Recovery Factor Calculation for Smart Traders

Master the recovery factor calculation to measure a strategy's resilience. Learn the formula, see DeFi examples, and find top wallets with Wallet Finder.ai.

June 20, 2026

Wallet Finder

June 18, 2026

A wallet can post eye-catching gains and still be a terrible strategy to copy.

That usually shows up after the first ugly pullback. You mirror a trader who looked unstoppable on a leaderboard. A few fast rotations later, your account is underwater, and the problem isn't just the loss. It's that you now have no idea whether this is normal heat, a temporary liquidity vacuum, or a strategy that was always one bad sequence away from breaking.

PnL tells you where a wallet ended up. Drawdown analysis tells you what it took to get there. In crypto, especially in DeFi, that difference matters more than most traders admit.

Consider a simple analogy: two climbers can reach the same summit, but one took a stable route while the other nearly fell off the mountain three times. If you only look at the final altitude, you miss the risk that defined the journey.

Trading works the same way. A wallet can finish with strong realized gains while spending long stretches in painful declines. That matters if you're allocating capital, copying trades, or deciding whether a strategy can survive the next regime change.

A raw return number doesn't show whether the trader:

That's why experienced traders look past the top-line result. The return is the headline. The drawdown profile is the character reference.

Practical rule: If you wouldn't sit through the worst historical decline of a strategy, you shouldn't size it based on its best historical return.

This is also where a lot of copy trading mistakes start. Traders select wallets based on recent winners, not on how those wallets behaved during stress. A strategy that compounds steadily with contained pullbacks is usually easier to hold, easier to size, and easier to stick with than one that alternates between euphoric spikes and brutal air pockets.

For a broader framework on building those guardrails, Wallet Finder's guide to risk management for traders is a useful companion.

In traditional markets, you might get time to reassess a bad trade. In DeFi, a thin pool, a cascade of exits, or a failed momentum follow-through can compress that whole process into minutes. That's why drawdown analysis isn't an academic metric. It's a survival tool.

A wallet with modestly lower returns and cleaner drawdowns is often the better long-run choice. You can allocate to it with clearer expectations, survive the rough patches, and avoid the classic mistake of quitting right before the recovery.

