Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

June 7, 2026

You're probably looking at a token launch calendar, a launchpad announcement, or a Discord thread and asking the fundamental question behind all the hype: is this an edge, or just another crowded sale where early buyers dump on each other?

That's the right question.

Most explainers answer “what is an initial DEX offering” at the glossary level and stop there. Traders need more than that. You need to know how the launch works, where the risk sits, what usually breaks after listing, and how to tell the difference between a clean setup and a bad one. In practice, an IDO is only interesting if the structure gives you a workable entry, enough liquidity to trade, and tokenomics that don't punish you the moment the pool opens.

An Initial DEX Offering, or IDO, is a token launch where a blockchain project makes its first public debut on a decentralized exchange, using liquidity pools and smart contracts so buyers can trade as soon as the sale goes live. That's why IDOs are often framed as a more community-driven alternative to older fundraising models like ICOs and IEOs, as described in CoinMarketCap's Initial DEX Offering glossary.

If you're searching for early-stage crypto opportunities, this is one of the main routes you'll run into. A project doesn't wait for a centralized exchange listing. It launches directly into on-chain trading.

That changes the experience for both sides. The project gets a public sale and immediate market access. Buyers don't have to wait for some later listing event to see a tradable market. If you need a quick refresher on the venue itself, this breakdown of what a DEX does is useful context.

An IDO matters because it compresses fundraising and market launch into the same event. You're not only buying a token. You're stepping into the first live market for that token.

That creates opportunity, but it also creates stress:

Practical rule: Don't evaluate an IDO like a private investment memo. Evaluate it like a fresh market with fragile liquidity and emotional order flow.

