Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

June 12, 2026

You enter a trade because the wallet flow looks clean, liquidity seems fine, and the setup has worked before. Then execution hits. Gas spikes, slippage widens, the fill gets worse than expected, and a trade that looked profitable in your notebook turns mediocre or negative on-chain.

That gap between a backtest and a live result is where most traders lose control.

Professionals don't handle that gap with intuition alone. They use sensitivity analysis to pressure-test a strategy before capital is exposed. Instead of asking whether a trade works under one neat assumption set, they ask how the result changes when the messy variables move together. In DeFi, that usually means token price, liquidity depth, slippage tolerance, network fees, and timing.

You track a smart wallet into a new token. The entry looks clean, the wallet has a strong hit rate, and the upside on paper looks worth the risk. Then the trade goes live. Your fill slips, gas jumps, liquidity thins out, and the edge you thought you had gets eaten by execution.

That is the point of sensitivity analysis.

Crypto traders already run rough what-if checks in their heads. What if the entry is worse. What if fees come in high. What if the market moves before the transaction confirms. Useful instinct, but still incomplete. Significant losses rarely come from one variable moving in isolation. They come from several inputs shifting at the same time, usually in the wrong direction.

In DeFi, that matters more than many traders admit. A wallet signal can be valid and still produce a bad trade for anyone following late, sizing too aggressively, or entering a pool with weak depth. Direction is only part of the outcome. Execution quality, fee pressure, and liquidity conditions decide whether a good idea pays.

Sensitivity analysis gives traders a way to test that before capital is on the line. It measures how much the result changes when you adjust the assumptions behind the trade. For a crypto strategy, those assumptions usually include entry price, slippage, gas cost, position size, hold time, and available liquidity. The result might be net PnL, drawdown, expected loss, or the range of outcomes across different market conditions.

Practical rule: If a strategy only works under one narrow set of assumptions, it is fragile.

This matters even more in crypto because inputs are tightly linked. A fast move can worsen your fill, increase the chance of MEV interference, and change your exit options within the same minute. Traders who ignore those dependencies end up treating noise as edge.

The goal is simple. Replace hopeful assumptions with tested ones, then decide whether the setup still deserves capital. For DeFi traders using wallet-level data from tools like Wallet Finder.ai, that turns sensitivity analysis from a textbook concept into a practical filter for copy trades, rotation plays, and on-chain execution risk.