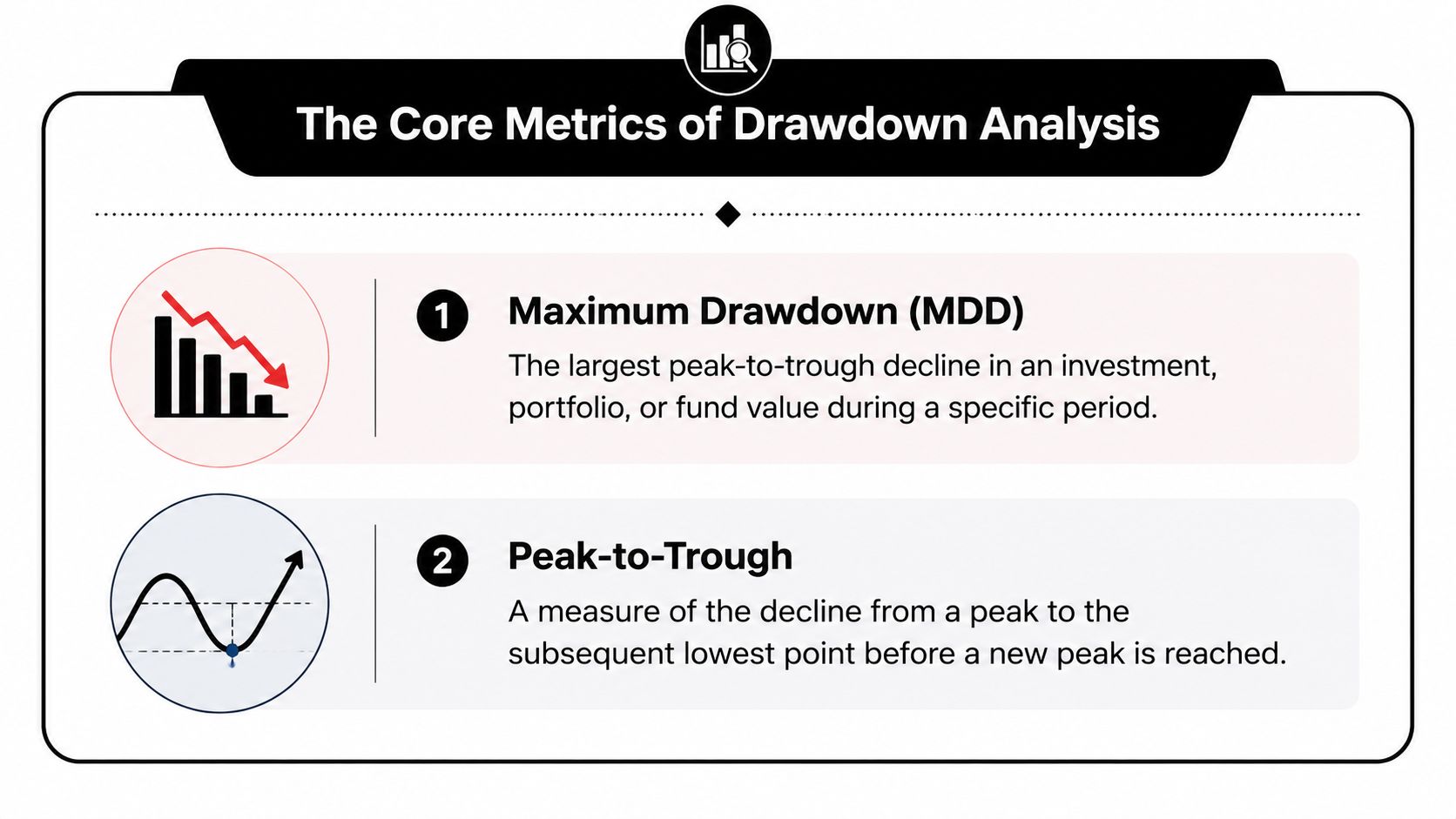

At its base, drawdown analysis measures the decline from a historical peak to a subsequent trough. Maximum drawdown, or MDD, is the summary statistic most traders use to compare downside risk across strategies, and the concept also includes recovery time, which makes it a two-dimensional risk metric, as outlined by CFI's explanation of drawdown.

You don't need a giant risk model to get value from drawdown analysis. You need a few metrics, used consistently.

| Metric | What It Measures | Trader's Takeaway |

|---|---|---|

| Peak-to-trough decline | The drop from the most recent high to the lowest point before a new high | Shows how much pain a strategy took in a specific downturn |

| Maximum drawdown | The worst peak-to-trough decline over the full sample | Quick way to compare downside severity across wallets or systems |

| Time to recovery | How long capital stayed below the prior high-water mark | Tells you how long money was trapped underwater |

| Drawdown distribution | The pattern of repeated losses across the equity curve | Helps separate occasional stress from a strategy that regularly breaks down |

Peak-to-trough decline is the local event. It answers, “How bad did this specific slide get before the strategy stabilized or recovered?”

Maximum drawdown is the big one. It captures the single worst realized loss along the path. Traders use it because it's easy to compare. If two wallets have similar returns, the one with the shallower MDD is often easier to finance and easier to hold.

Time to recovery is where a lot of traders get fooled. A decline isn't just about how deep it got. It's also about how long your capital stayed stuck below its previous peak. Two strategies can show the same loss on paper but create very different trading experiences if one recovers quickly and the other grinds sideways for months.

Drawdown has a money dimension and a time dimension. Ignore either one and you understate the real risk.

Drawdown distribution is less formal but extremely useful. Instead of focusing only on the worst event, you look at the pattern. Does the wallet suffer repeated sharp dips? Are losses clustered around certain token types, market conditions, or execution styles? That pattern tells you whether the risk is occasional or structural.

A lot of people stop at MDD because it's simple. That's a mistake.

Use the metrics together:

That bundle gives you a much better read on whether a wallet is resilient, fragile, or overfit to one market phase.