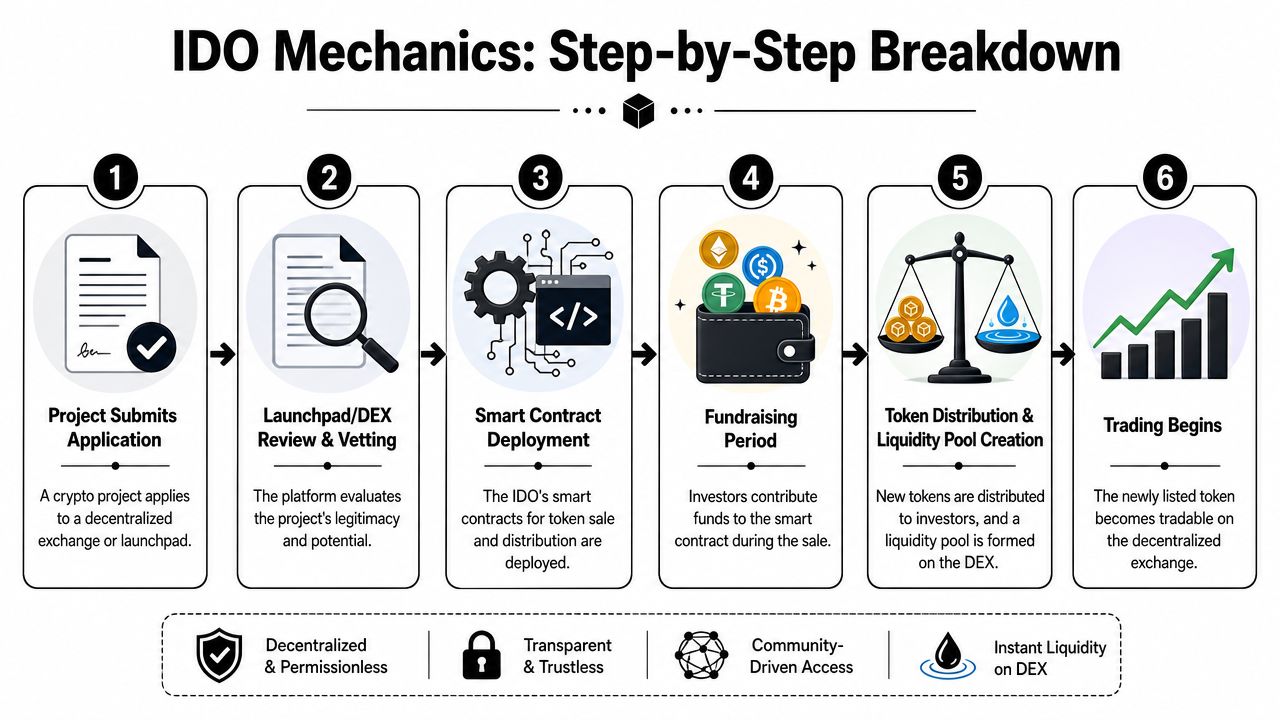

The term sounds technical, but the core idea is simple. A project launches on a DEX, users commit funds, smart contracts handle distribution, and trading opens once liquidity is added.

The important part isn't just the definition. It's the implication. An IDO is not “early access” in the abstract. It's a public token sale with a live market attached to it. That's why some IDOs become strong opportunities and others become traps within hours.

An IDO is easiest to understand if you think of it as a self-running sale and listing process. The project sets the rules in code. Users bring funds. The contract handles distribution. The liquidity pool becomes the first market.

Ledger describes an IDO as a fundraising method where a crypto project sells newly issued tokens directly on a DEX, typically via smart contracts and liquidity pools rather than a centralized intermediary, with the sale and first listing happening on-chain and enabling immediate trading liquidity once the pool is live in its IDO glossary entry.

Here's the practical sequence most traders deal with:

A project chooses a launch venue

Sometimes that's a launchpad with an approval process. Sometimes it's a direct DEX listing path.

Sale contracts get deployed

These contracts define who can participate, how funds are accepted, and how tokens are distributed.

Participants commit funds

Buyers connect a wallet and send the accepted asset during the sale window.

Tokens are allocated

The contract either distributes tokens automatically or makes them claimable.

Liquidity gets added

The team pairs the new token with a base asset in a pool so trading can begin.

The market opens

At that point, the token has a live venue for buying and selling.

The opening market doesn't appear out of nowhere. It needs a pair. In practice, that means the project's token is matched with a base asset that traders already use. That pairing creates the first executable market.

It operates as an automated booth instead of an order-book listing. The contract doesn't need a centralized operator to match people manually. It handles the swap logic itself.

What works cleanly on paper can still go badly in live trading. The sale might be orderly, but the first hour can still be chaotic if demand is one-sided or the pool is shallow.

That's why experienced traders don't stop at “how do I join?” They ask:

The smartest way to read an IDO isn't as a launch event. Read it as the creation of a brand-new market with almost no trading history.

IDOs didn't appear in a vacuum. They grew out of dissatisfaction with earlier fundraising models. CoinGecko notes in its guide to IDOs that IDOs emerged as the market shifted away from ICOs and IEOs.

That history matters because each format changes who controls access, who handles distribution, and how quickly a token reaches a tradable market.

| Characteristic | Initial Coin Offering (ICO) | Initial Exchange Offering (IEO) | Initial DEX Offering (IDO) |

|---|---|---|---|

| Where the sale happens | Usually through the project itself | Through a centralized exchange | On a decentralized exchange or DEX-linked launchpad |

| Intermediary | Minimal or none beyond the project team | Centralized exchange acts as gatekeeper | Smart contracts and on-chain infrastructure handle the process |

| Access style | Depends on project rules | Depends on exchange account access and platform rules | Usually wallet-based participation |

| Token listing path | May come later and separately | Often tied to the exchange hosting the sale | Launch and first public market happen in the same on-chain flow |

| Custody model | Users often rely on project process | Users rely on exchange process | Users interact through their own wallets |

| Core trade-off | Open but often trust-heavy | More structured but more centralized | Faster, on-chain, but highly sensitive to launch quality |

An ICO puts more burden on trust. You're relying heavily on the project team's sale process and later execution.

An IEO adds an exchange in the middle. That can make participation feel more structured, but it also means access is shaped by a centralized platform.

An IDO moves the action on-chain. That's attractive because it removes part of the centralized bottleneck. It also means the live market forms faster, which is good when the setup is strong and painful when it isn't.