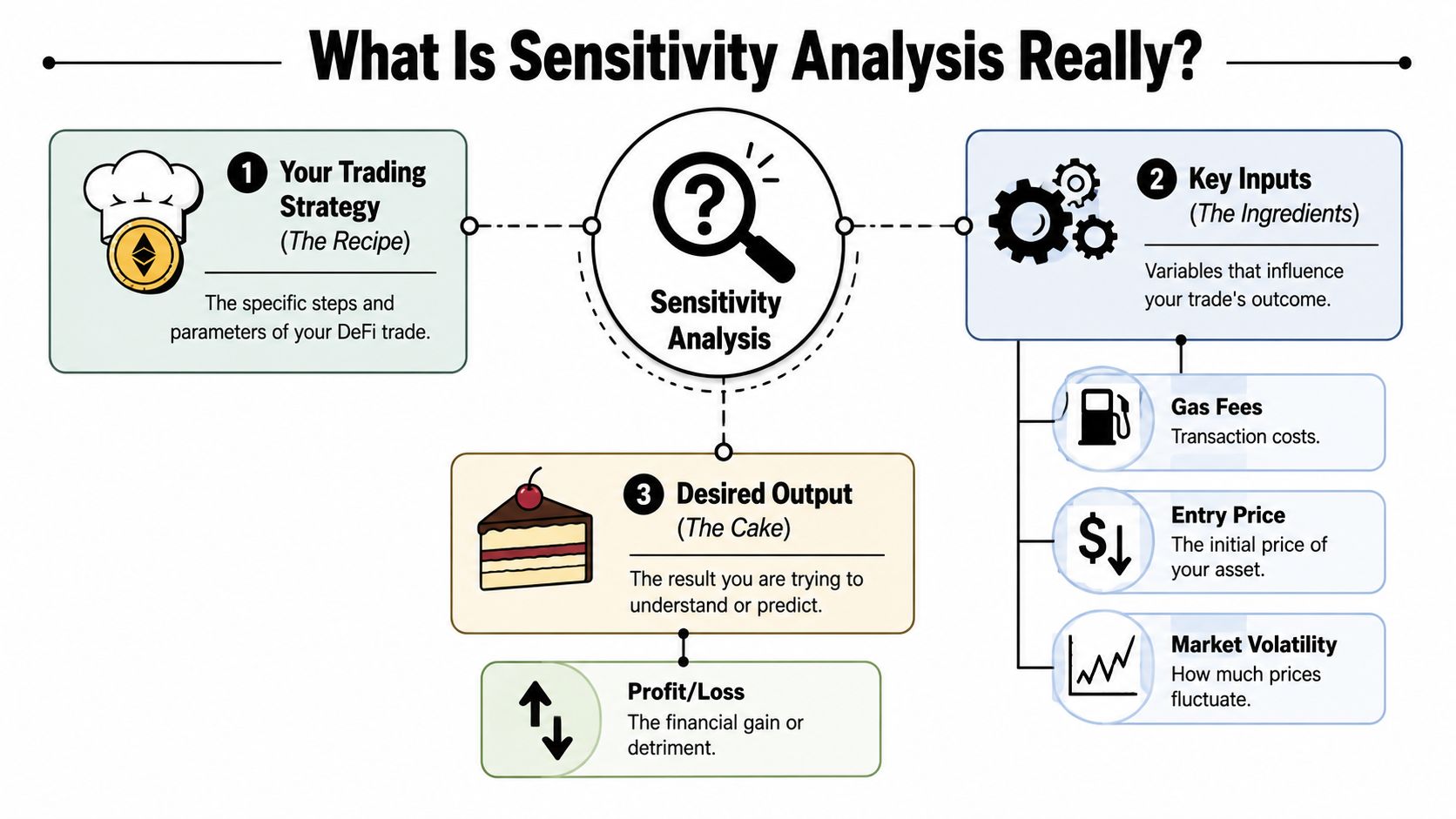

Think of a strategy like a recipe. You have ingredients, a process, and a final result.

The ingredients are your inputs. In crypto, those might be entry price, exit price, gas fees, slippage tolerance, liquidity conditions, and position size. The process is your model. That could be a manual copy-trading rule, a spreadsheet PnL calculator, or a more serious execution model. The result is the output. Usually that's profit, loss, drawdown, or some risk-adjusted measure.

Sensitivity analysis becomes easy to understand once you separate those parts.

If you change one ingredient and the result barely moves, that input isn't very sensitive. If a small change in one variable wrecks the trade, you've found a key risk driver.

Sensitivity analysis isn't just a fancy way to make a spreadsheet look quantitative. It's a way to find out where a strategy is brittle.

Suppose you copy a wallet that buys quickly after a breakout. You may think the core risk is price direction. But after testing, you might learn the strategy is far more sensitive to execution timing than to the token's final move. That changes what you monitor, how you size, and whether the setup is worth taking at all.

It also forces cleaner thinking. Traders often mix conviction and model quality. A strong thesis doesn't fix a weak execution framework. Sensitivity analysis separates the two.

A strategy can be directionally right and still fail because the execution assumptions were wrong.

It isn't a prediction engine. It won't tell you what the market will do next. It tells you how exposed your result is to uncertainty inside your model.

That's a different question, and often the more useful one.

If you're serious about trading on-chain, that's the shift. Stop treating assumptions like background noise. Put them under stress and see which ones control your outcome.

Methods differ in what they reveal. A one-variable test is useful for a fast screen. A broader method is better when slippage, gas, liquidity, and volatility start interacting the way they do in live DeFi trading.

That distinction matters on-chain because inputs rarely move in isolation. Gas spikes during volatility. Liquidity thins out when you want size. Copy-trading a wallet can look profitable in a clean backtest and fail once execution frictions stack up.