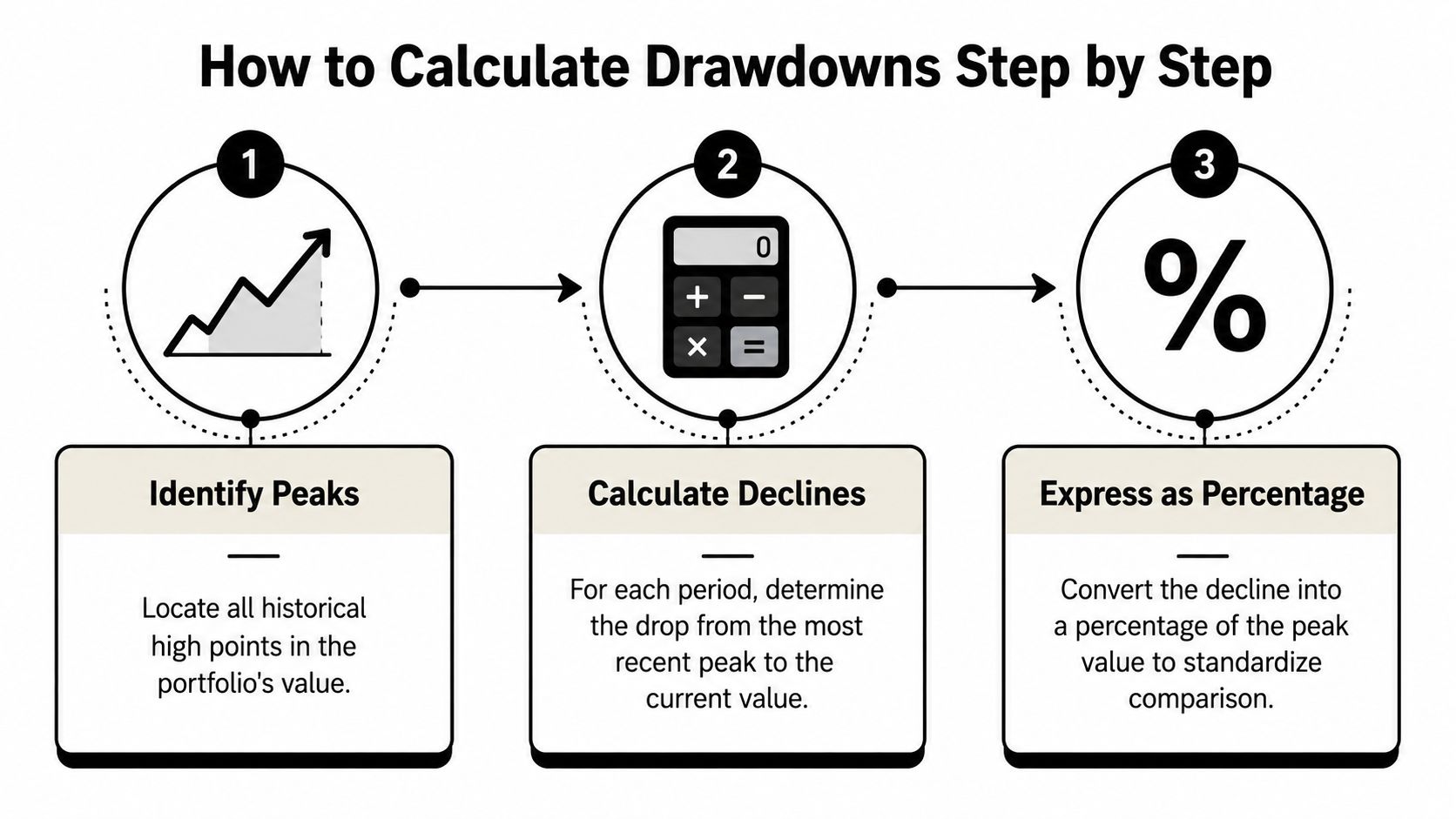

The mechanics are simple. Start with a sequence of portfolio values, track the running peak, measure the decline from that peak at each point, and then identify the worst decline in the series.

Maximum drawdown is computed as (Trough Value - Peak Value) / Peak Value, which makes it a path-dependent metric that captures the worst realized loss along an equity curve rather than a path-independent measure like volatility, as described in this walkthrough of maximum drawdown calculation.

Suppose your equity curve looks like this:

| Period | Portfolio Value | Running Peak | Drawdown |

|---|---|---|---|

| 1 | 100 | 100 | 0% |

| 2 | 120 | 120 | 0% |

| 3 | 110 | 120 | -8.33% |

| 4 | 130 | 130 | 0% |

| 5 | 90 | 130 | -30.77% |

| 6 | 95 | 130 | -26.92% |

| 7 | 140 | 140 | 0% |

The process is straightforward:

In this example, the worst drawdown occurs when the portfolio falls from 130 to 90. That's the maximum drawdown.

Drawdown analysis offers greater utility than a simple return summary.

Take two traders who both finish at the same ending value. One climbs steadily. The other doubles, crashes hard, then claws back. End result looks identical in a leaderboard export. Risk experience is completely different. Drawdown captures that path.

That matters even more when you're reviewing wallet histories for copy trading. The order of gains and losses affects psychology, sizing decisions, redemption risk, and whether a trader would've stayed with the strategy at all.

If you're doing this in Excel or Google Sheets, set up four columns:

Use a running maximum for the peak column, then compute drawdown relative to that peak. Once you have the series, you can chart it below the equity curve. That visual alone often reveals more than a summary dashboard.

For strategy research, this pairs well with a structured testing process. A practical reference is Wallet Finder's article on building a backtesting framework, especially if you want to compare drawdown behavior across multiple rulesets.

If you can't plot the equity curve and the underwater curve together, you probably don't understand the strategy well enough to size it.