Projects usually choose the IDO route when they want decentralized distribution and immediate market access. That can help them build early community ownership around the launch.

For traders, the signal is mixed. An IDO can indicate a project wants open participation. It can also mean you'll be trading in a much rougher opening market than you would on a mature centralized venue.

The lesson is simple. Don't treat “IDO” as a quality stamp. Treat it as a market structure choice.

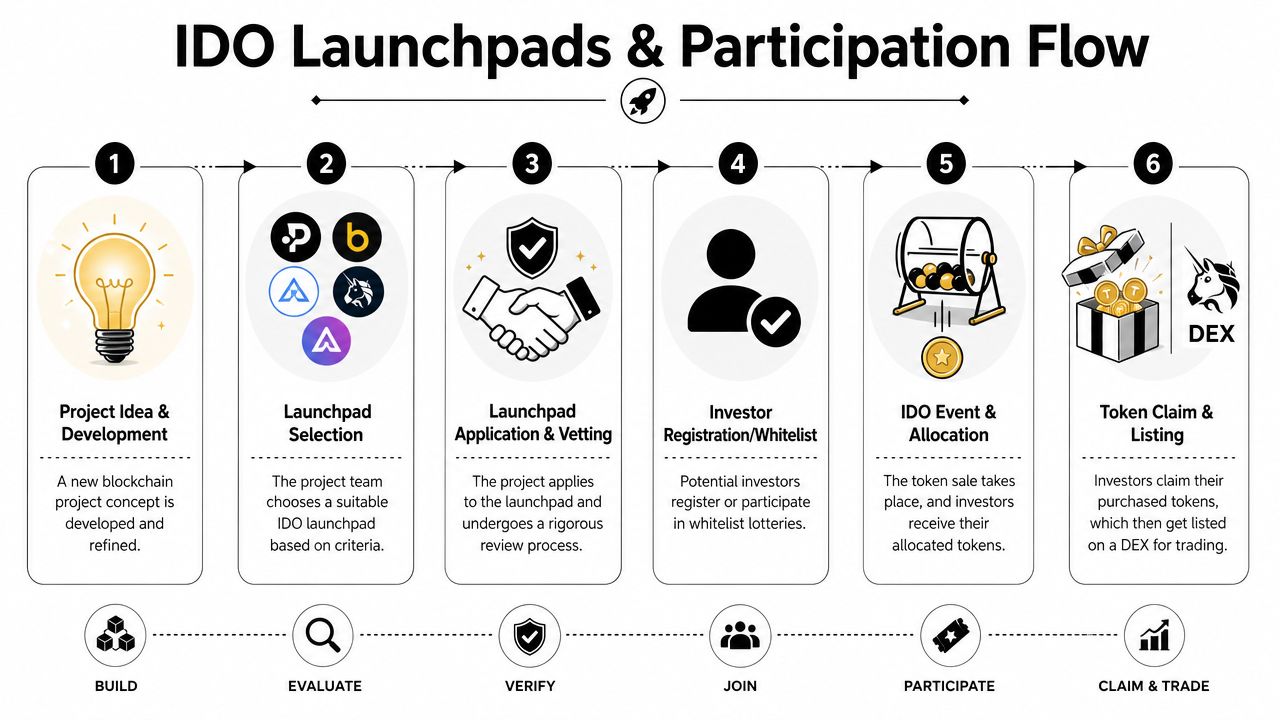

A lot of traders think every IDO happens directly on a big DEX. However, that's not the common way they are encountered. Many sales are organized through launchpads, which add structure around the event.

These platforms often screen projects, manage eligibility, and coordinate allocation rules. That doesn't remove risk, but it does change how you get access.

You'll usually see one of these structures:

If you're comparing sale formats more broadly, this overview of token pre-sales helps place IDOs in the larger early-access space.

A launchpad can help with:

But a launchpad doesn't guarantee a good trade.

That distinction matters. A clean interface and a familiar platform don't solve weak tokenomics, thin post-listing liquidity, or immediate sell pressure.