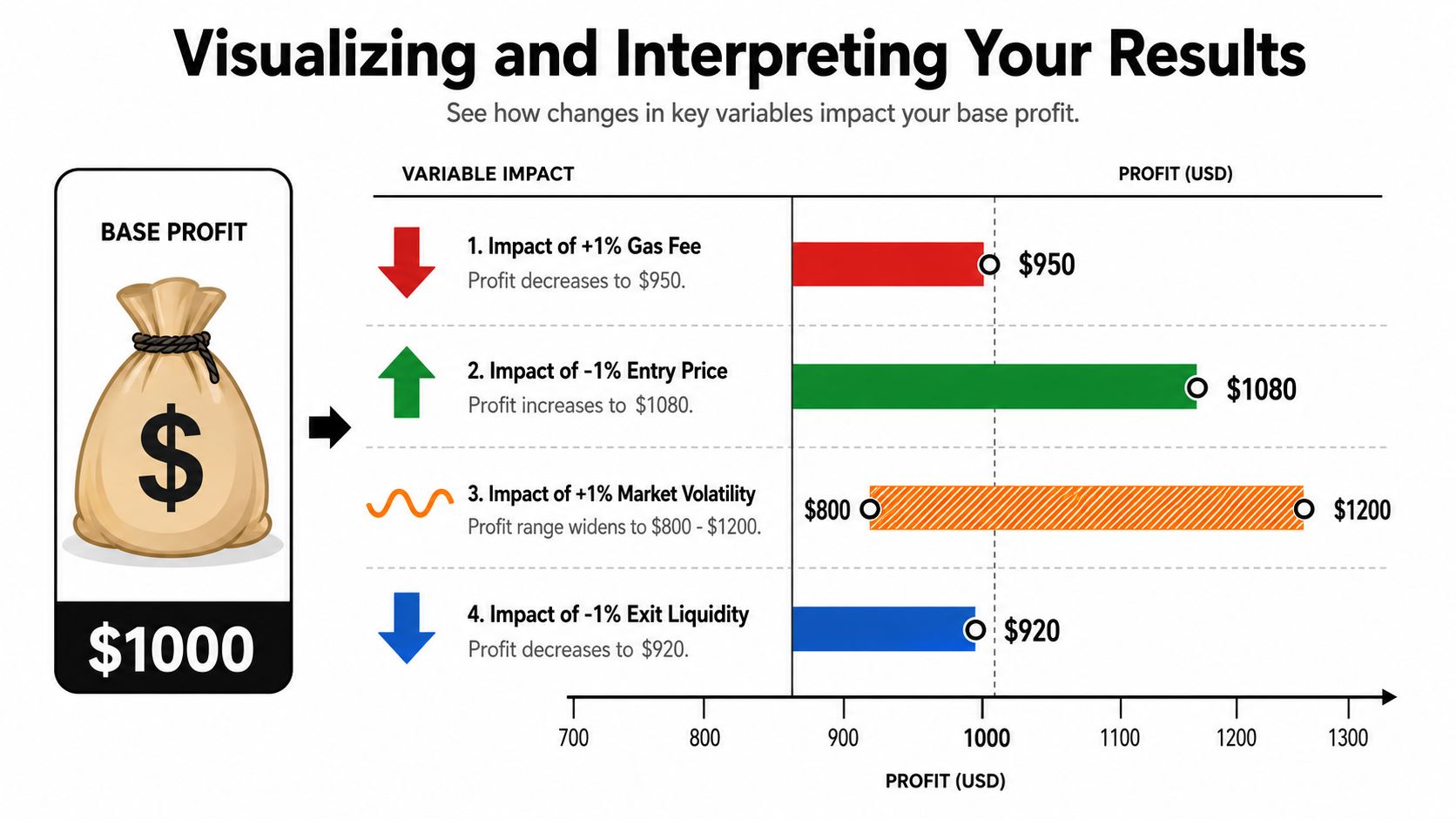

One-way analysis changes a single input while the rest stay fixed.

Use it to identify obvious weak points fast. If raising slippage from 0.5% to 1.5% destroys expected PnL, that is an immediate warning that your edge may depend more on execution quality than on direction. I use this method early because it is quick, easy to audit, and hard to misread.

Its limitation is just as clear. Fixed inputs can hide the underlying source of risk.

Two-way analysis changes two inputs together. Multi-way analysis extends that idea across several variables.

Models begin to resemble real markets more closely, without yet becoming a full simulation. A DeFi trader might test entry price against gas fee, or liquidity depth against position size. Those pairings often expose zones where a setup works, degrades, or breaks completely.

Multi-way analysis is slower, but it surfaces interaction effects that one-way tests miss. If your strategy only survives when gas is low, liquidity is deep, and fills are fast, that is not a stable edge. That is a narrow operating window.

Scenario analysis groups inputs into market states that make sense together.

For crypto, that might mean a launch-day frenzy, a slow grind higher, or a forced-risk-off session after a major exploit. Each scenario should reflect how the market behaves. Higher volatility often comes with worse fills, wider spreads, and less reliable exits.

This method is useful for decision-making because traders place capital into conditions, not isolated variables. It helps answer practical questions. Should this setup be traded only during high-liquidity US hours? Does a wallet-following strategy still hold up when mempool competition increases?