For traders working in Python, the logic is clean:

import pandas as pd# Example equity curvedf = pd.DataFrame({"equity": [100, 120, 110, 130, 90, 95, 140]})# Running peakdf["peak"] = df["equity"].cummax()# Drawdowndf["drawdown"] = (df["equity"] - df["peak"]) / df["peak"]# Maximum drawdownmax_drawdown = df["drawdown"].min()# Recovery flagdf["at_new_high"] = df["equity"] >= df["peak"]print(df)print("Maximum Drawdown:", max_drawdown)This gives you the full drawdown series, not just the worst value. That's important because the series lets you inspect recurring stress, not only the single worst event.

Once the base series is working, add a few extra fields:

Those additions turn a static risk metric into a research tool. You stop asking, “How bad was it?” and start asking, “What conditions produced the damage?”

That's the level where drawdown analysis becomes operational.

A drawdown number means nothing in isolation. It only becomes useful when you connect it to strategy type, holding period, liquidity profile, and your own tolerance for pain.

A deep drawdown isn't automatically disqualifying. Some aggressive strategies will always run hotter than conservative ones. A key question is whether the drawdown profile matches the return stream and whether you can hold it through stress without changing behavior at the worst moment.

Historical asymmetry matters, as Morgan Stanley found that only about 1 in 6 stocks that fell 95% to 100% ever returned to their prior peak, while roughly 4 in 5 stocks with drawdowns in the 0% to 50% range recovered, according to Morgan Stanley's analysis of drawdowns and recoveries.

The lesson isn't that every crypto asset behaves like an equity. The lesson is that very deep losses can change the odds of recovery in a fundamental way. Once capital gets crushed hard enough, “it can always come back” stops being a serious risk assumption.

Don't ask whether a drawdown is good or bad in the abstract. Ask tighter questions:

A lot of traders use return-to-drawdown ratios such as Calmar or MAR to contextualize risk. That's sensible. A strategy with strong returns and moderate drawdowns usually deserves more attention than one that produced similar returns with much worse downside.

But ratios can hide ugly internals. A wallet can score well while still relying on infrequent bursts, unstable liquidity, or concentrated bets. Use the ratio as a filter, not a verdict.

Later in your review, it helps to watch a visual explanation before making sizing decisions:

The drawdown you can survive is more important than the return you can advertise.

When a drawdown profile looks rough, the answer isn't always “reject it.” Sometimes the right move is to resize it, isolate it in a satellite sleeve, or require tighter execution conditions before following the wallet.

Good interpretation turns drawdown analysis into a position-sizing input. Bad interpretation turns it into trivia.

Traditional drawdown analysis starts to break when you apply it lazily to DeFi.

The issue isn't the concept. The issue is sampling speed. If you only evaluate daily closes, you'll miss the intraday and often near-instant moves that define on-chain risk. In DeFi, liquidity can vanish, spreads can gap, and a wallet can move from healthy to broken before a daily mark tells you anything useful.

The speed of liquidity shifts in DeFi makes traditional risk models insufficient. Data indicates that 95% of crypto drawdowns occur within minutes, not days, which is why on-chain-specific analysis is needed to separate a temporary dip from a genuine strategy failure, as discussed in Western Asset's drawdown analysis note.

That point has direct consequences for copy traders:

When reviewing an on-chain wallet, don't stop at total PnL. Rebuild the path.

A workable process looks like this:

Platform-level tooling matters. Wallet Finder.ai can surface wallet histories, PnL, timing, and position-sizing data that help traders inspect whether a profitable wallet is also stable enough to follow.

What works

What doesn't

On-chain drawdowns aren't only about price. They're also about exitability.

A wallet that repeatedly takes steep hits but recovers because it's early, fast, or privileged in execution may still be a poor copy candidate for everyone else. Drawdown analysis helps expose that mismatch.

The easiest way to use drawdown analysis is to make it part of your daily filter, not a one-off postmortem after a bad week.

That means every strategy review, wallet screen, and capital allocation decision should include a drawdown lens. Not because it predicts everything. It doesn't. Because it prevents the most common form of self-deception in trading, which is confusing high returns with durable returns.

Use a simple routine:

If you're tracking wallets for mirroring, keep the checklist practical:

Once you build this into your workflow, the whole selection process improves.

You stop chasing wallets that only look good at the endpoint. You start favoring strategies you can hold through volatility. You get fewer surprise failures, fewer emotional exits, and a more honest view of how copied performance might diverge from source performance.

That's the core value of drawdown analysis. It turns raw performance data into risk-aware decision-making.

Wallet Finder.ai helps traders inspect on-chain wallet histories, trade timing, PnL patterns, and position-sizing behavior in one place. If you're screening wallets to copy, drawdown analysis becomes much more useful when you can reconstruct how returns were made, how losses developed, and whether the strategy stayed stable under stress. Explore Wallet Finder.ai if you want a cleaner workflow for evaluating wallets beyond headline returns.

A premier DeFi analytics platform empowering traders to discover and analyze profitable blockchain wallets, trades and tokens.