A polished launchpad can improve access. It can't rescue a launch with bad incentives.

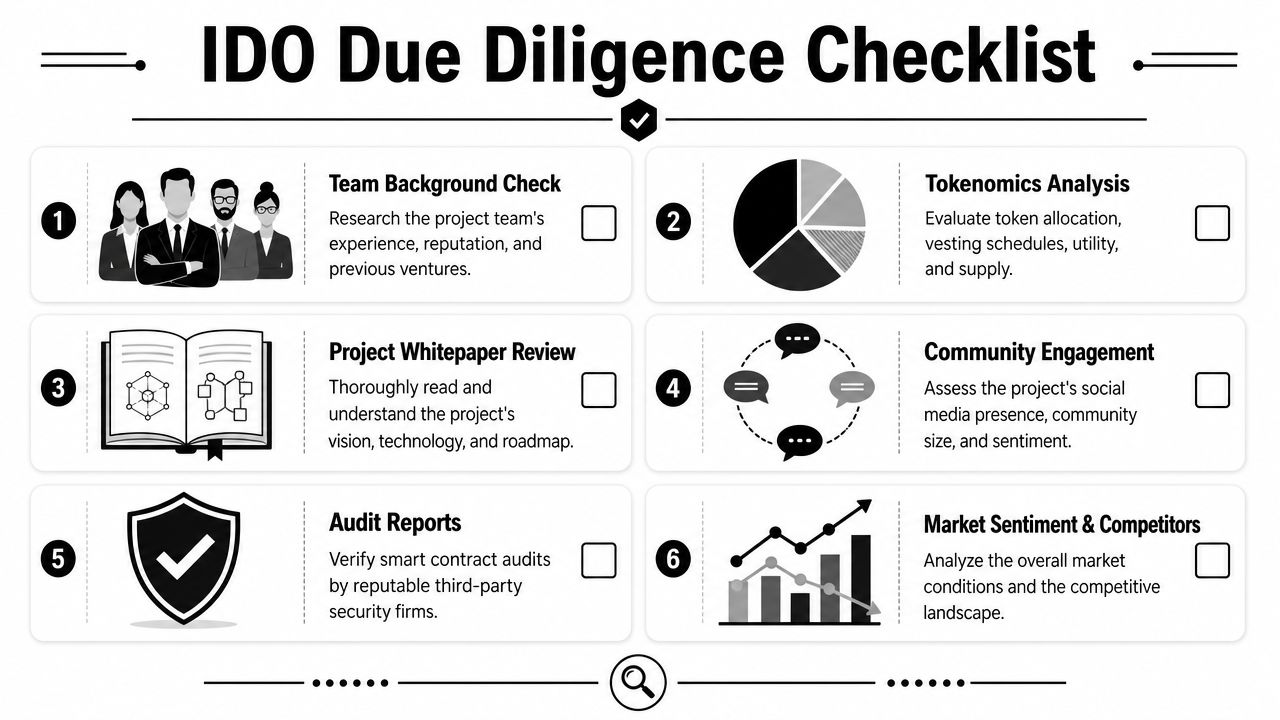

Before you try to join an IDO, confirm the basics:

Most missed opportunities in IDOs aren't caused by bad analysis. They're caused by operational mistakes. Wrong chain. Wrong wallet. Wrong time. Wrong contract.

The biggest mistake in IDO trading is assuming the hard part is getting access. It isn't. The hard part is deciding whether the launch is tradeable at all.

CoinTracker's explanation of IDO market structure gets to the core issue. An IDO usually requires the token to be paired with a base asset such as ETH or USDT in a liquidity pool, and that pool becomes the executable market for price discovery. That reduces settlement friction, but launch quality depends heavily on the initial liquidity depth and the tokenomics written into the contract.

That one point explains a lot of real-world blowups.

A token can “launch successfully” and still be miserable to trade. If the initial pool is too shallow, price moves violently on small flows. That creates slippage on both entry and exit.

If early participants, insiders, or the team can sell too freely into the first market, the pool becomes an exit ramp for people with better entry prices than you.