Probabilistic analysis assigns ranges or distributions to inputs and runs many simulations across them.

For active traders, this is often the first method that feels like a real risk tool instead of a spreadsheet exercise. You stop asking for a single expected outcome and start looking at a distribution of outcomes. That shift matters because the median result, the downside tail, and the chance of a severe drawdown can point to very different sizing decisions.

It is also more demanding. You need reasonable input ranges, enough runs to stabilize the output, and enough judgment to avoid feeding the model fantasy assumptions. But if you are testing a strategy with multiple moving parts, this is usually the method that shows whether the edge is durable or just backtest luck.

| Method | How It Works | Best For | Example |

|---|---|---|---|

| One-way analysis | Changes one input while holding the rest fixed | Fast checks and initial screening | Vary slippage tolerance to see how net PnL responds |

| Two-way analysis | Changes two inputs together | Finding pairwise interaction patterns | Test entry price and gas fee at the same time |

| Multi-way analysis | Changes several inputs across a defined grid or rule set | Stressing a strategy under more realistic combinations | Evaluate token price, liquidity, and fees together |

| Scenario analysis | Bundles multiple input changes into market states | Decision-making under named conditions | Compare “flash crash” versus “trend continuation” |

| Probabilistic sensitivity analysis | Samples across input ranges to generate outcome distributions | Estimating loss risk and tail exposure | Simulate many possible PnL paths for a copy-trading setup |

A practical workflow is straightforward. Start with one-way tests to find obvious pressure points. Use two-way or multi-way analysis to map interactions. Add scenario analysis to reflect real market regimes. Before putting on size, run a probabilistic layer to see the full spread of outcomes.

If you want to identify which variables tend to move together before building these tests, pair this work with correlation analysis for on-chain research.

Raw output doesn't help much if you can't read it quickly. A strong sensitivity analysis should tell you, at a glance, what matters, where the danger zones are, and how ugly the tail can get.

A tornado chart ranks variables by impact. The longest bars show which assumptions move your output the most.

For traders, that means you can stop obsessing over low-impact details. If gas fees barely move the result but exit liquidity drives most of the PnL spread, your monitoring should reflect that. Tornado charts are especially useful early in model review because they cut through noise fast.

Heatmaps work well when two variables interact. Put one variable on each axis and color the output. You'll see where the strategy works, where it degrades, and where it fails.

This is useful for execution problems. A heatmap of entry price against gas fee can show that a setup is profitable only in a narrow band. A strategy that looked stable in a summary table may turn out to have a very small safe zone.

Distribution charts matter most once you move into probabilistic sensitivity analysis. Instead of a single expected result, you get a range of possible outcomes.

Research on probabilistic sensitivity analysis notes that when inputs such as gas fees and token price are varied across historical percentile ranges, PnL can become heavy-tailed rather than normal, which implies a higher chance of extreme losses than simple deterministic what-if tests suggest, as discussed in this Cambridge treatment of sensitivity analysis.

Don't trust a strategy because the average outcome looks good. Trust it only after you've inspected the left tail.

Use the charts to answer a few direct questions:

If you're building dashboards for this work, good chart design matters. This walkthrough on blockchain data visualization techniques is useful for turning model output into something you can trade from.

A wallet you want to mirror buys a low-float token at 9:02, exits two hours later, and books a clean gain. You copy the setup at 9:07, route through thinner liquidity, pay more gas, and give back most of the edge in slippage. The trade idea was fine. The execution assumptions were wrong.

This is one of the clearest uses for sensitivity analysis in crypto. A copied trade rarely fails because the original wallet had no edge. It fails because your version of the trade has different latency, fees, pool depth, and fill quality.

Start with the variables that change between the source wallet and your account. Delay after the original fill. Slippage tolerance. Gas cost. Position size relative to pool depth. Then test how much each one changes realized PnL. If a strategy only works inside a narrow execution window, treat it as fragile.

For traders sourcing ideas from smart money wallets, the first job is understanding how those wallets trade on-chain before trying to reproduce the result. This guide on checking on-chain wallet behavior is a good starting point.

AMMs create interaction risk that traders often miss in spreadsheet-level analysis. Token volatility, liquidity depth, and network congestion can hit at the same time. That matters because the loss from all three moving together is often worse than the sum of each one in isolation.

A simple one-variable test can still help. Change token price assumptions while holding everything else fixed. Then change slippage. Then gas. That gives a first pass on what matters most. But if you're trading size in volatile pools, you need to test combinations, not just isolated inputs.

