you traded.

That result is possible, but it deserves a second look. In DeFi, a reading above 100% can reflect genuine price improvement, but it can also come from weak benchmarking, missing gas costs, or comparing your fill to the wrong quote source.

Yes, and the difference shows up in P&L fast.

A market-style swap usually gets the trade done, but you accept more slippage risk and more exposure to thin liquidity. A limit-style order gives you tighter price control, but the order may sit unfilled while the market moves away. Traders are choosing between execution certainty and price discipline. On-chain, that choice also depends on pool depth, volatility, and how quickly a quoted route becomes stale.

Yes. Entry quality sets your cost basis, and exit quality determines how much of the gain you keep.

A long-term view does not cancel out a weak fill. If you overpay getting into a token, you start the position behind. If you sell into poor liquidity months later, part of your paper gain disappears during execution.

They confuse price realization with headline slippage, quoted price, or token performance after the trade.

Price realization is about what you captured versus what was reasonably available at the time you traded. To measure it properly, check the executed amount, fees, gas, route quality, pool liquidity, and the benchmark timestamp. If one of those inputs is wrong, the metric looks cleaner than the trade really was.

Not automatically. Splitting reduces price impact from any single piece, but it extends your exposure to the market moving against you during the execution window, and it adds gas cost for each additional transaction. It tends to help most on trades large enough to meaningfully impact a pool's depth, and it tends to add unnecessary cost and complexity on routine, smaller trades where a single execution wouldn't have moved the price much anyway.

It depends on what you're trying to measure. A pre-trade quote isolates execution quality from the moment you were ready to trade. Arrival price, the market price at the moment you first decided to trade, captures the full cost of any delay between decision and execution as well. Use arrival price when you want to separate hesitation cost from execution cost as two distinct problems rather than one blended number.

If you want to improve execution by studying what profitable wallets do on-chain, Wallet Finder.ai gives you a practical way to inspect real entries, exits, trade timing, and wallet behavior across major ecosystems. It's one of the fastest ways to move from a theoretical understanding of price realization to a sharper trading process.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.