Everything runs through code. If the sale contract, claim logic, or token contract is flawed, your analysis of the project story won't matter.

Use this before you commit capital:

Traders lose money in IDOs when they rely on surface signals:

| Weak signal | Why it fails |

|---|---|

| Large social buzz | Attention doesn't guarantee stable post-launch order flow |

| Fast whitelist fill | Scarcity in registration isn't the same as durable market demand |

| Familiar launchpad | Platform quality and token quality are different questions |

| A strong opening candle | Early momentum often attracts late buyers into poor liquidity |

Field note: The first green candles don't prove strength. Sometimes they just prove there weren't enough sellers yet.

You get the whitelist. The token launches. The first candle rips, CT calls it a winner, and then early buyers start feeding inventory into thin liquidity. That is the part that decides whether the IDO was a good trade or a trap.

A lot of IDO content stops at access. Real PnL usually comes from what happens after listing. Entry quality, wallet behavior, sell pressure, and liquidity depth matter more than the sale announcement once the market opens.

Independent commentary in this guide to IDO trading dynamics makes the same point. Post-launch structure often matters more than the sale itself, especially when liquidity is thin and early holders can exit fast.

Announcements tell you where attention is. On-chain activity tells you who is committing capital.

Using smart-money tracking on Wallet Finder.ai, you can examine whether wallets with a history of good early entries are participating, how they size in, and whether they hold through the first wave of volatility or sell into it. That gives you a much better read on trade quality than social buzz alone.

I care less about whether a launch is popular and more about whether capable wallets treat it like a real opportunity.

Build a list of credible wallets

Start with wallets that have shown repeatable performance across multiple early token trades. One big winner is noise. Consistency is the signal.

Check their entry timing

Some wallets buy before listing activity gets crowded. Others wait for the first liquidity to settle. Timing tells you a lot about their playbook and the risk they are willing to take.

Study how they manage exits

Good wallets do not all behave the same way. Some sell strength fast. Others scale out over time or add on weakness if the market structure stays healthy.

Look for clustering

A single smart wallet can be early or wrong. Several strong wallets entering around the same launchpad, token, or pool deserve attention.

Set alerts and watch changes live

Speed matters, but context matters more. An alert is useful only if you already know why the wallet is worth tracking.

A lot of traders would benefit from watching this before they try to build the habit manually:

This approach helps you answer tradeable questions:

Those answers will not replace project research. They do improve your timing and position sizing.

The first few hours matter most. That is where weak launches usually reveal themselves.

The best IDO setups tend to look coherent on-chain. Strong wallets appear, entries are not isolated, and post-listing behavior stays disciplined. Weak ones usually show the opposite. Plenty of excitement at launch, then a rush to offload into the first burst of demand.

Sometimes, yes. Sometimes they're terrible trades.

There's no reliable “typical return” you can quote across IDOs, and you shouldn't trust anyone who pretends there is. Profitability depends on allocation terms, opening liquidity, tokenomics, broader market conditions, and whether buyers after launch can absorb early selling.

In many jurisdictions, they can be. The exact treatment depends on where you live and how local tax rules classify token purchases, sales, swaps, and later disposals.

If you trade IDOs regularly, keep records from the start. Waiting until the end of the tax year usually turns a manageable task into a mess.

Different ecosystems host IDOs depending on where builders and users are active. In practice, traders often encounter IDOs on chains with established DEX infrastructure and active launchpad ecosystems.

The right question isn't “which chain is best?” It's “which chain supports the wallet tools, liquidity culture, and project quality I can evaluate well?”

It depends on the setup.

Buying during the sale can give you better initial pricing, but it also puts you directly in front of early volatility and seller pressure. Waiting can reduce uncertainty, especially if you want to see how liquidity, wallet behavior, and first-day price action develop.

For most traders, patience beats blind speed.

If you want a more practical edge on IDOs than launch calendars and social hype can give you, Wallet Finder.ai is worth using. It helps you track profitable on-chain wallets, study how strong traders enter and exit new token opportunities, and set alerts so you can react to real wallet behavior instead of guessing.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.