I have seen traders model a pool as if liquidity conditions and execution costs were separate line items. In calm conditions, that shortcut looks acceptable. In stressed conditions, it breaks fast. A pool that looked tradable at a 20 basis point slippage assumption may become untradeable once gas spikes and your order moves deeper into the curve.

The practical takeaway is simple. Size AMM trades for the hostile state, not the average state.

Yield farming, basis trades, and looping strategies often look stable until the inputs start moving together. Funding changes, collateral prices drop, borrow costs rise, and exit liquidity gets worse right when you need it.

Sensitivity analysis is useful here because it forces a trader to stop evaluating yield as a single headline number. Instead, test the strategy under a range of token prices, utilization levels, rewards emissions, and transaction costs. Then look at what happens to net yield, liquidation distance, and time needed to unwind.

That process usually changes the decision. A farm showing attractive nominal APY can have weak real economics after fees and adverse price moves. A looping strategy can survive small collateral drawdowns but fail once borrow rates reprice at the same time. Those are the cases where sensitivity analysis saves money because it shows where the trade stops being an income strategy and starts behaving like short volatility.

Strong on-chain performance is only a lead. Sensitivity analysis tells you whether the edge survives your actual execution conditions.

A good workflow doesn't need to start with a massive quant stack. A spreadsheet is enough if the logic is clean.

The goal is simple. Take a past trade, define the key assumptions, and test how the result changes when one or more inputs move. If you do this consistently, you'll learn very quickly whether a strategy is stable or just flattering itself with one lucky path.

Start with a wallet whose trade history is clear enough to reconstruct. Don't grab the flashiest profile. Pick one with understandable entries, exits, and position sizing.

You want a trade where you can identify:

If you're still building your shortlist, this guide on how to check on-chain wallet behavior is a useful starting point.

Use Google Sheets or Excel. Keep the first version deliberately plain.

A workable model usually needs these fields:

| Input | What to enter | Why it matters |

|---|---|---|

| Entry price | Observed or assumed fill | Drives initial position economics |

| Exit price | Actual or tested exit | Controls realized gross return |

| Position size | Capital allocated | Sets exposure |

| Trading fees | Network and execution costs | Reduces net result |

| Slippage | Estimated execution friction | Captures market impact |

| Net PnL | Formula output | Main result to test |

At this stage, don't over-engineer. If the model already has too many moving parts, you'll struggle to interpret the output.

Pick one variable that matters. Exit price is a common starting point because it gives immediate intuition.

Create a table of alternative values around the observed trade. Then recalculate net PnL for each value. You don't need fancy software. Spreadsheet data tables work fine.

This first pass helps answer basic questions:

Once the one-way analysis is done, add a second variable. Good pairs include gas fee and slippage, or entry timing and exit price.

Many strategies reveal their weakness in such situations. A setup that looks acceptable under isolated changes may become unattractive once two execution frictions move together.

Keep the model as simple as possible, but no simpler than the market structure you're trading.

A sensitivity table is only useful if it changes behavior. Convert what you learn into specific rules.

For example:

That's the key outcome. You're no longer reacting to surprises. You're trading with pre-defined failure conditions.

A sensitivity model fails fastest at the edges. Traders often test a neat base case, shift one input a little, and call the strategy "safe." That works for simple spot trades. It breaks down fast in DeFi, where gas spikes during volatility, slippage widens as liquidity thins, and execution timing changes the fill you get.

The first rule is range discipline. If your test inputs do not match live market conditions, the output is false comfort. For crypto, that usually means using stressed values, not average ones. Test the fee regime you get during crowded blocks. Test the slippage you see when copying size into thin pools. Test exit conditions during fast reversals, not only in orderly periods.

One-at-a-time analysis still has value. It is useful for triage and for spotting which variable deserves attention first. The problem starts when traders stop there. In DeFi, variables often move together, so isolated tests hide the actual failure mode.

Use a few habits to keep the work honest:

There is also a practical trade-off here. More complexity can improve realism, but too many inputs turn the model into a black box you do not trust under pressure. I prefer a smaller model tied to variables I can observe and act on. If a result cannot change sizing, execution, or trade selection, it does not belong in the decision process.

Sensitivity analysis does not forecast the next candle. It shows how fragile your trade is before capital is on the line. That makes it part of regular risk work, especially if you are using Wallet Finder.ai data to study profitable wallets and pressure-test whether their trades still make sense under your execution conditions.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.